Oct 20, 2025

From Flash Crash to Structural Re-Anchoring

Summary

- Liquidity Rebuilding Under Macro Stress: The market spent the week rebuilding liquidity following last week's $19B liquidation shock, all while global risk aversion was prolonged by persistent political headwinds (Trump's 100% tariff announcement and Beijing's retaliatory rhetoric).

- Dead-cat bounce: However, the crypto market saw a decent bounce on Sunday after Trump confirmed a meeting with China's President at the APEC summit on October 31st, providing a brief reprieve from trade uncertainty.

- Largest ETF Outflows Since Launch: BTC spot ETFs recorded a substantial -$1.23 billion in net outflows (the largest weekly redemption since launch, excluding the initial GBTC conversion). ETH ETFs followed at -$312M, while the Solana REX-Osprey vehicle posted +$14M, a small but symbolically important inflow.. These redemptions reflected hedging and risk control, not a structural exit.

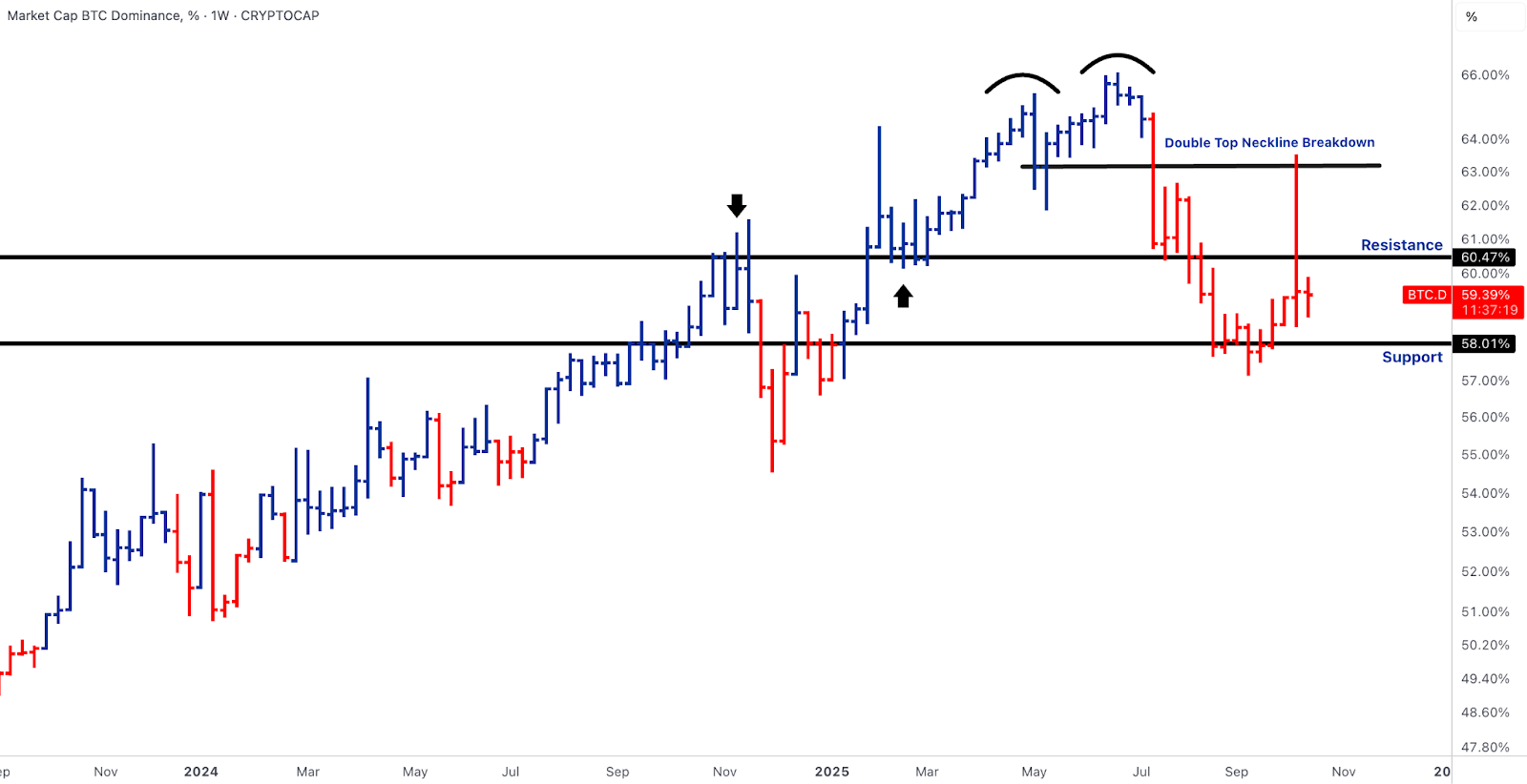

- Structural Bias Maintained Despite Drawdown: Despite the outflows, the TOTAL3 index (chart below) defended the $1 trillion base, and BTC Dominance remained capped below 60.5%, reinforcing that the altcoin rotation bias persists even amid drawdowns.

- Market Structure Reset: The market proved resilient as DeFi protocols cleared liquidations cleanly, and exchange liquidity was restored. The deleveraging phase is now evolving into a selective rebuilding phase led by structurally funded buyers rather than retail leverage.

- CPI Data Unlikely to Derail: Slew of key US macro figures due on Friday, including headline September U.S. CPI data (forecast at 3.1%) that is unlikely to trouble markets, as the Fed has not pushed back against the current aggressive rate cut expectations.

- Fed Rate Cuts Fully Priced: Markets are fully priced for a 25bps Fed rate cut this month and another in December, with rates expected to reach 3.0% by mid-2026.

- Earnings Season Boosts Sentiment: Market sentiment is being lifted by hopes for strong corporate earnings as the Q3 season kicks off with reports from giants like Tesla, Netflix, and major industrials.

BTC - Controlled Outflows, Structural Defence Intact

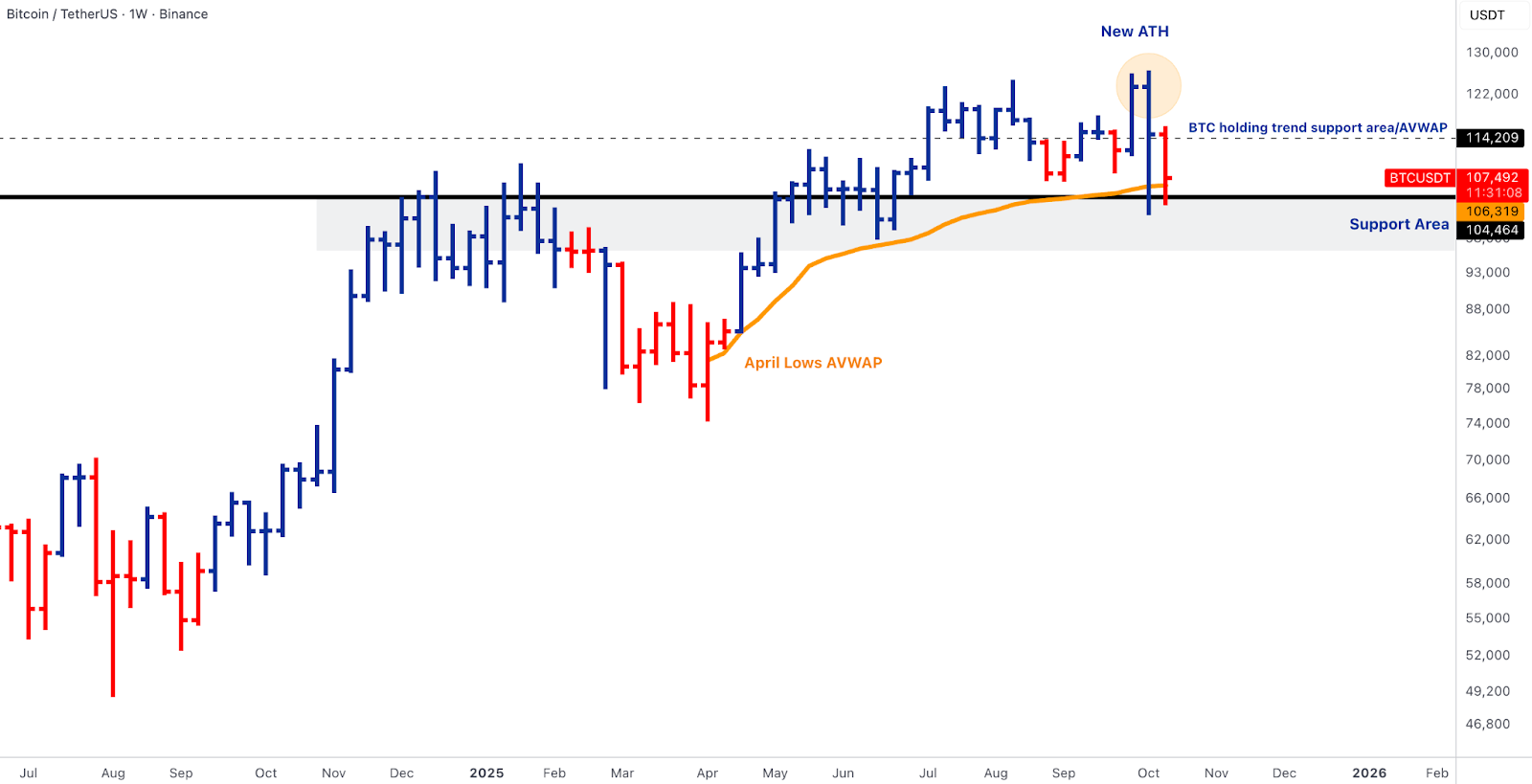

- BTC’s retracement to ~$107-109K found clear demand near the April lows anchored VWAP (~$106k), preserving the mid-cycle structure (chart below).

- The -$1.23B net ETF outflow was driven mainly by Valkyrie’s BRRR and Franklin’s EZBC redemptions, while IBIT and FBTC absorbed over 50% of the pressure, confirming that authorised participants remained active.

- CME open interest normalised to ~$8.5B, funding reset to 0%, and long-term holder supply declined by only 0.1%.

- On the supply side, Bitfarms upsized its offering to $500M to accelerate expansion ahead of the 2026 halving, signalling confidence in mining economics.

- The Binance $400M refund initiative also helped restore user trust, avoiding a repeat of last week’s liquidity freeze.

- Structurally, BTC continues to oscillate within a broad $104-126k range; losing $104k would invite a deeper retest into $96k, but as long as ETF redemptions decelerate, the higher-timeframe bias remains constructive.

- Regaining $114-116k opens the path back toward $126-128k. The higher-timeframe bias stays constructive as long as ETF redemptions decelerate.

ETH - ETF Rotation Re-Emerges

- ETH mirrored BTC’s retracement but retained composure. ETFs logged -$312M in weekly outflows, a moderation versus prior weeks’ capitulation, led by small redemptions in ETHA and FETH mid-week before partial recovery by Friday.

- The ETH/BTC ratio (chart below) stabilised around ~0.037, with short-term support forming at 0.034, keeping the broader basing structure alive.

- Fundamentally, ETH’s ecosystem tone improved: Bitmine added $417M in new holdings, maintaining its lead among corporate stakers. The Ethereum Foundation deployed 2,400 ETH through Morpho, continuing DeFi integration. Meanwhile, Asia’s largest ETH backers announced a $1B Treasury fund, marking a coordinated regional accumulation push.

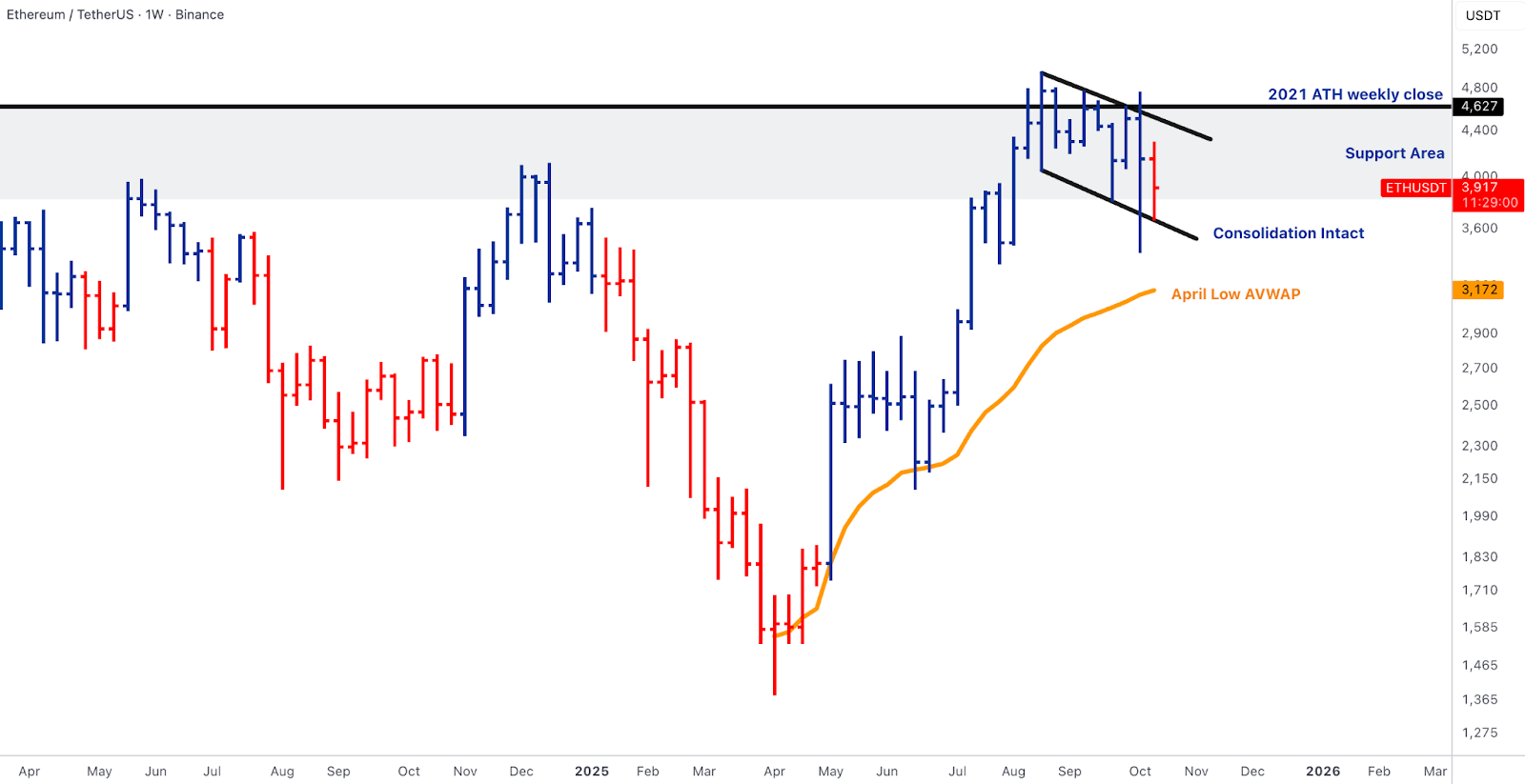

- Technically, ETH continues to consolidate between $3,600-4,630. The April-low VWAP near $3,170 defines deep structural support; a reclaim of $4,627, the 2021 ATH weekly-close band, would confirm leadership rotation back from BTC. For now, relative stability amid outflows signals robust on-chain demand absorption.

SOL & BNB - ETF Optionality and Exchange Strength

- SOL remained the key beta gauge. After last week’s ~23% intraday drawdown, SOL recovered to ~$188, still below its $200-210 inflexion band (chart below).

- The first dedicated Solana ETF, REX-Osprey, recorded +$14 million in net inflows, the only positive primary-creation print among major L1s.

- Catalyst momentum continued:

- a16z Crypto’s $50M investment in Jito fortified validator-economy depth;

- Jupiter DEX’s Ultra v3 launch introduced MEV protection and gasless transactions, improving trade execution quality;

- A Solana treasury vehicle added 5 % to holdings at ~$110 average, demonstrating institutional conviction.

- Technically, reclaiming $210 would restore momentum; holding above $170 signals absorption strength.

- BNB, meanwhile, extended its outperformance, closing above $1,090, maintaining the psychological $1k handle (chart below).

- Exchange fee capture and perpetual-volume share rose ~7% WoW. The firm’s European custody alliance with Standard Chartered and PayPay’s 40% stake in Binance Japan have reinforced regulatory durability.

- Together, SOL and BNB remain breadth thermometers: their stability indicates that internal market structure is rebuilding, not breaking.

Emerging Rotation Leaders - The Alpha Cluster

- The week’s top performers reflected a pivot toward utility-backed and post-depeg recovery trades.

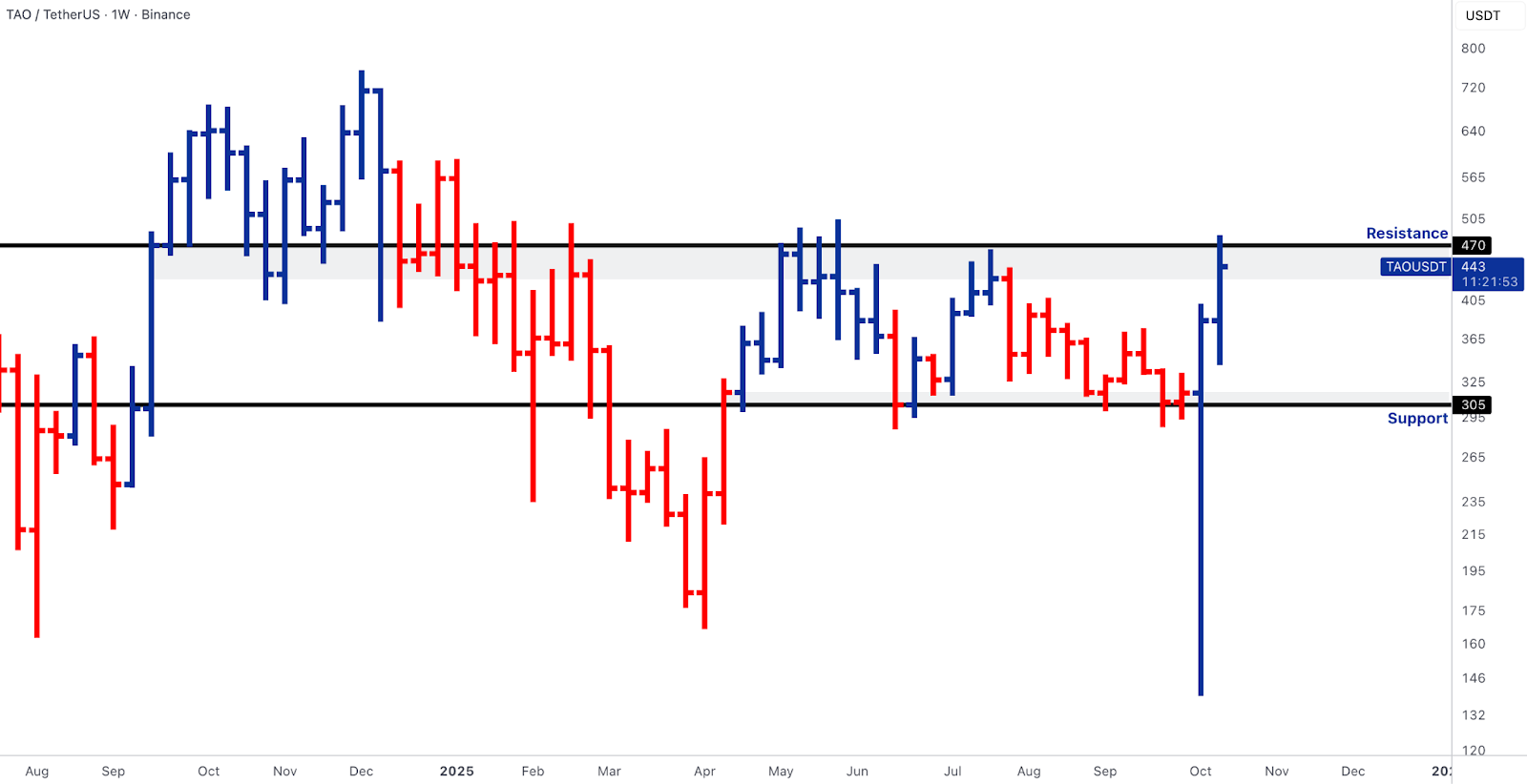

- TAO (Bittensor) surged after its treasury announced $11M in cross-network synergies and new subnet deployments. The weekly chart (below) shows a breakout through $400-470 resistance, confirming structural leadership.

- ENA (Ethena) rebounded after the full USDe re-peg and enhanced hedging via Morpho. ENA defended the $0.44-0.49 support zone (see chart below), transitioning from recovery to momentum asset.

- CRV (Curve), CFX (Conflux), and THETA rose on short covering and selective rotation into DeFi and Asia-layer names.

- The key differentiator this week: structural cash flow and utility. Tokens with sustained on-chain revenue (TAO, ENA, CRV) attracted liquidity far faster than high-beta plays, suggesting that rotation is again rewarding quality balance-sheets, not leverage.

Rails & Productisation – Tokenisation Marches On

- Infrastructure headlines offset last week’s deleveraging.

- BlackRock confirmed plans for a Genius-compliant money-market fund tailored for stablecoin issuers.

- Japan’s mega-banks announced a joint stablecoin network to accelerate corporate payments.

- OpenEden’s T-Bill fund earned an S&P AA rating, marking a milestone for tokenised treasuries.

- Meanwhile, Kraken acquired a smaller exchange to expand regional coverage; OKX and Standard Chartered launched a custody alliance for off-exchange collateral.

- Ondo Finance completed its Oasis Pro acquisition, bridging RWAs and securities.

- The RWA-finance-to-public-markets arc now looks inevitable, Securitise’s planned $1B SPAC underscores it.

- These developments collectively reinforce that the structural thesis for digital assets, interoperable collateral, regulated custody, and tokenised yield, is deepening, irrespective of price volatility.

Outlook - Fragile Rebuild, Institutional Floor

- Week 16 closed with a message of resilience over exuberance.

- The ETF channel turned negative (BTC -$1.23 B, ETH -$0.31 B), but prices stabilised at structural supports.

- Liquidity is being rebuilt from the bottom up, not by leverage, but by cash buyers and re-collateralised protocols.

- TOTAL3’s ~$1T base, BTC.D below 60%, and ETH/BTC holding ~0.034 collectively imply a foundation for a measured rotation, once the ETF prints normalise.

- Macro catalysts ahead, tariff enforcement, delayed macro data, and U.S. budget clarity will determine whether this rebound evolves into sustained rotation.

- China's GDP data on Monday morning beat the forecast, lending support to risk assets including stocks and crypto. Markets are hoping for more stimulus coming out from China's fourth plenum as policymakers meet this week to discuss its five-year plan.

- A slew of US macro figures is due on Friday, including headline U.S. CPI data that is expected to be held at 3.1% in September, but should not derail the Fed from further rate cuts

- Markets have fully priced in a 25bps easing this month, and another in December, with rates seen reaching 3.0% by the middle of next year.

- Hopes on solid earnings also helped lift market sentiment, a few key giants including Tesla, Ford, GM, Netflix, Procter & Gamble, Coca-Cola, RTX, IBM and Intel.

- For now, the system has absorbed the largest liquidity fracture ever without apparent contagion.

- Institutions are no longer the weak link; they are the circuit breaker.

Thanks for reading this week's Market Pulse.

We’re watching flows in real time. If you want early alerts, customised sizing analysis, or routing paths for your trade, we’re here to help you execute on your strategy.

Get in touch with your Relationship Manager.

- The Hex Trust Markets Team

Oops! Something went wrong while submitting the form.