Confidence Shock, Structural Separation: Crypto De-Risks as Institutional Rails Compound

Blueprint - Regime, Flows & Cross-Asset Context

Key Points

- Crypto entered a confidence-driven de-risking phase, triggered by Bitcoin’s break below the $80k psychological level and reinforced by the heaviest ETF redemptions since early 2025.

- Spot BTC ETFs recorded roughly $1.3-1.6B in net outflows over the month, while ETH products remained persistently negative, reflecting discretionary risk reduction rather than forced liquidation.

- Market structure deterioration remained orderly: no exchange liquidity stress, no stablecoin dislocations, no leverage cascades.

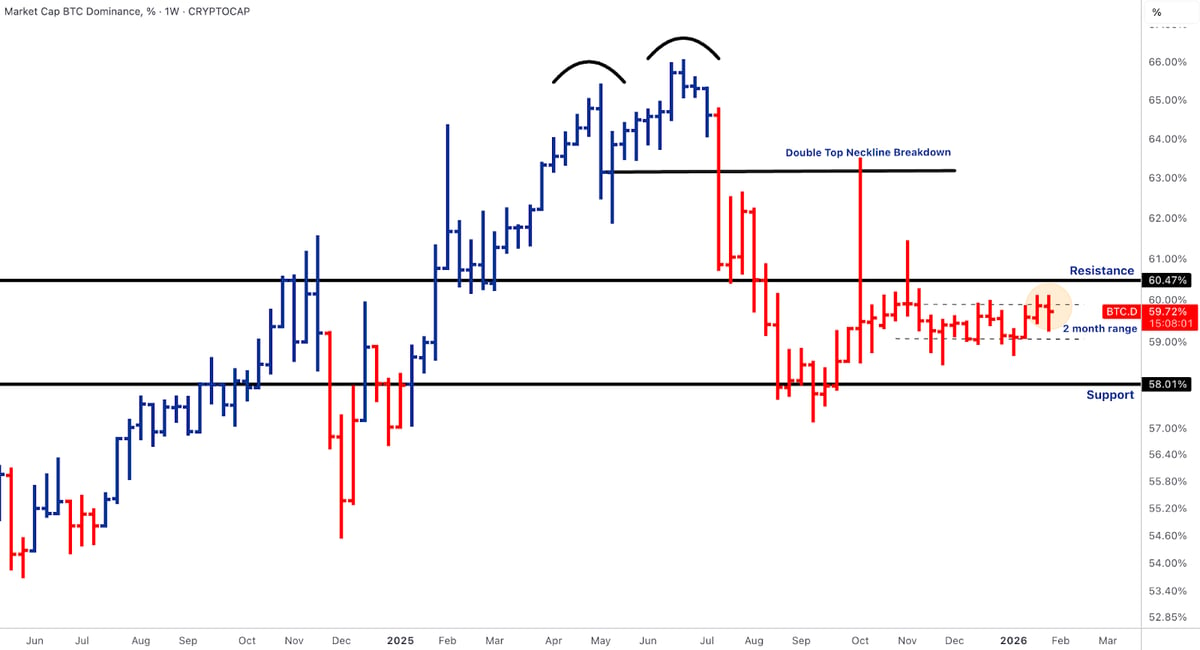

- BTC dominance stabilised but failed to extend meaningfully higher, confirming de-risking without a return to BTC-led leadership.

- TOTAL3 retraced into the $760-780bn zone, a historically critical band separating cyclical resets from structural breakdowns.

- Cross-asset signals reinforced defensiveness: equities weakened (notably AI-linked software), private credit stress re-entered narratives, while gold and silver extended safe-haven rallies amid geopolitical and policy uncertainty.

Our take: This was a confidence shock, not a systemic failure. Price adjusted faster than structure, and the widening gap between market volatility and institutional infrastructure progress continues to define the regime. The environment remains corrective, selective, and balance-sheet sensitive, but not existentially bearish.

Bitcoin - ETF-Driven De-Risking, Structure Under Pressure

- BTC failed to hold the $80k level, accelerating downside as ETF redemptions compounded negative sentiment.

- On-chain data shows rising realised losses, concentrated among short-term holders; long-term holders remain largely inactive.

- No evidence of miner capitulation, exchange stress, or disorderly supply release.

- Price remains below key AVWAP resistance zones, confirming acceptance of lower after multiple failed reclaim attempts.

Our take: Bitcoin is undergoing flow-driven sentiment repair, not structural erosion. ETF products are acting as short-duration risk instruments, while deeper institutional and sovereign-style demand remains intact. Sustainable recovery requires ETF flow stabilisation and macro relief, not narrative shifts alone.

Ethereum - Tactical Weakness, Strategic Durability

- ETH underperformed as ETH/BTC retraced toward the lower end of its multi-month range.

- ETH remains below the April-lows AVWAP, which continues to cap upside and define near-term acceptance.

- Whale-linked de-risking events weighed on price, but occurred alongside record-high staking participation and continued capital allocation to Ethereum security, privacy, and censorship resistance.

- Ethereum remains the dominant settlement layer for tokenised funds, stablecoins, and institutional on-chain activity.

Our take: Ethereum is strategically indispensable but tactically sidelined. Macro beta and ETF asymmetry explain recent weakness more than platform fundamentals. ETH retains convex upside to macro stabilization but is unlikely to lead until AVWAP reclaim and ETH/BTC confirmation occur.

Solana & BNB - Leadership Unwound, Structure on Trial

Solana (SOL)

- SOL completed a full leadership unwind, retracing into the January 2023 AVWAP zone (~$110-115).

- Network activity cooled after prior speculative intensity; validator participation and throughput normalised.

- No material ecosystem impairment observed.

Our take: SOL is now at a structural inflexion point. Holding long-term AVWAP preserves the broader cycle thesis; failure would signal deeper regime rotation away from high-beta leaders.

BNB

- BNB failed to sustain acceptance above $1,000 and retraced toward the prior breakout zone (~$740).

- Relative resilience reflects exchange-linked cash-flow relevance rather than speculative demand.

Our take: BNB continues to trade as a platform-equity proxy. Downside is cushioned by revenue durability; upside remains macro-constrained.

Emerging Rotation & Alpha - Usage and Policy Sensitivity

Hyperliquid (HYPE)

- HYPE materially outperformed as on-chain derivatives activity surged.

- Aggregate open interest across Hyperliquid-linked venues approached $900M, driven by trader migration from centralised venues amid broader risk reduction.

- Performance was supported by measurable increases in volume, fees, and engagement.

Our take: This was a usage-driven repricing, not speculative noise. Sustainability depends on retention, but the signal reflects real leverage migration.

Canton (CC)

- CC benefited from renewed focus on permissioned blockchain infrastructure and regulated settlement stacks.

- Performance aligned with regulatory clarification around tokenised securities and institutional on-chain settlement frameworks.

Our take: CC functions as a policy-aligned infrastructure proxy, well-positioned in environments favouring compliance-first adoption over speculative beta.

Rails & Productisation - Profitability, Regulation, and Scale

- Tether reported ~$10B in net profit for 2025, supported by over $6B in excess reserves, reinforcing its position as crypto’s most profitable and systemically important liquidity issuer.

- Stablecoin growth moderated post-shock, but transaction volumes remain dominated by enterprise and payments use cases, not retail churn.

- Traditional finance continued operational tokenisation: Asset managers expanded tokenised fund offerings, exchanges and custodians scaled regulated rails, and regulators clarified frameworks for tokenised securities and settlement across the US, Europe, and Asia.

- Payment adoption accelerated, driven by large businesses and financial institutions, not speculative wallets.

Our take: This remains a rails-first cycle. Profitability is real, regulation is converging toward enablement, and institutional infrastructure is compounding regardless of price volatility. These foundations matter more than short-term market sentiment.

Outlook - Macro, Earnings & Transmission Channels Ahead

Key Points

- US PMIs are the primary macro focus, shaping expectations around growth momentum without near-term inflation prints.

- US labour market data (payrolls, unemployment) will shape expectations around growth durability versus soft-landing risk.

- Any re-acceleration in yields (globally) could pressure equities and reinforce crypto defensiveness; downside surprises would support stabilisation.

- Earnings skew toward AI-adjacent software, semiconductors, and platform enablers, following last week’s mega-cap releases; guidance will influence broader risk appetite.

- Credit conditions remain a latent risk, with private credit stress capable of spilling into equities and crypto sentiment.

- For crypto, ETF flow stabilisation remains the most immediate signal to watch; continued rails execution provides medium-term ballast.

Our take: The coming week should be viewed as a growth and confidence checkpoint rather than a catalyst phase. US PMIs and labour market data will shape expectations around growth durability versus soft-landing dynamics, with markets focused on consistency across indicators rather than isolated data points.

Global rates remain the primary transmission channel. A renewed rise in yields would tighten financial conditions and reinforce defensiveness across equities and crypto. More moderate downside surprises that keep yields contained would likely support stabilisation and allow risk assets to re-base. Only materially weak, recession-like data, which is not the base case, would challenge this framework and reintroduce broader downside risk.

Earnings guidance from AI-adjacent software, semiconductor suppliers, and platform enablers will further influence sentiment following last week’s mega-cap releases. For crypto, ETF flow stabilisation remains the most immediate signal to monitor. Until that improves, price action is likely to remain selective and range-bound, while continued execution across stablecoins, tokenisation, and institutional rails provides meaningful medium-term support.

Thanks for reading this week's Market Pulse.