Nov 3, 2025

Rotation pauses, rails build, liquidity compresses at the long end

Market Overview

- "Hold-and-Build" Week: The market saw a stabilising week last week, focused on consolidation rather than a decisive breakout or breakdown.

- Altcoin Breadth Intact: The TOTAL3 index held its rising trendline around $1 trillion, keeping breadth intact while BTC.D stalled near ~60% resistance, signalling no decisive shift back to BTC leadership.

- Liquidity Preserved by Fed: Fed’s 25 bps rate cut and 10-year Treasury yield easing ~7 bps WoW to ~4.08% compressed real yields and preserved liquidity conditions for risk, but the market still demands tangible cash-flow stories.

- AI Investment Reaffirmed: Macro attention swung back to AI spending and financing. Mega-cap earnings (NVIDIA, Microsoft, Google) reaffirmed large, front-loaded investment cycles in AI and data-centre infrastructure: NVIDIA’s supply-chain pull-through remains intact; Microsoft and Google expanded multi-year opex and data-centre capex.

- Sustainable Financing Model: Crucially, these mega-cap outlays are being financed not by leverage blow-outs but through record free-cash flow, opportunistic equity issuance, and still-open IG/convertible markets, a late-cycle posture of “invest through slowdown”.

- Selective Digital Asset Liquidity: For crypto, this trend means liquidity is selective, favouring real cash-flow rails (stablecoins, staking, tokenised treasuries) and transparent ETF pipelines where capital transmission is visible and risk-managed.

- ETF flows captured the divergence clearly: BTC ETFs saw ~$799M of net outflows, ETH ETFs posted a muted $16M inflow, while SOL ETFs drew $199M in their debut week, capital rotating within the system, not exiting it. The regime remains one of rotation hold, not renewed impulse.

- Trade Truce Doubts & China Miss: Investors are digesting the US-China year-long trade truce, but doubts about its durability persist. Geopolitical anxiety is compounded by China's PMI data missing expectations.

- US Data Vacuum Continues: The ongoing US government shutdown will continue to delay critical labour market figures, including Nonfarm Payrolls and job openings data.

- Earnings Season Takes Spotlight: With macro clarity scarce, market focus remains squarely on the Q3 earnings season, driven by a slew of major tech firms reporting this week.

BTC - AVWAP holds, ETF outflows contain downside

- BTC defended its April-lows AVWAP around $106.7k and consolidated between $107-114k (chart below).

- Despite –$799M in ETF net outflows, the tape showed structural resilience; the outflows were largely profit-taking from legacy holders, not mass redemptions. Authorised participants kept the creation/redemption window fluid, preventing dislocations.

- On-chain, miners remained steady: Riot posted $104.5M Q3 net income, reversing losses, while hashrate expansion slowed, tempering new supply.

- Liquidity metrics point to restored two-way depth post-October’s volatility, and funding normalised near flat. The map is unchanged: immediate support $106-107k, potential buyers found down to ~$104k, pivot $114-115 k, resistance $126-128 k. BTC leadership persists but remains capped by the ~60 % BTC.D ceiling.

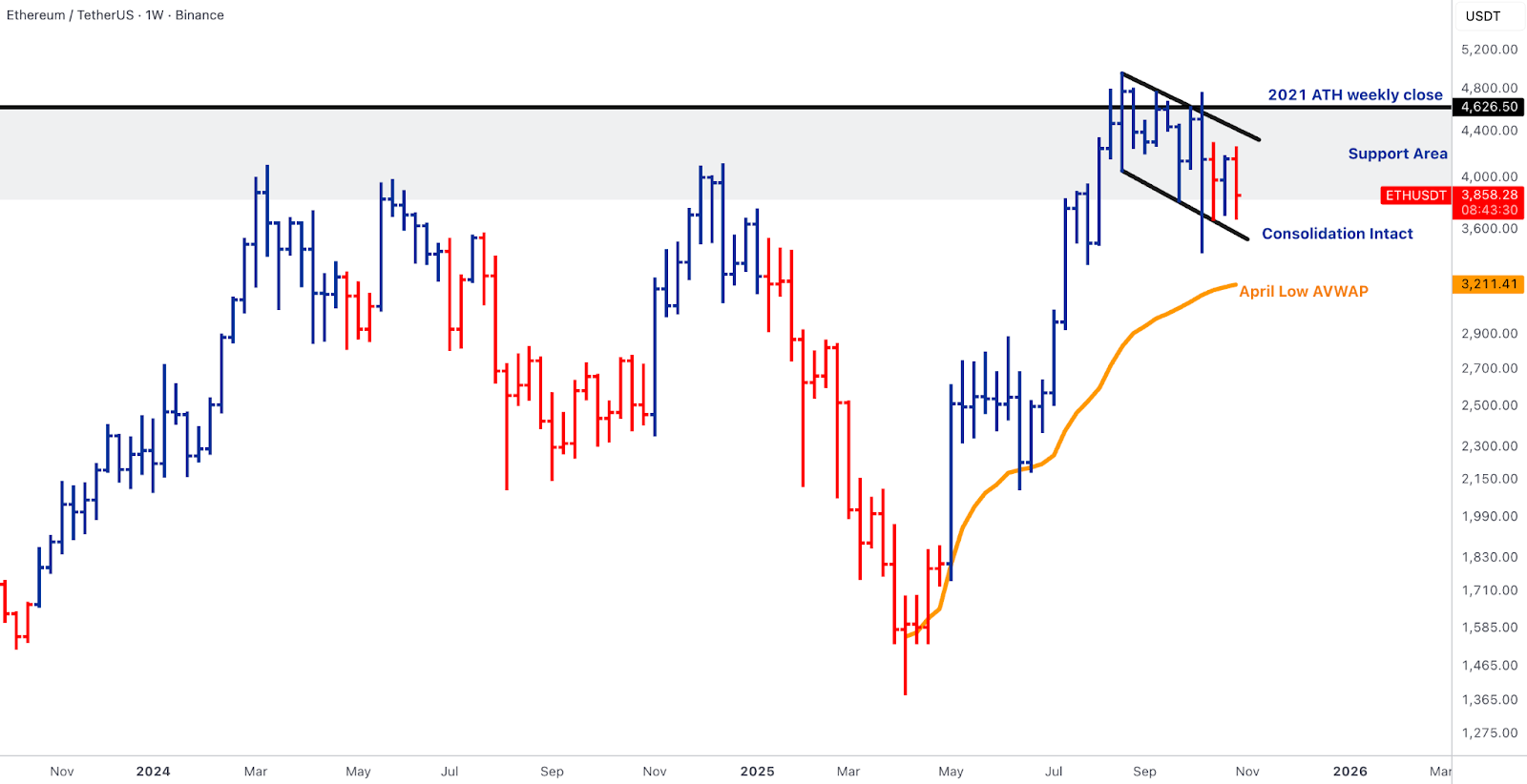

ETH - Flows stabilise, technical base intact

- ETH ETFs eked out $16M in net inflows, a neutral print that nonetheless signals the return of passive demand after prior weeks’ redemptions.

- Price tested $3,800 support, undercut $3,600 briefly, and recovered to close mid-range (chart below). The Fusaka upgrade is locked for 3 Dec, with testnets fully activated, renewing developer focus after a quiet quarter.

- Ecosystem data stayed firm: Sharplink deployed $200M in ETH on Linea, Bitmine added 27,000 ETH to corporate holdings, and Aave’s loan book exceeded $25B, reinforcing Ethereum’s centrality to on-chain credit.

- The ETH/BTC ratio at ~0.034 remains the tactical hinge: defend it and ETH can re-target 0.039-0.04 into Fusaka; lose it and BTC resumes dominance. Structure intact; leadership deferred.

Solana & BNB - Structural bid vs. technical cooling; rails keep broadening

- The SOL spot ETFs landed as advertised: ~$199M net inflows in a four-day debut, healthy day-two volumes, and a clear institutional footprint.

- Price, however, slipped below the ~$202 support, respecting its trendline break and telegraphing that ETF demand is stabilising flows, not yet dictating price.

- The constructive read is simple: the ETF pipe is now “on,” so any improvement in risk tone or breadth can transmit faster to SOL than pre-ETF.

- BNB held above $1,000 after its late-summer breakout, with rails headlines (e.g., Western Union’s WUUSD trademark timing after announcing a 2026 Solana-based stablecoin, Ondo’s expansion on BNB Chain) reinforcing BNB’s role as a toll token for high-throughput consumer rails. Both improve the base case that fee-generating networks retain bids during carry compression.

Emerging Rotation Leaders - Functionality Over Hype

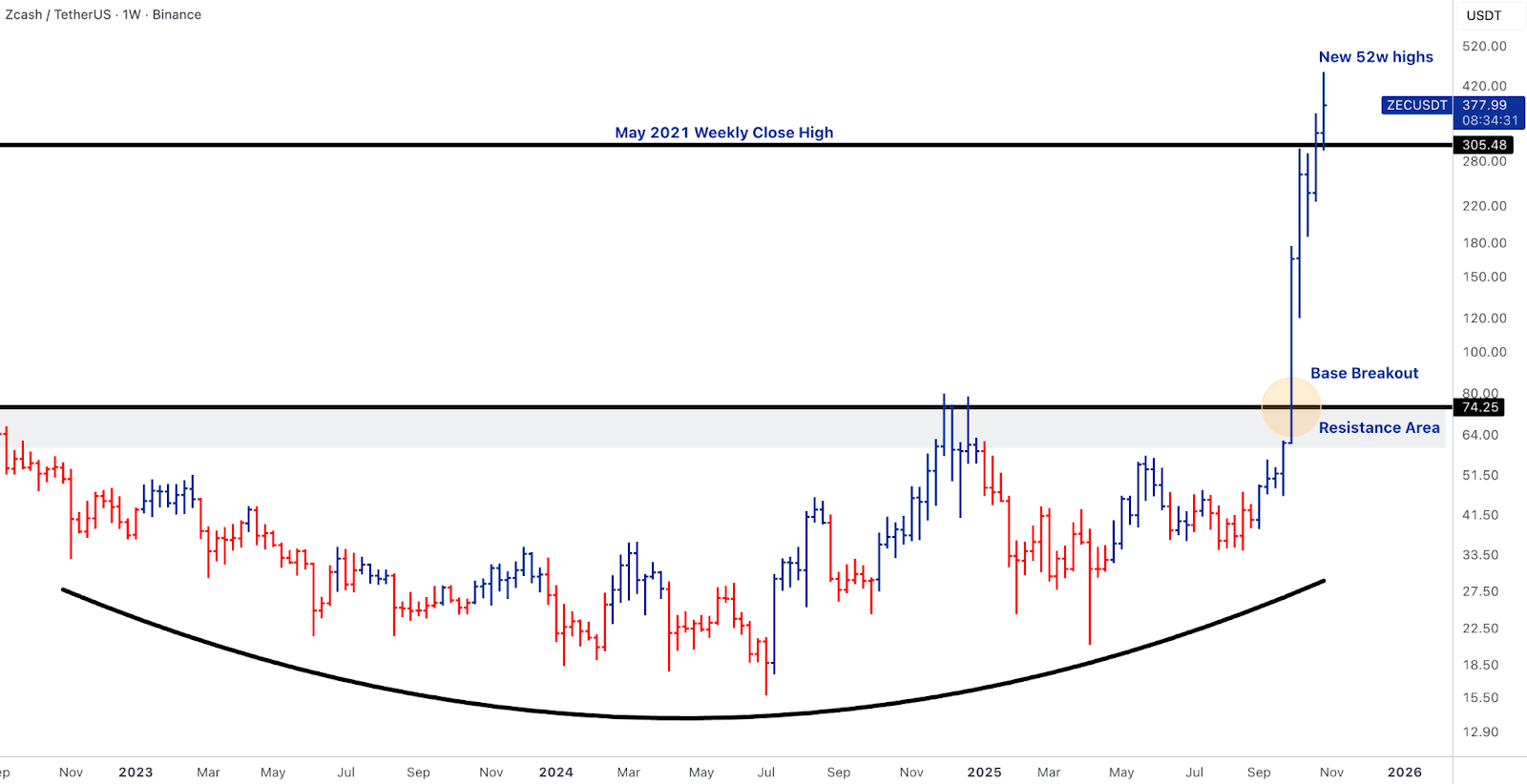

- Zcash (ZEC) extended its base-breakout toward new 52-week highs (~$380) after ECC published its Q4 roadmap, and attention re-focused on the surge in shielded supply. The story works because privacy liquidity is scarce and ZEC has the cleanest listed exposure, but momentum now sits far above the breakout band (~$74-85), so trailing-risk management is key.

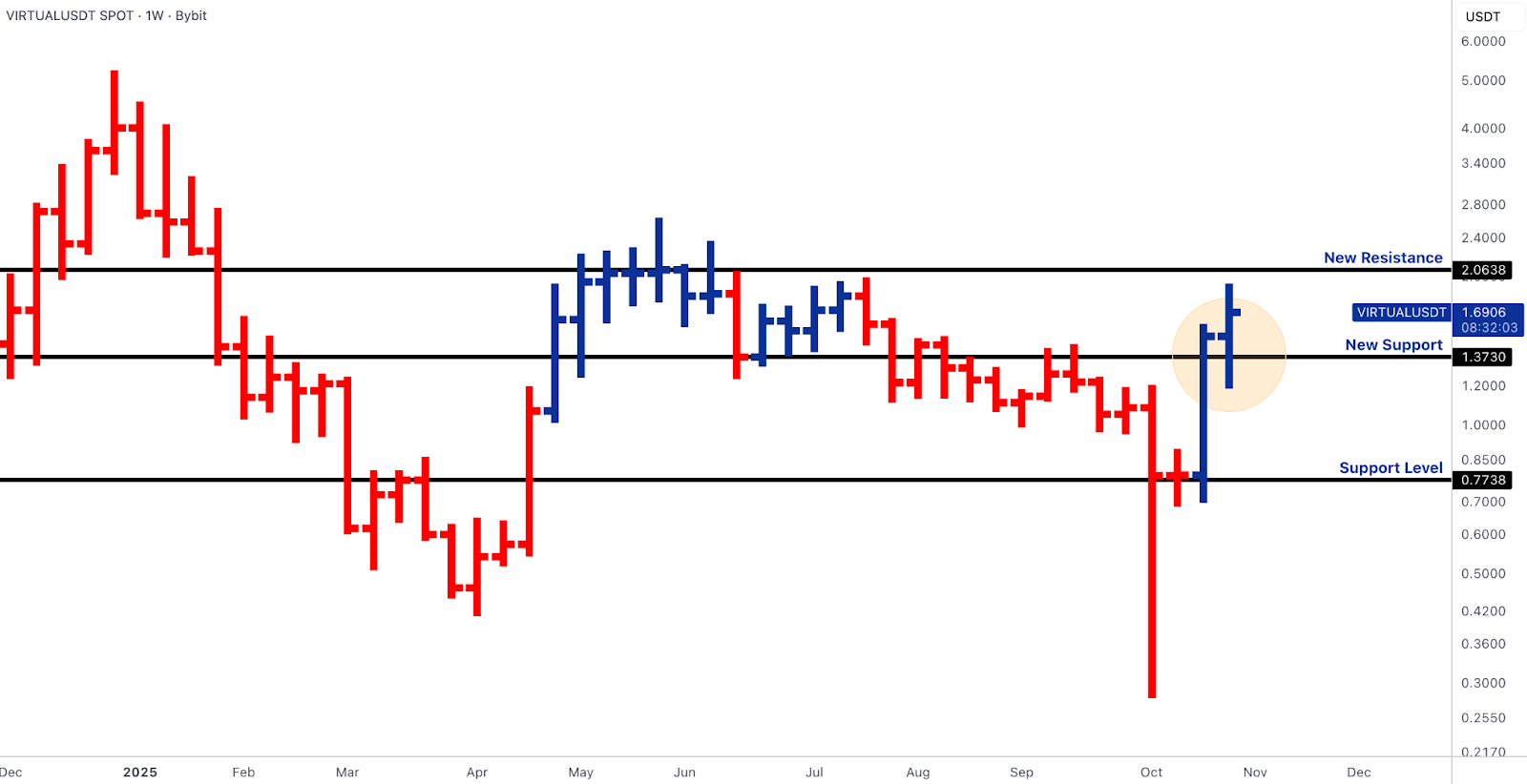

- Virtuals Protocol (VIRTUAL) flipped its structure back above ~$1.37, creating a new support with resistance near ~$2.06, holding sustained strength post-Bybit integration, as speculative AI flows consolidated into actual-usage networks.

Rails, Stablecoins & Tokenisation - Profit pools consolidate and distribution widens

- The revenue map keeps concentrating on where cash flows are real.

- Tether’s annual profit run-rate north of $10B underscores the “stablecoin seigniorage + T-bill carry” moat, while new distribution commitments continue.

- Visa is onboarding more stablecoins across four chains.

- Western Union is positioning for a Solana stablecoin in early 2026.

- Canada’s federal framework update and Japan’s JPYC launch add sovereign scaffolding.

- Circle’s ARC testnet (with institutional participants) and Securitise’s SPAC path speak to tokenised treasuries and compliant rails moving into mainstream capital-markets plumbing.

- Banks aren’t absent either: J.P. Morgan progressed on-chain fund-servicing and separately highlighted USDT/USDC growth, which matches the week’s flow reality, stablecoin issuers are now the dominant daily protocol earners.

- The through-line: rails monetisation is active now, ETF monetisation is passive but powerful, and both pipes grew sturdier last week.

Outlook

- This was a liquidity-conserving, rails-advancing week.

- Rates eased modestly, the Fed delivered the cut, and mega-caps validated multi-year AI spend while showing public-market capacity to finance it.

- That mix doesn’t force a chase, but it funds pipes, and the data show those pipes are exactly where crypto’s cash flows now concentrate: stablecoin issuers’ profits, tokenisation rails, and spot ETF demand.

- With TOTAL3 holding trend and BTC.D capped, the blueprint through November remains:

- Own the monetised pipes (stablecoins, tokenised treasuries, staking/exchange rails).

- Trade BTC between AVWAP support and the $114-115k pivot, and let confirmed ratio/ETF signals dictate ETH/SOL adds.

- The SOL ETF launch proved institutional capacity exists; the next leg depends on ratio confirmation and BTC.D rejection rather than macro alone.

- Investors will be digesting developments from last week, including the central bank meetings and the US-China year-long trade truce. But doubts remain on its long-term durability, adding to geopolitical uncertainty.

- Markets will also be accessing the macro data from China, as the China PMI data came through Monday morning missing expectations.

- The ongoing US government shutdown will continue to delay key labour market figures, including Nonfarm Payrolls and job opening data.

- Earnings Season Takes Spotlight: With macro data scarce, market focus remains squarely on the earnings season, as a slew of major tech firms are set to report results this week.

Oops! Something went wrong while submitting the form.