From CPI Relief to Flow Reality: Beta Fragile, Plumbing Compounding

Blueprint - (breadth, rotation, macro-to-crypto transmission)

Key Points

- Key facts: The week stayed in risk-repair mode: macro volatility (AI valuation debate + growth vs “old economy” rotation) pressured positioning early, but Friday’s equity rebound translated into a mild crypto bounce rather than a regime shift. CPI landed notably non-hawkish in headline terms (0.2% m/m; 2.4% y/y), keeping the “rates aren’t re-pricing higher” channel intact, even as risk premia remained elevated.

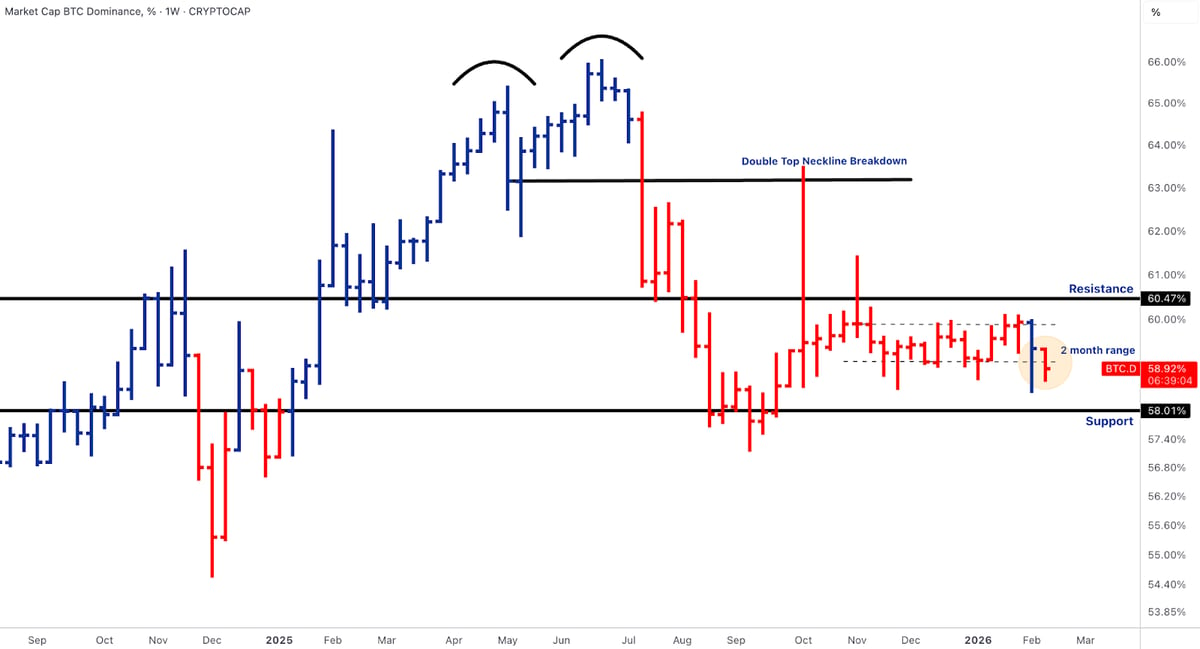

- Market structure: BTC.D remains the cleanest “who leads?” tell, as dominance is still range-bound (~58-60.5%), although it ended the week outside its 2-month range (on a closing basis), which may imply a retest of ~58% support level. TOTAL3 is the bigger scar: the drawdown sits on/through the marked support band (~$760B) with the wick probing toward the April ’25 lows (~$658B), i.e., alts are prone to keep trending lower without a recovery of its support area that could imply potential consolidation.

- This was a liquidity and positioning week more than a “new narrative” week: macro stopped tightening at the margin (yields down post-CPI), but crypto’s internal plumbing (ETF redemptions, leverage cleanup, selective rails adoption) still dominated. The tape is saying: beta is fragile, but rails are compounding, so the highest-quality way to express conviction is via levels and flow thresholds, not blanket directional exposure.

BTC (structure, miner reflexivity, spot ETF transmission)

- BTC saw weekly net outflows of -$360M - Daily: Mon +$144.9M; Tue +$166.5M; Wed -$276.3M; Thu -$410.2M; Fri +$15.1M.

- BTC is pinned below the marked resistance/overhead supply with the prior acceptance zone near ~$89.8k-$93.0k (AVWAP band) and the higher pivot at ~$104.5k. Spot is currently printing ~$68.9k, just below the support area, which may indicate potential for further downside.

- Miners & reflexivity: The week’s large negative difficulty adjustment matters because it typically signals a hashrate shock/profitability squeeze that can reduce marginal sell pressure over the next adjustment window, but in the near term, it’s also a reminder that stress is real inside the production complex (which tends to correlate with fragile price floors when leverage is high).

Our take: BTC is trading like an ETF-mediated risk asset again: green days require actual creations, while selloffs accelerate when redemptions meet thin bid depth. The tactical tell for stabilisation is simple: two consecutive creation days with price holding the support band; without that, rallies tend to fade into the $89-93k supply on any reflex bounce.

ETH (ETF flows, ETH/BTC compression, “base layer vs L2” narrative shift)

- ETH saw weekly net outflows of -$161.2M. Daily: Mon +$57.0M; Tue +$13.8M; Wed -$129.1M; Thu -$113.1M; Fri +$10.2M.

- ETH is printing ~$2.0k, decisively below the marked support shelf and under the June ’22 low AVWAP (~$2,375) with the next meaningful overhead reference at the April low AVWAP (~$3,092).

- ETH/BTC is at ~0.029, just below the 0.03 support area. A reclaim/acceptance above would favour ETH outperformance; significant work is needed to clear upper resistance levels:(main ~0.0398; interim ~0.0354).

- Protocol posture: The week’s discourse shift toward making Ethereum mainnet the center of gravity again (and pushing back on “copy-paste L1 sprawl”) is important, but it’s not price-supportive unless it converts into fee density + sustained demand. In this tape, narratives don’t lift ETH; flows + ratio structure do.

Our take: ETH remains the market’s balance-sheet stress barometer: when ETH can’t hold key AVWAP references and ETH/BTC is heavy, the path of least resistance is “alts underperform, rallies are tactical.” ETH needs ratio stabilisation (hold ~0.03) as well as ETF bleed slowing, before you can credibly call a broader rotation.

SOL & BNB (leadership gauges, beta containment, “alts aren’t equal”)

- SOL: SOL is printing ~$87, after losing the ~$112-114 “new resistance / Jan ’23 AVWAP” zone. The key read is that the prior leadership structure has flipped: rallies back toward ~$112-114 are now tests, not breakouts, unless the market re-accepts above that shelf.

- SOL saw weekly net outflows: +$12.6M (small but positive). Daily totals: Mon $0.0M; Tue +$8.4M; Wed $0.0M; Thu +$2.7M; Fri +$1.5M.

- BNB: BNB is printing ~$619, after rejecting hard from the prior breakout zone ~$742, with the next “story level” still $1,000 overhead. The constructive element is that BNB historically stabilises earlier than high beta alts when exchange-linked cashflows/rail narratives stay intact, but this week’s candle says risk is still de-grossing first, asking questions later.

Our take: SOL/BNB are now tactical beta instruments until TOTAL3 repairs. The market will pay you to be patient: the “good” entry regime is support defended + ETF/spot demand returning, not catching knives through broken shelves.

Alpha Cluster (UNI, AAVE, HYPE, ZRO) - catalyst first, then structure

- UNI caught a structural bid on the back of direct on-chain access to institutional tokenised cash products, effectively turning the DEX layer into a distribution rail rather than a pure retail venue; in this tape, that’s why UNI can outperform even when beta is fragile, it’s a plumbing winner.

- AAVE benefits from the same regime: as tokenised collateral and stablecoin settlement rails expand, Aave increasingly trades like DeFi’s balance-sheet utility, which is why the market is willing to entertain wrapper/vehicle conversations around it despite cyclical drawdown risk.

- HYPE remains the purest expression of the CEX-like experience on-chain, the key is that volumes and product breadth (including non-crypto perps proxies) keep pulling liquidity into a single venue, and that liquidity concentration is exactly what the broader market is lacking right now.

- ZRO saw tangible distribution/strategic validation: the story moved from “messaging layer” to “institutional adoption vector,” with high-profile strategic capital reinforcing LayerZero’s positioning as an interoperability primitive that can sit underneath tokenised products and cross-venue settlement.

Rails & Productisation (stablecoins, tokenisation, regulatory plumbing)

- Key facts: The week reinforced that “rails” are the durable bull case even when price is volatile: stablecoin and tokenisation initiatives kept stacking (bank-adjacent tokenised bonds, on-chain settlement integrations, and tokenised cash products moving closer to native DeFi connectivity). At the same time, regulatory process risk remains live (stablecoin/bank perimeter debates; market structure still messy), but directionally, the plumbing is being built.

Our take: The investable takeaway is that rails adoption is decoupling from beta. In drawdowns, this shows up as relative strength in tokens with cashflow/usage hooks (e.g. UNI/AAVE/HYPE/ZRO-type exposures) while TOTAL3 bleeds. That is the cleanest expression of how institutionalisation continues even when the price structure breaks.

Outlook

Key Points

- Next week is about inflation follow-through and growth prints: the market will trade on whether disinflation can continue without growth breaking (see PCE, GDP prints, flash PMIs and Industrial Production/Durable Goods). Any upside inflation surprise would hit duration-sensitive tech again and spill into crypto via risk premia; any downside surprise could support the “yields lower / risk repair” channel, but only matters for crypto if it converts into ETF creations rather than a one-day bounce. The release of Fed Minutes may provide clues into supportive rate expectations.

- Downside macro surprises must be interpreted carefully. A mild cooling in data would support liquidity relief, while anything more may start invalidating the soft-landing narrative and pressure risk across the board. Current data does provide much indication of the latter, but sensitivity to data dispersion is elevated given high valuations.

- For crypto specifically, ETF flow stabilisation remains the most immediate leading signal. Infrastructure expansion provides medium-term ballast, but near-term structure remains flow-driven.

Thanks for reading this week's Market Pulse.