Rotation Reverses, Liquidity Tests the Pipes

Market Overview

- Last week marked a decisive turn as the tape flipped from the prior “hold-and-build” regime into genuine de-risking and rotation.

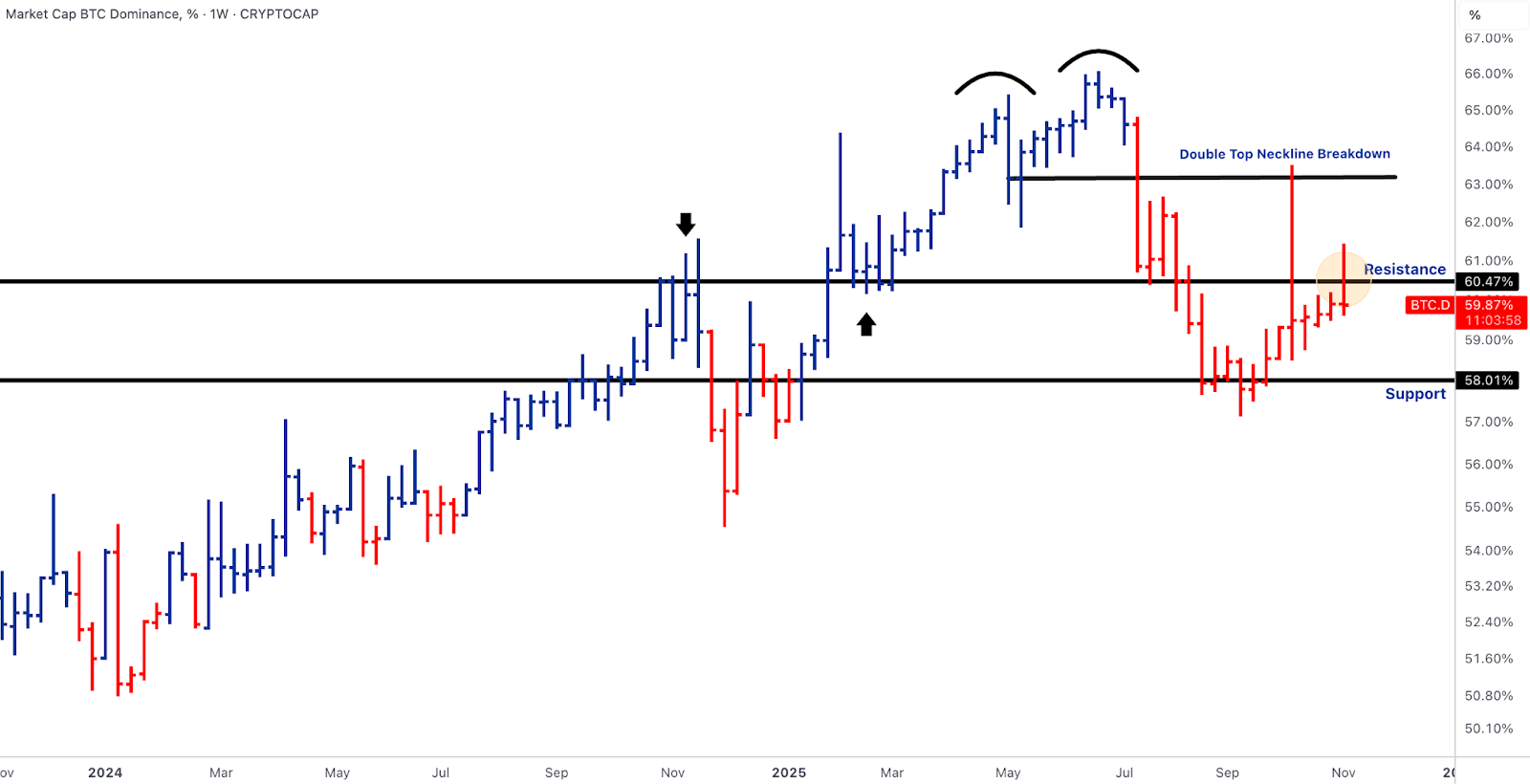

- BTC.D rebounded toward 60%, re-testing its neckline resistance but stopping short of a breakout, while TOTAL3 (ex-BTC & ETH) slid to ~$0.95T, breaking its rising trendline yet holding the critical $0.93-0.95T support band.

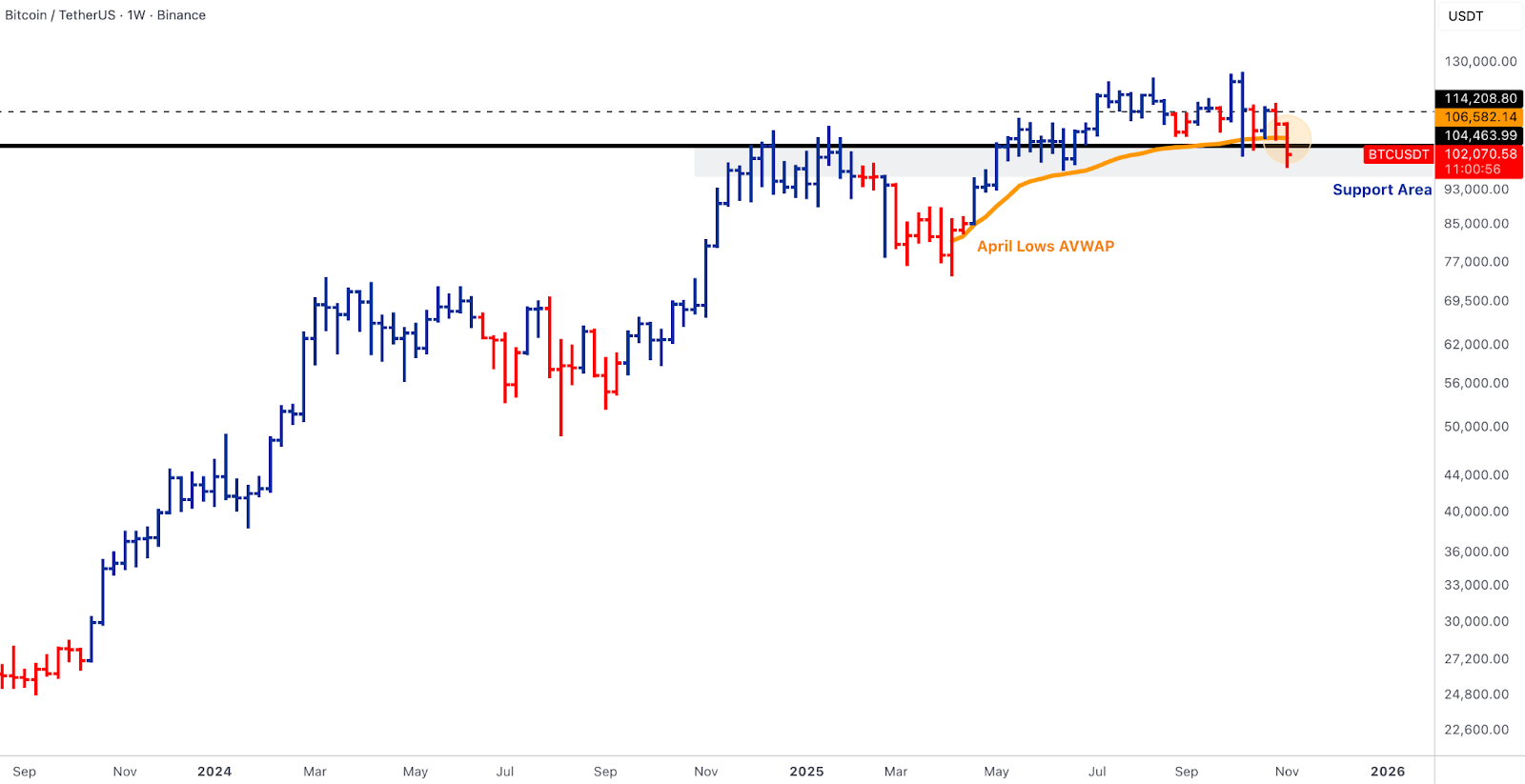

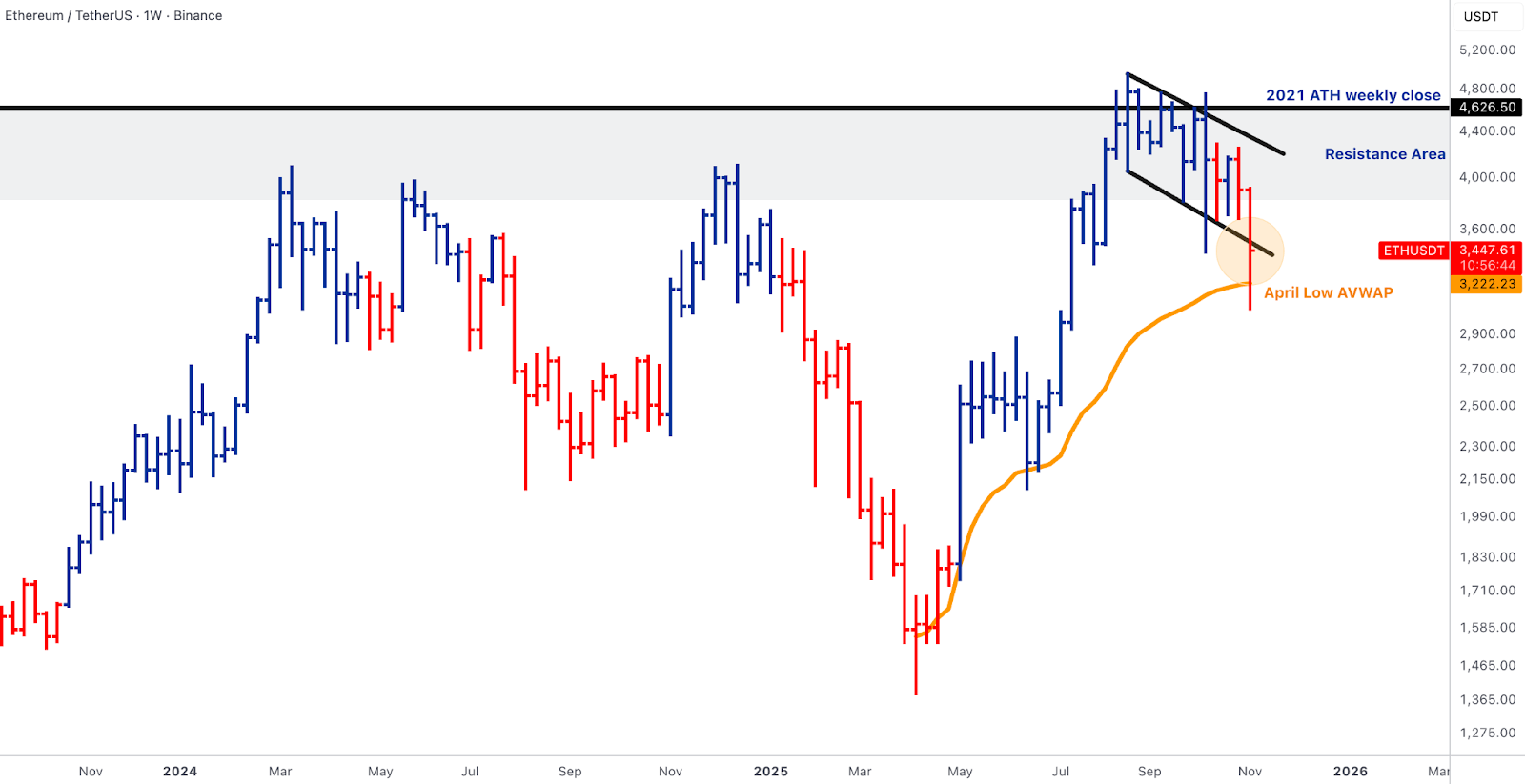

- Spot majors lost key levels as BTC closed below its April lows AVWAP, ETH breached pattern support, and ETH/BTC fell beneath short-term structure, signalling that while the market is not abandoning crypto, it is repricing risk along the curve.

- The defining driver was ETF rotation. BTC ETFs saw ~$1.21B in net outflows, ETH ETFs ~$0.51B, while SOL ETFs absorbed ~$136.6 million in steady five-day inflows. This was not capitulation; it was a migration of capital away from over-crowded ETF beta toward vunder-owned growth rails.

- The largest BTC ETF redemptions since August reinforced that theme: institutions are cutting weight at the top, not exiting the asset class.

BTC - AVWAP Lost, ETF Outflows Bite, Structural Story Intact

- Price action was unambiguous: BTC closed below the April lows AVWAP (~ $106k), landing in the $93-104k support zone after intraday wicks through $100k. Resistance is now stacked at $106-107k (AVWAP retest), then $114-115k and $126-128k. The technical setup confirms a shift from neutral to corrective bias.

- BTC ETFs printed their heaviest redemptions since May throughout the week (-$1.21B), led by Fidelity (FBTC) and ARK (ARKB). Four of five sessions closed negative, briefly interrupted by 6 Nov’s $240M relief inflow. Yet structural demand endures: JPMorgan’s IBIT holdings grew 64% QoQ, Metaplanet borrowed $100M against BTC to add exposure, and Block derived one-third of Q3 revenue from BTC.

- Technically, it is now below both a key AVWAP and heavy ETF supply, suggesting rallies into $106-115k will meet selling until ETF flows stabilise.

- Fundamentally, the ecosystem of banks, corporates and reserve-style allocators still adds BTC on structural timelines, which limits the probability of a sustained breakdown below the $93-95k band without a macro shock.

ETH - Underperforms, But the Staking Flywheel Builds

- ETH lagged on every axis. On USD pairs, it broke channel support and tagged the April-low AVWAP (~ $3.2k) before closing ~ $3.45k. On ETH/BTC, the ratio slipped below 0.034, close to confirming tactical rotation into BTC.

- Flows corroborated the weakness: ETH ETFs shed $507.7M over the week, dominated by BlackRock’s ETHA and Grayscale’s ETHE. The market is unwilling to pre-position for the Fusaka upgrade while redemption pressure remains.

- Structurally, however, the staking and L2 flywheel continues to tighten: the validator queue has grown to over 1.5M ETH waiting to start staking, locking in future reductions in free-float supply.

- With Aave’s loan book above $25B and institutional ETH treasuries continued reallocation into on-chain yield, ETH remains a hold, not a buy, as core long-term economics remain intact, albeit leadership will not rotate back unless ETH/BTC reclaims 0.034 and ETF flows neutralise.

SOL & BNB - ETF Bid vs. Technical Damage

- SOL exemplified the week’s paradox: price weakened while institutional demand accelerated. The token extended its correction toward $150-160 after losing the $201-202 support band and ascending trendline, yet SOL ETFs absorbed $136.6M in five consecutive inflow days, the only major product set with positive net flows.

- Beneath the surface, corporate adoption continued to reinforce Solana’s status as an institutional treasury and balance-sheet asset. Upexi’s treasury added 2.1M SOL, confirming that corporates are increasingly holding Solana natively rather than synthetically. In parallel, a Solana-affiliated company board approved up to $100M in share buybacks, explicitly linking the program to a SOL-denominated treasury narrative, a first-of-its-kind blend of corporate-finance policy and on-chain asset management.

- Together, these moves elevate SOL from a high-beta blockchain to a monetised corporate-treasury instrument, one that can now transmit real-world balance-sheet flows into on-chain liquidity.

- Technically, SOL remains in a pullback: the January 2023 AVWAP and horizontal support near $114-115 define the next defence zone. Holding that band would preserve its leadership profile once market breadth stabilises.

- Structurally, the asset now trades as crypto’s growth-equity proxy, volatile, institutionally owned, and increasingly integrated into corporate capital policy.

- BNB experienced its first meaningful retest since the $742 breakout, slipping just below the $1,000 round number but closing well above structural support. Exchange-fee generation, Ondo’s tokenisation on BNB Chain, and sustained rails activity continue to support the token’s floor. BNB behaves like a profitable exchange equity with systemic throughput, not a speculative L1.

Top Performers & Alpha Cluster - Privacy, Governance and Storage

- Zcash (ZEC) exploded from its $74-80 base to above $600, surging past the May 2021 weekly high (~$305) and lifting market cap above $10B. The long, rounded base transitioned into vertical extension on increasing shielded supply and ECC’s Q4 roadmap. ZEC is now the default liquid privacy proxy, but with asymmetric risk: a break back below $305 would end the parabolic phase.

- Given ECC’s published Q4 roadmap last week and the multi-fold increase in shielded supply, ZEC is now the default liquid privacy proxy. However, risk-reward at these levels is asymmetrical: any break back below ~$305 would signal the blow-off is over. It remains an important signal asset for privacy demand, but position sizing has to respect the verticality of the move.

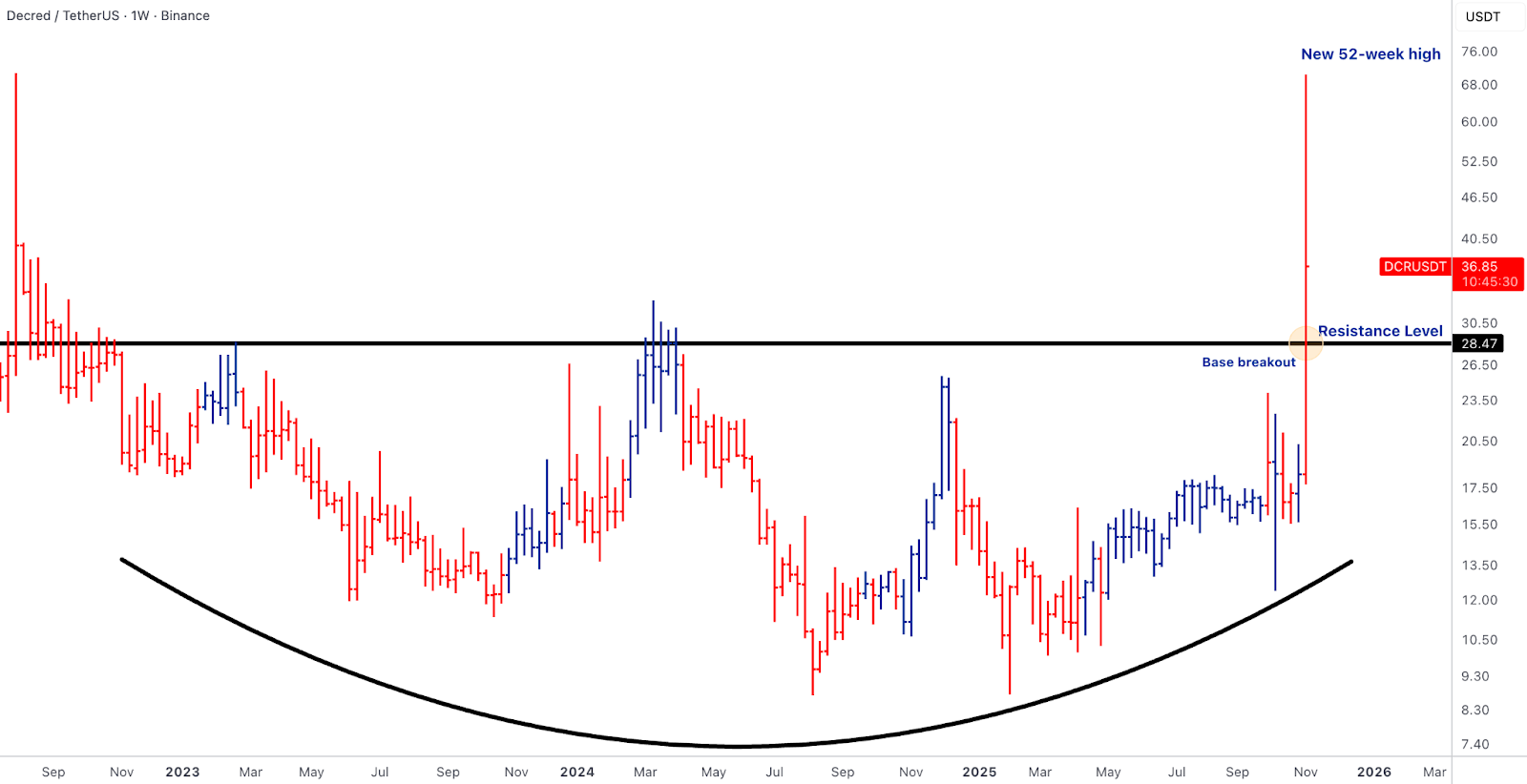

Decred (DCR) cleared multi-year resistance at $28.5 and set new 52-week highs around $36-37. Without a singular headline, the move reflects renewed interest in on-chain governance and hybrid PoW/PoS yield. It functions as an index for “governance yield” sentiment.

Internet Computer (ICP) reclaimed $5.98 resistance and closed above $7 for the first time in a year, reversing a persistent downtrend. The surge was mostly technically driven, backed by a major launch of its AI builder platform (“Caffeine”) and a large increase in volume/open interest, with short-covering and rotation into under-owned compute beta. Holding above $6 keeps the next target at $9-10.

Filecoin (FIL) advanced to ~$2.7, testing the $3.05 resistance that has capped since mid-year, driven by the DePIN infrastructure rally. The setup resembles a first impulse from a depressed base as AI data and storage themes regain attention. On-chain data shows increased whale accumulation (+32%), exchange supply dropping, and strong volume (~$1.4B) accompanying a breakout from a descending wedge structure, ahead of “DePIN Day” on Nov 18.

Rails & Tokenisation

- While the majors were corrected, the rails were strengthened. Stablecoin issuers’ annualised profits surpassed ~$10B, and policymakers moved from defensive to constructive.

- Macro conditions reinforced selectivity rather than stress. The US 10-year yield closed at ~4.1%, consolidating last week’s move. Policy tone was more revealing: a Fed governor called stablecoins “a force to be reckoned with,” Japan and the UK advanced bespoke stablecoin regimes, and Italian banks supported the ECB’s digital-euro framework while pleading for phased costs, an implicit admission that legacy banking rails lag programmable money.

- Kazakhstan’s $1B crypto-reserve plan extended sovereign adoption. The macro-policy mosaic thus points toward gradual recognition of digital-money rails as macro-relevant liquidity infrastructure even as risk assets retrace.

- Synthetic experiments like deUSD collapsed, underscoring that over-engineered designs cannot compete with fully backed, high-carry models, with the latter winning the race to institutional acceptance.

- Tokenisation and index initiatives followed suit: Franklin Templeton launched Hong Kong’s first tokenised fund, FTSE Russell and Chainlink bridged Russell 1000 data on-chain, and on-chain perp volumes topped $1.2T in October. Value is accreting to oracles and stablecoin rails as fee engines rather than to the generic L1 beta.

Outlook

- Last week’s tape is best read as a flow-driven ETF de-risking, not a structural collapse. BTC and ETH ETF outflows underscore institutional position trimming after an extended run.

- SOL’s consistent inflows highlight rotation within the ecosystem rather than flight from it. Rails and tokenisation projects continue to attract policy support and capital inflows, while privacy and governance tokens reflect residual risk appetite at the margin.

- TOTAL3’s trendline break and BTC’s AVWAP loss mean this is not yet a buy-the-dip regime. The institutional stance heading into mid-November is to maintain core BTC exposure sized for further ETF outflows, keep ETH underweight until the ratio and flows turn up, preserve optionality in SOL and regulated rails where inflows persist, and monitor ~$93-95k for BTC, ~$3.2k for ETH, and ~$0.93T for TOTAL3 as key stress levels.

- Capital rotated rather than evaporated; ETF beta bled while on-chain cash flows and policy momentum strengthened.

- The era of indiscriminate beta is ending, and the era of monetised pipes - stablecoins, tokenised funds, and exchange rails, has fully arrived.