Liquidity Fracture: AI de-risking meets crypto stress-test

Blueprint - De-risking phase, but rails continue to compound beneath price

Key Points

- The week played out in a classic risk-compression, forced unwind and late-week stabilisation sequence: an AI/mega-cap valuation wobble spilt into broader momentum, tightened financial conditions at the margin, and crypto absorbed the second-order hit via liquidity gaps and leveraged positioning.

- Cross-asset tone was defined by rotation out of crowded growth/momentum and a value bid, culminating in a late-week equity rebound that coincided with a mild crypto bounce off the lows.

- Credit anxiety remained the background amplifier: market commentary increasingly centred on where the “next” stress might surface (private credit, software/AI-adjacent leverage, and funding mismatches), which matters for crypto because it tightens the marginal buyer and lifts liquidation risk when volatility spikes.

- Importantly, BTC dominance failed to trend higher, remaining range-bound after a completed double-top structure (resistance ~60.5%, support ~58.0%).

- TOTAL3 broke decisively below its prior support band, exposing the April-2025 lows (~$658B) as the next structural reference, while failed rebounds are now capped near ~$776B.

- BTC relative to equities rolled over decisively, confirming crypto underperformance within the broader risk complex.

Our take: The macro tape mattered less through “data surprises” and more through duration/valuation sensitivity: once the market started to question the payback period on AI capex (and the financing stack behind it), risk premia widened quickly. Crypto did not need a crypto-native catalyst to sell off; it simply needed thin liquidity and leverage at the wrong moment. The late-week rebound helped, but it read more like positioning relief than a clean regime reset. Breadth is fragile when the market is simultaneously repricing AI economics and acknowledging latent credit stress. The fact that BTC.D did not trend higher even as TOTAL3 broke down is a key tell: the tape looked less like a clean “flight to BTC” and more like a broad balance-sheet contraction. In that setup, the only durable stabiliser is flow repair (ETFs) plus rails execution (stablecoin distribution, tokenised cash/settlement), because price rebounds without those inputs remain structurally “sellable”.

Bitcoin - ETF bleed dominates, but capitulation plumbing begins to surface

- Spot BTC ETF flows remained a headwind overall, with weekly net outflows of -$358.5M.

- The selloff included a liquidity-air-pocket / flash-crash dynamic and then a stabilisation attempt as the market moved from panic liquidation to more stable price discovery as two-way flow returned after hitting ~$60k.

- Mining difficulty printed a large negative adjustment (~11%), consistent with miners responding to stress via reduced effective hashrate / operational rationalisation.

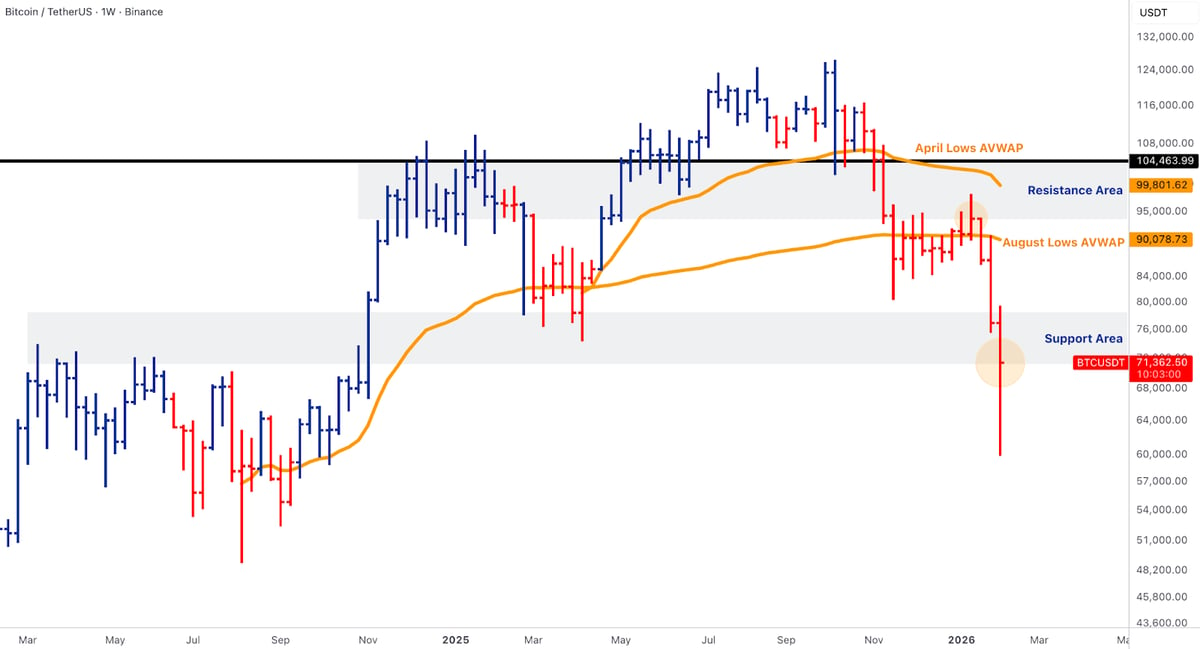

- From a technical perspective, BTC is trading well below the April AVWAP (~$104.5k) and August AVWAP (~$90.1k), with those now acting as overhead supply/resistance bands. Spot rebounded by the end of the week within its support pocket above ~$70k, after the violent break below mid-week. The nearest “risk-control” reference is whether BTC can reclaim and hold back into the $90k zone (August AVWAP), otherwise any rebounds risk staying corrective, opening the prospect of summer 2024 lows.

Our take: BTC is behaving like a macro-sensitive risk asset again, but the week also delivered the kind of “plumbing signals” that often appear near tradeable lows: difficulty downshifts, washout prints, and high-conviction volume days. That said, the tape won’t sustainably reset until ETF flow pressure stops dominating the marginal buyer; a couple of green days don’t change the regime if the rebound fails below the $90k-$100k repair band. The cleanest “risk-on permission” next week is BTC re-accepting above ~$90k, while the bear case remains: continued outflows + a second liquidation wave that forces another leg lower before balance sheets clear.

Ethereum - leverage unwind and weakening relative structure

- Spot ETH ETF flows were also negative, with weekly net outflows of -$170.4M

- DeFi reflexivity re-emerged as a downside amplifier, with collateralised positions forcing supply into declining liquidity.

- ETH/BTC is held within its support zone at ~0.03, well below the short-term resistance (~0.0354) and far below the higher resistance band (~0.04). The 0.0250 “breakout line” is now the critical downside reference.

- The week’s narrative was not only price: the Ethereum roadmap debate re-accelerated (re-examining rollup-centric assumptions, L2 decentralisation timelines, and what belongs on L1 vs L2), and ENS explicitly chose mainnet-first over launching its own L2, both reinforcing the theme that in stress regimes, markets tend to reward base-layer clarity and credible security primitives.

Our take: ETH is stuck between two forces: (1) macro-beta and de-risking, which pressures everything with duration characteristics, and (2) strategic “rails” demand, which grows slowly and rarely rescues price during deleveraging. The combination of net-red ETH ETFs and a soft ETH/BTC keeps ETH in “defensive posture” until flows turn. Tactically, ETH needs to rebuild acceptance above its June 2022 AVWAP (~$2,380) and then challenge the April AVWAP (~$3,115) before the chart stops reading as “sell rallies.” Structurally, the mainnet-centric decisions and roadmap scrutiny are directionally supportive, but they matter most once the market exits liquidation mode.

Solana & BNB - high-beta discounting continues

- Solana-linked products saw modest net outflows, showcasing weekly net outflows of −$9.3M, despite price action reflecting broader beta compression rather than product-specific stress.

- SOL lost its prior AVWAP shelf and is trading near $88.5, with $112-114 now acting as a critical “lost level” resistance zone and the 2024 lows forming the next structural support band.

- BNB lost its prior breakout level (~$742) and is back at ~$645, leaving $1,000 as a distant “re-risk” marker and a wide vacuum beneath if risk conditions worsen.

- In the broader alt complex, liquidity fractured into islands: idiosyncratic winners can still print strong weeks, but index-level breadth (TOTAL3) broke hard.

Our take: SOL and BNB both behaved like liquidity barometers. When the market is comfortable, they lead; when the market is stressed, they gap lower and require time to rebuild. SOL’s key question is whether it can reclaim/accept above ~$114 (AVWAP) to stop the slide from turning into a persistent “sell-the-rip” regime. BNB is a cleaner “risk-on/risk-off” signal: holding above ~$742 would have implied structural sponsorship; losing it shifts the burden to time (base-building) rather than price (immediate reversal).

Rails & Productisation - stablecoins and tokenised cash keep compounding even as price breaks

- Stablecoin and “cash-on-chain” rails continued to push forward despite the drawdown: Fidelity’s stablecoin (FIDD) went live, and along with CME’s tokenised cash/coin efforts with collateral use, both point to regulated distribution and collateral utility as the next adoption leg.

- Tether remained central to the “rails” story: coverage included strategic investments and expansion, reinforcing USDT’s role as the dominant settlement asset in risk-off conditions.

- There were additional policy-market plumbing shifts: CFTC scrapping a proposal to ban political event contracts adds to the broader narrative of US market structure being “re-opened” for certain crypto-adjacent product types.

- On tokenisation, there was a clear “jurisdiction competition” thread: market participants warned EU constraints could push tokenised market activity toward the US, while China reiterated/tightened its stance on RWA tokenisation/offshore yuan stablecoins, two very different policy vectors shaping where issuance can scale.

Our take: This keeps being the part of the market that makes the drawdown less existential than prior cycles: even as price breaks, the infrastructure for settlement, collateral, and tokenised distribution keeps compounding. In practice, that means the medium-term floor for the asset class is increasingly set by who controls the rails (stablecoins, broker rails, tokenised cash) rather than by pure speculative inflows. Near-term, though, rails progress is not a timing tool; ETF flows, and credit optics still determine whether “rails execution” translates into price support this month versus next quarter.

Outlook - Macro/credit catalysts and what they mean for crypto risk

Key Points

- US labour market data (payrolls/unemployment and surrounding labour indicators) will shape expectations around growth durability vs soft-landing risk.

- Global rewards remain the key cross-asset transmission channel: re-acceleration risks pressuring equities and keeping crypto defensive; downside rewards surprises can help stabilise risk, but the interpretation depends on why rewards fall. Inflation data released on Friday will play an important role in shaping rate expectations as the market continues to assess Kevin Warsh as Fed Chair nominee.

- Credit conditions remain a latent tail risk: private credit stress can spill into equities and crypto sentiment via funding availability and risk premia.

- For crypto, ETF flow stabilisation remains the most immediate signal to watch; continued rails execution is the medium-term ballast.

Our take: Next week’s macro is best framed around the volatility of expectations. CPI will shape the rates impulse; a benign print helps stabilise rewards and supports risk digestion; an upside surprise risks re-tightening financial conditions and prolonging the defensive regime. The labour channel matters more for growth durability than for near-term inflation: firm labour tends to keep soft-landing narratives intact, while a downside miss is only “risk-on bullish” if it reads as cooling, not cracking. If downside surprises start to cluster in a recession-like way, that’s not a “rewards down, risk up” scenario; it’s risk-off with crypto vulnerable via liquidity and leverage. For crypto specifically, ETF flow stabilisation remains the highest-frequency tell: fewer large red days and more “small green” days would validate the late-week bounce; continued heavy red prints would argue the market is still in the process of finding a durable base.

Thanks for reading this week's Market Pulse.