Dispersion Over Direction: Crypto Markets Digest Macro and Geopolitical Headwinds

Key points

- The Crypto market remained in a controlled corrective regime, characterised by risk-absorption and consolidation.

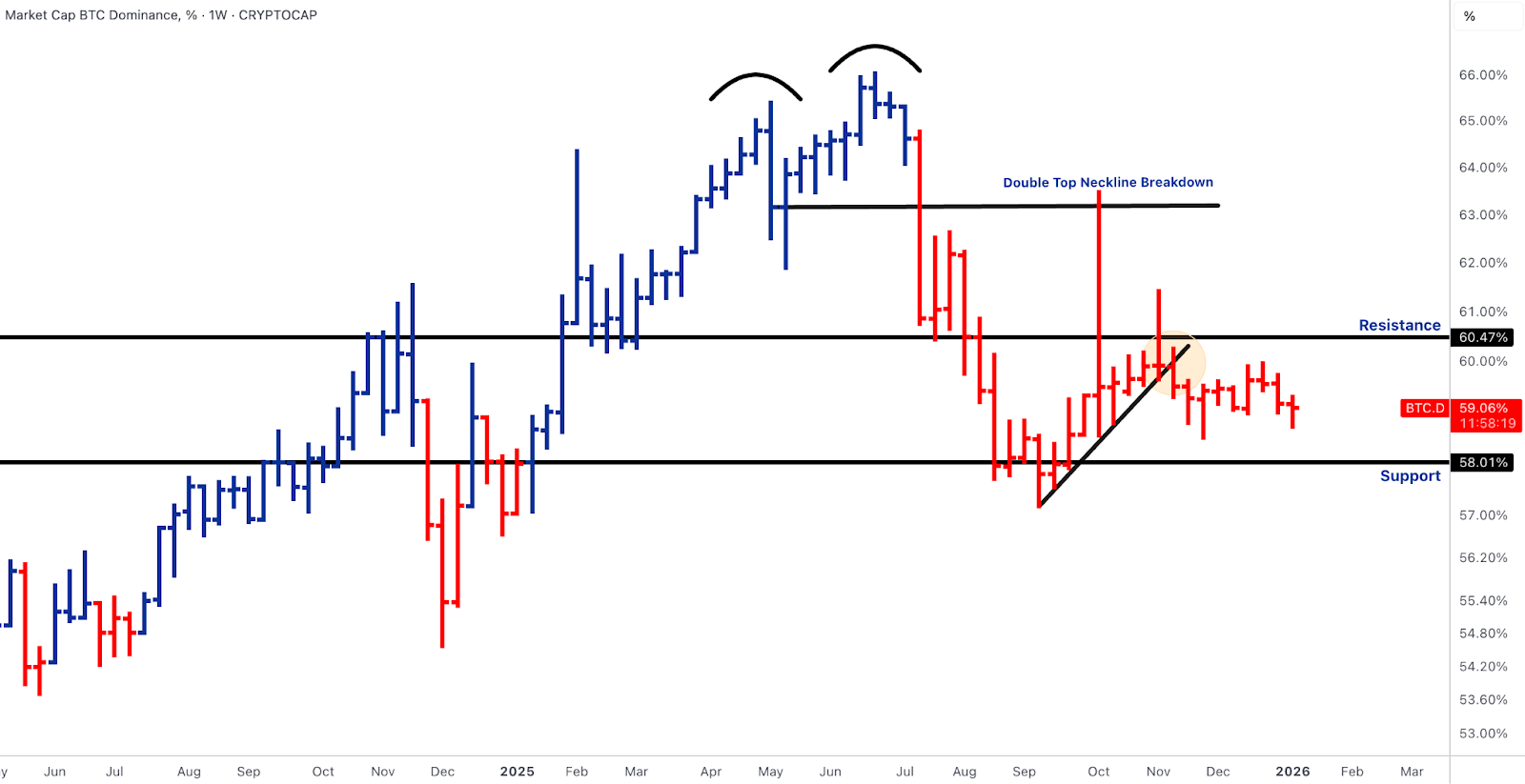

- BTC dominance stabilised near ~59% but failed to reclaim ~60.5% resistance, keeping the tape rotation-friendly rather than BTC-led.

- TOTAL3 remains below the prior ATH weekly close, attempting to rebuild inside the former resistance zone; ~776B is the key structural support separating orderly consolidation from renewed downside risk.

- Spot BTC and ETH ETF flows extended a net-negative streak, but the cadence resembled tactical de-risking rather than forced liquidation.

- Geopolitical risk premium increased (Middle East escalation sensitivity), raising risk of cross-asset exposure to energy, USD liquidity and volatility spillovers without triggering a disorderly risk-off shock.

- US macro conditions reinforced a higher-for-longer backdrop, limiting expectations for near-term policy easing and constraining duration-sensitive risk assets.

Our Take

This was a risk-absorption and recalibration phase. Persistent ETF outflows, macro headwinds and a higher geopolitical risk premium capped risk appetite, yet the absence of disorderly selling suggests underlying demand remains intact but increasingly selective. Until either macro clarity improves or geopolitical risks de-escalate, the dominant regime remains consolidation, rotation and relative-value positioning rather than broad beta acceleration.

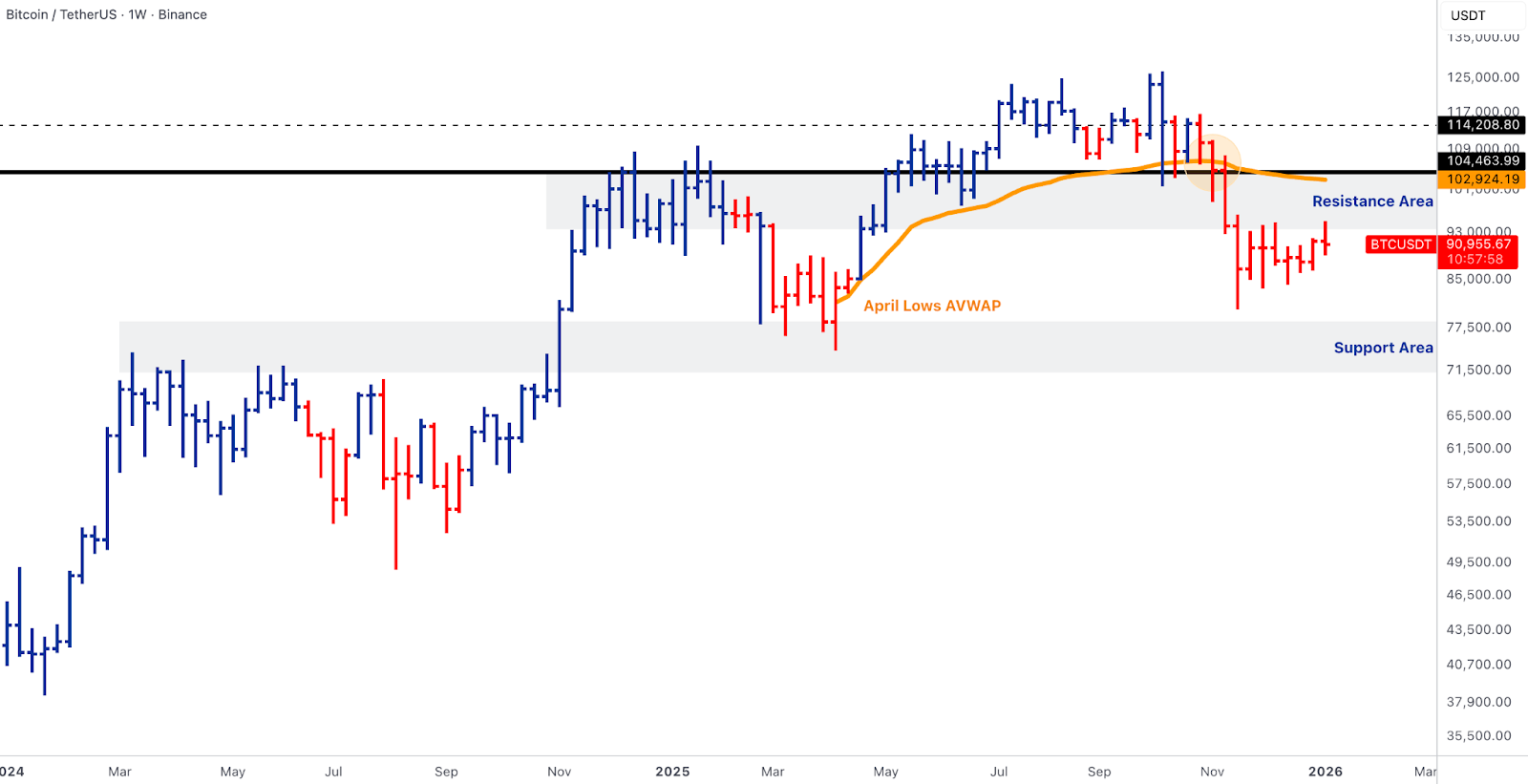

Bitcoin - Structure Intact, Acceptance Still Elusive

Key points

- BTC keeps trading below the April-lows AVWAP, which continues to act as dynamic resistance near ~102-104k, aligned with the broader ~103-105k resistance band.

- Price stabilised in the low-90ks following rejection from overhead supply.

- The pullback unfolded without signs of panic or liquidity stress, reinforcing a corrective phase rather than trend failure.

- Higher-timeframe support remains intact; the key question is whether BTC can re-accept above the April AVWAP and reclaim 102–104k.

Our Take

BTC remains structurally constructive but tactically capped. The market is pricing time, not systemic risk, and the next meaningful regime improvement requires acceptance back above the AVWAP-aligned supply zone. Until that occurs, BTC functions more as a stabilising anchor than a leadership engine, and dispersion is likely to persist elsewhere in the complex.

Ethereum - Relative Stabilisation, Still Below Key AVWAP

Key points

- ETH remains capped below the April-lows AVWAP, which continues to reject upside attempts and defines the near-term acceptance threshold.

- ETH has held its higher-timeframe support and avoided breakdown despite a challenging macro and flow backdrop.

- ETH/BTC remains above cycle lows and is attempting to base, but has not confirmed renewed relative strength; a sustained move back above ~0.039-0.040 would be required to validate leadership.

- ETF flow dynamics remain unresolved, keeping ETH in stabilisation rather than acceleration mode.

Our Take

ETH’s fundamental base remains intact, but price is still treating the April AVWAP as supply. Until ETH reclaims that level and ETH/BTC confirms follow-through beyond its near-term ceiling, Ethereum remains a stabilising asset rather than a leadership vehicle. The signal is improving, but still incomplete.

Solana & BNB - Leadership Fatigue Remains, Structure Still Valid

Solana (SOL)

Key points

- SOL rejected from ~200-210 and retraced toward ~114-115, which aligns with long-term AVWAP support from the January 2023 lows.

- Momentum cooled, but the move remains proportional to the broader environment rather than SOL-specific weakness.

- Sustained acceptance back above ~200 would be required to reassert leadership.

Our Take

SOL is digesting after leadership, not failing structurally. Holding the AVWAP-confluence support zone keeps the higher-timeframe thesis intact, but leadership will only return with acceptance above key resistance and improved risk appetite.

BNB

Key points

- BNB failed to hold above $1,000 and retraced toward the prior breakout zone around ~$740, now acting as structural support.

- Higher lows remain preserved; upside continuation likely requires improved macro conditions or renewed exchange-linked catalysts.

Our Take

BNB remains in a consolidation regime above an important breakout shelf. It continues to trade more like a platform/cash-flow proxy than pure speculative beta, with $1,000 remaining the obvious re-rating trigger.

Alpha Cluster - Catalyst-Backed Strength Amid Broad Consolidation

Key points

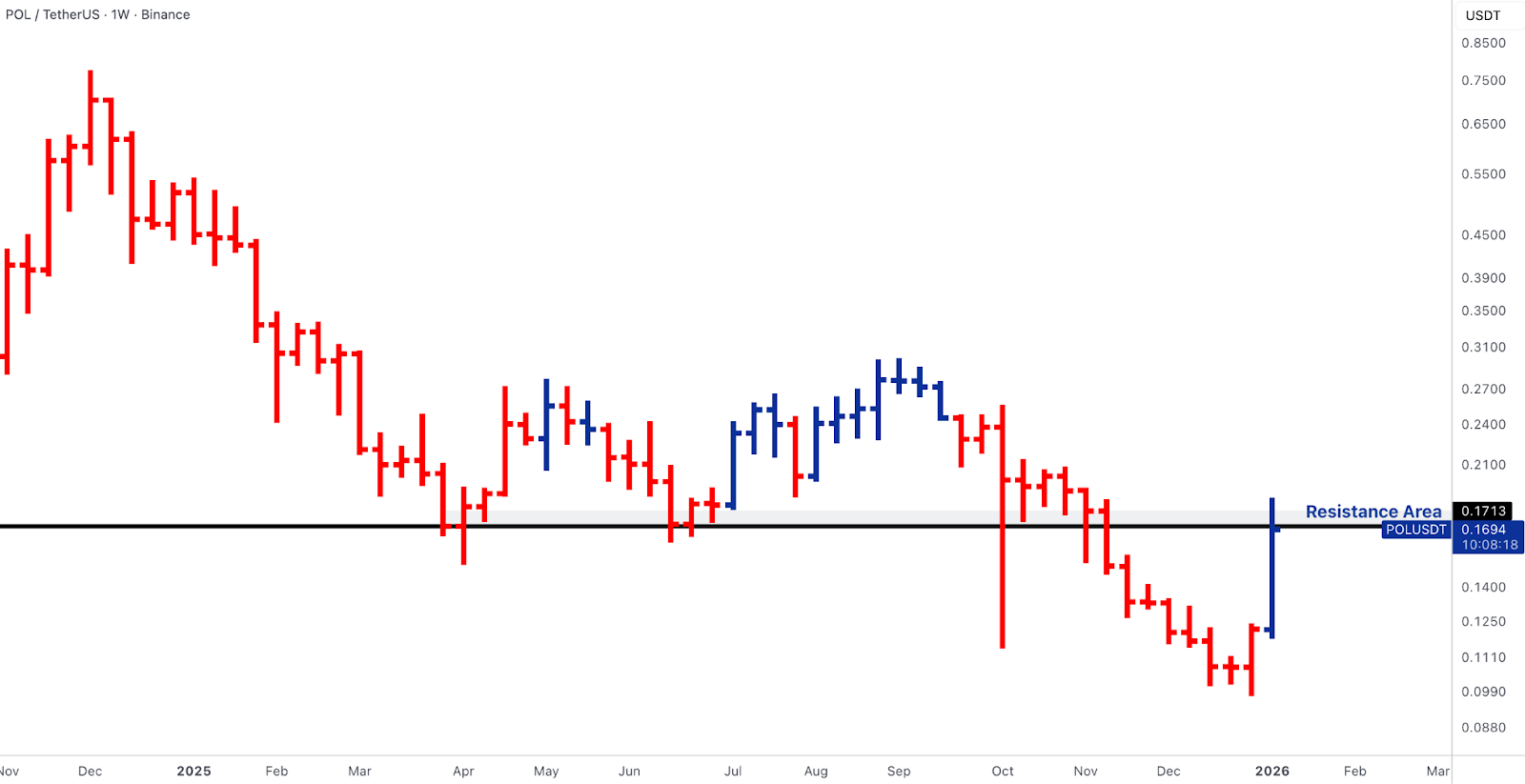

- Dispersion remained high, but only POL, RENDER and XRP displayed moves supported by identifiable catalysts rather than purely technical mean reversion.

- Polygon (POL) rebounded sharply into the ~0.17 resistance area, supported by renewed attention to Polygon’s modular scaling roadmap and ongoing enterprise/economic positioning.

- Render (RENDER) reclaimed into the ~2.40–2.80 resistance band, supported by sustained institutional interest in decentralised GPU / AI-compute narratives.

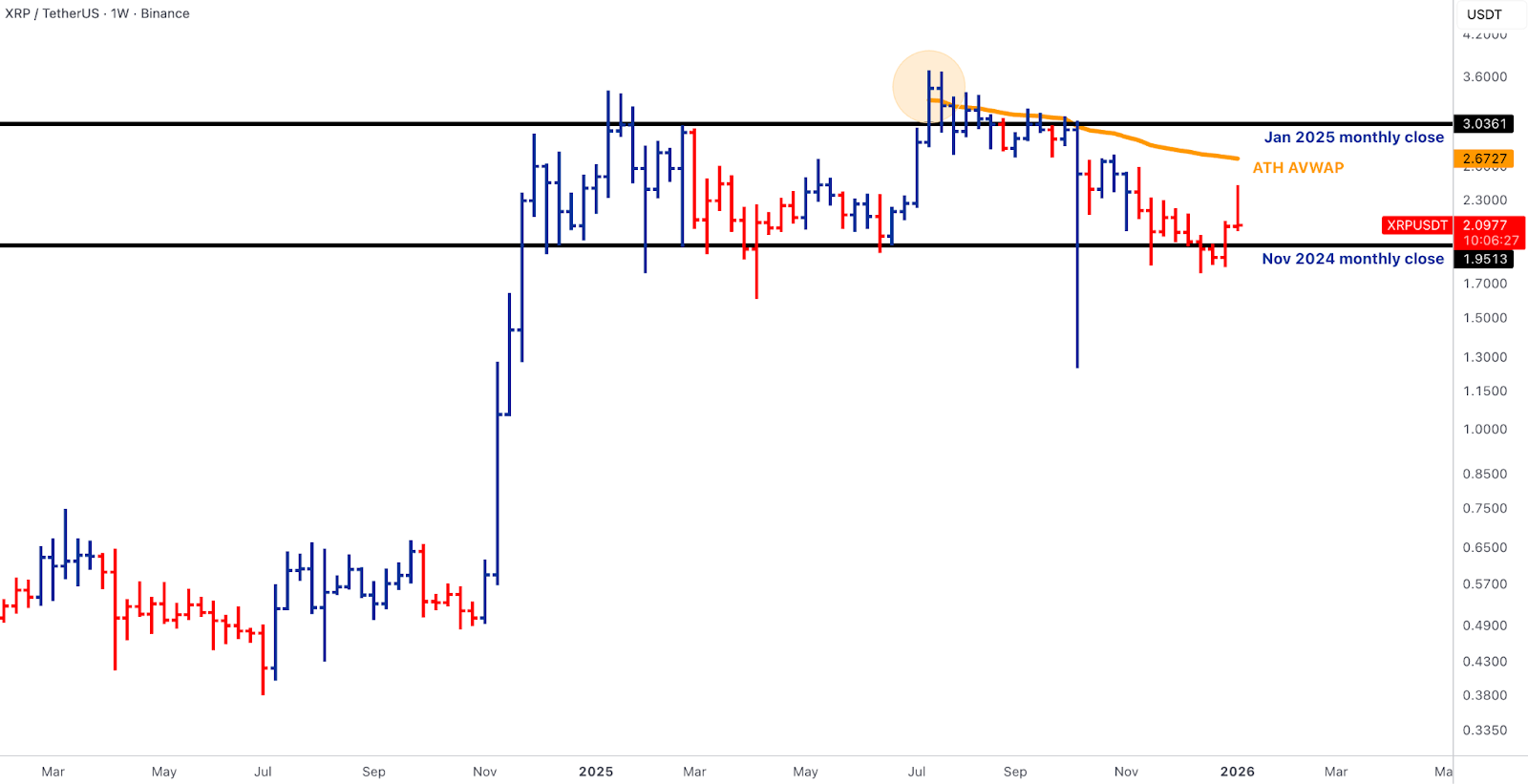

- XRP remained range-bound technically but attracted meaningful attention due to regulatory and institutional progress (UK licensing developments) and persistent ETF-related optics; it held above key support while broader beta weakened.

Our Take

This was not a broad risk bid; it was selective repricing into catalysts. POL and RENDER expressed infrastructure narratives that can be underwritten even during macro-capped regimes, while XRP continued to trade as a policy-sensitive payments/rails proxy rather than a pure alt beta. The common thread is that these moves remain credible only if they can hold reclaimed levels into follow-through; without broader acceptance in ETH/BTC, alpha remains rotational and reversible.

Rails & Productisation — Institutional Infrastructure Accelerates Under Scrutiny

Key points

- Tokenised bank money moved from concept to activation: BNY Mellon activated its tokenised deposit service, enabling on-chain payments and collateral functionality and marking a concrete step beyond pilots into live institutional usage.

- Large financial institutions continued to build crypto-native rails: JPMorgan expanded its on-chain settlement stack (JPM Coin / Canton), reinforcing the direction of travel toward permissioned, interoperable financial infrastructure.

- Stablecoin onshoring and charter strategies advanced: Trump-backed World Liberty Financial’s pursuit of a US bank charter to issue USD1 fully onshore highlights increasing competition around regulated stablecoin issuance and distribution, not just market share.

- Payments and trading platforms pushed further into hybrid models: Bitget expanded TradFi-style market access within crypto platforms, while Morgan Stanley reiterated plans to launch a crypto wallet in 2026, signalling continued convergence between traditional brokerage and digital asset rails.

- Regulatory pressure tested the system’s edges: State-level action against Polymarket and heightened scrutiny of illicit flows (including reports on Iran-linked crypto activity) underscored that as rails scale, compliance, AML, and jurisdictional controls are becoming price-relevant variables, not background noise.

- UK and European regulatory gateways progressed: Ripple securing FCA authorisation reinforced the UK’s role as a regulated expansion hub for crypto payments and settlement infrastructure.

Our Take

This was unequivocally a rails week. The market is no longer debating whether tokenisation, stablecoins, or on-chain settlement will exist, it is now deciding who controls distribution, compliance, and trust at scale. BNY’s tokenised deposits and JPMorgan’s on-chain settlement rails demonstrate that regulated institutions are operationalising crypto infrastructure in ways that are repeatable and balance-sheet relevant. At the same time, enforcement actions and sanctions-linked scrutiny make clear that growth will not be frictionless. The winners in this phase are unlikely to be speculative protocols, but platforms that can combine regulatory alignment, institutional trust, and composability. This structural build-out is slower than price cycles, but far more durable, and it is increasingly the foundation beneath any future risk-on phase.

Outlook - What Matters From Here

Key points

- Markets remain highly sensitive to incoming US macro prints that shape real-rate expectations (labour updates, inflation signals, sentiment), with upside surprises likely reinforcing a risk-contained regime. Earnings season starts next week with financials.

- Geopolitical developments remain a first-order variable for cross-asset volatility through energy prices and USD liquidity conditions.

- A transition back to broad risk engagement requires either acceptance above key AVWAPs for BTC and ETH or a meaningful shift in macro/flow dynamics.

Our Take

The near-term path remains range-bound and event-sensitive. Unless macro surprises materially weaken the “higher-for-longer” pricing or geopolitical risks de-escalate, broad beta should remain capped and dispersion should continue to dominate. The highest-quality signal will come from acceptance: BTC reclaiming its AVWAP-aligned supply zone and ETH reclaiming the April-AVWAP pivot. Until those conditions are met, the playbook remains selective, rails, policy-adjacent assets and catalyst-driven alphas over indiscriminate beta.