Selective Rotation Persists as Rails Advance and Beta Consolidates

Regime, Flows & Macro Context

TL;DR / Key Points

- Market remains in a late-cycle, selective risk regime, with capital rotating internally rather than expanding aggregate beta.

- BTC dominance continues to trend lower following the prior double-top resolution, but is consolidating rather than accelerating downside.

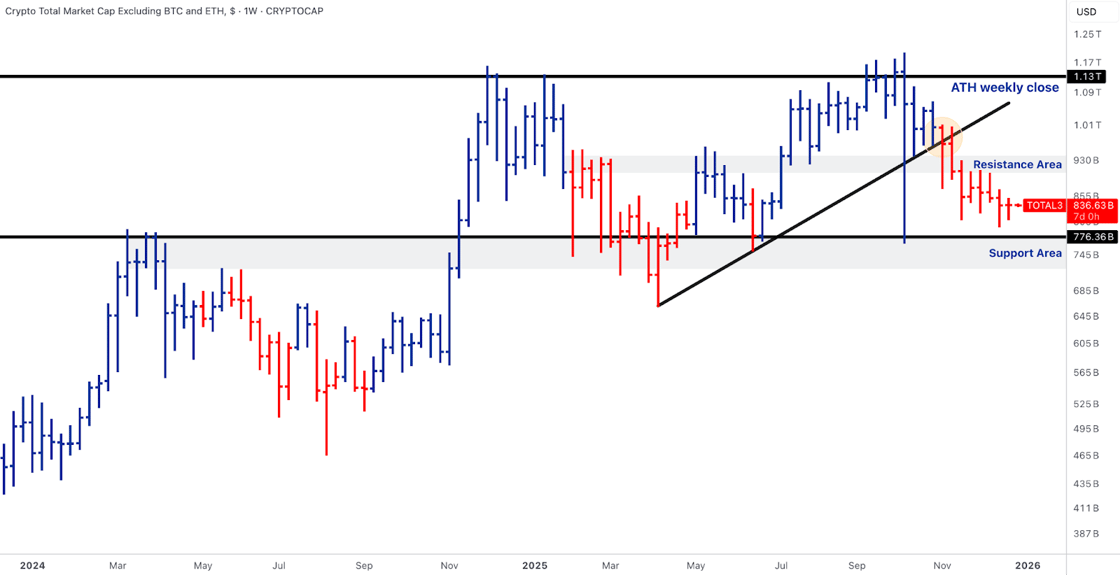

- TOTAL3 failed to hold near prior ATH weekly closes and is digesting gains, yet structural higher lows remain intact.

- ETF flows were seasonally soft and choppy, consistent with year-end liquidity conditions rather than structural de-risking.

- Macro tone remained non-disruptive, with no new data shocks into low-liquidity holiday trading.

ETF flows

- BTC: Net outflows across multiple sessions, with redemptions concentrated into holiday-thinned liquidity.

- ETH: Continued modest outflows, stabilising toward week-end but still reflecting consolidation rather than accumulation.

- SOL: Low-magnitude, mixed flows, consistent with consolidation rather than loss of structural interest.

Macro context

- No major US macro releases materially altered rate or growth expectations.

- Cross-asset performance favoured equities and precious metals, while BTC sat out the seasonal Santa-rally dynamic.

Our take: The trading week reinforced the ongoing grind-and-digest regime rather than a regime shift. With macro catalysts largely absent and liquidity thinning into year-end, price action was governed by relative positioning and product flows rather than fresh information. The key signal remains internal: infrastructure, rails, and regulatory clarity continue to advance even as prices consolidate. This divergence between fundamentals and price is characteristic of late-cycle markets transitioning from beta-led to structure-led returns.

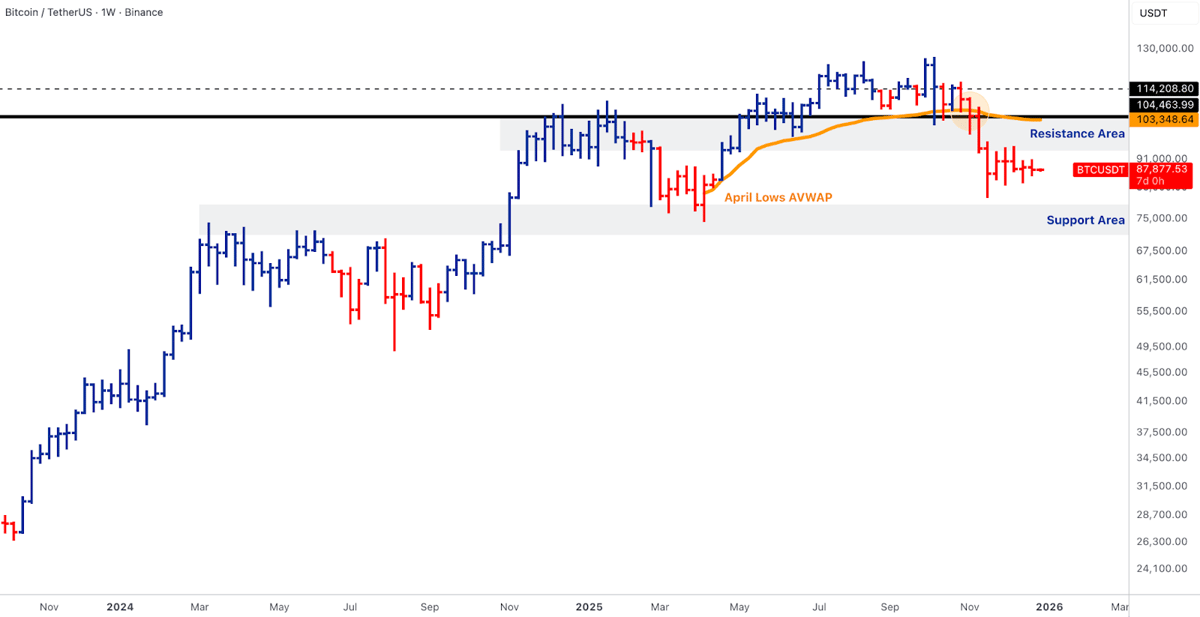

Bitcoin (BTC) - Consolidation Below Resistance

- BTC was rejected at the ~$103-105k resistance zone, with the April-lows AVWAP now broken and acting as upper-range resistance.

- Price continues to hold above the $75-80k structural support band, preserving long-term trend integrity.

- Spot ETF flows were negative but orderly, with no evidence of forced selling or miner stress.

- BTC dominance is consolidating rather than reasserting leadership.

Our take: BTC is functioning as a balance-sheet asset, not a momentum driver. The rejection at resistance caps upside near-term, but the absence of breakdown below structural support argues against distribution. In this regime, BTC’s role is to anchor portfolios while capital selectively migrates toward relative-strength expressions elsewhere in the complex.

Ethereum (ETH) - Relative Structure Still Intact

- ETH remains below the 2021 ATH weekly close (~$4.6k), defining the next macro validation level.

- The April-lows AVWAP near ~$3.2k remains the key pivot; price is consolidating just below it.

- ETH/BTC continues to hold above its long-term breakout region (~0.025), despite short-term consolidation below ~0.035.

- ETF flows were soft but showed signs of stabilisation late in the week.

Our take: ETH continues to express structural relative strength, even as the absolute price consolidates. The ETH/BTC breakout remains the most important signal: it reflects a willingness to rotate down the crypto risk curve without broad speculation. As long as ETH holds above its breakout band on a relative basis, the medium-term bias remains constructive despite near-term range-bound price action.

Solana & BNB - Leadership Digestion

Solana (SOL)

- SOL failed to sustain momentum above the ~$200-205 resistance zone.

- Price is testing trend support while remaining above the January 2023 lows AVWAP, preserving long-term structure.

- No adverse ecosystem or regulatory headlines during the week.

Our take: SOL’s pullback reflects trend digestion, not thesis failure. In selective-risk regimes, SOL behaves as a volatility amplifier: strong in expansion phases, corrective during consolidation. Structural support remains intact, keeping SOL positioned as a leadership candidate when risk appetite re-engages.

Binance Coin (BNB)

- BNB rejected near the $1,000 psychological level.

- The prior breakout above ~$740 remains structurally valid.

- No exchange-specific or regulatory shocks emerged this week.

Our take: BNB continues to trade more like a cash-flow and platform proxy than a speculative asset. The pullback reflects valuation digestion rather than loss of confidence, with structure remaining intact above the breakout zone.

Selective Rotation Beneficiaries

- Canton (CC): Benefited from rails-adjacent rotation into permissioned and enterprise blockchain narratives, amplified by thin liquidity rather than a discrete catalyst.

- Zcash (ZEC): Advanced as shielded supply holding near ~23% reinforced sticky privacy adoption amid a less hostile regulatory tone.

- Dash (DASH): Likely participated via sympathy with the privacy basket rather than protocol-specific developments.

- Toncoin (TON): Continued to consolidate around 2023 lows on Telegram-ecosystem monetisation and distribution momentum.

- Tezos (XTZ): Saw catch-up flows as Tezos’ EVM-compatible Layer 2, Etherlink, activated its Farfadet upgrade on 22 December. The upgrade doubled its chain capacity to 1,000+ native transfers per second while maintaining sub-cent fees. Most importantly, fast withdrawals were reduced from 15 days to under a minute, critical for DeFi traders and gamers.

Our take: This week’s outperformers underline a market expressing views through niche utility, regulatory asymmetry, and distribution reach, rather than broad alt-beta. These are rotation signals, not the start of a generalised alt-cycle.

Rails & Productisation - Infrastructure Outpaces Price

- Regulatory clarity continued to advance globally, with Asia, the UK, and emerging markets formalising crypto rulebooks and licensing frameworks.

- Tokenisation momentum accelerated, with institutions and market infrastructure providers positioning for on-chain settlement and securities issuance.

- Stablecoin narratives remained front-and-centre, spanning ratings frameworks, bank-adjacent issuance, and embedded distribution channels.

- Institutional rails expanded across custody, interoperability, and compliant DeFi access.

Our take: Rails are compounding quietly beneath price. From regulatory scaffolding to tokenised securities and stablecoin distribution, the stack required for institutional adoption continues to solidify. This divergence, muted prices alongside accelerating infrastructure, is characteristic of durable adoption cycles and argues for patience and selectivity rather than momentum chasing.

Outlook

- Attention shifts to early-January macro data, where inflation and activity prints will reset real-rate expectations.

- Liquidity conditions are expected to improve post-holiday, potentially reactivating suppressed flows.

- Relative-value and structure-led trades remain favoured over directional beta.

Our take: Holiday trading is marking a pause rather than a pivot; the setup into the new year remains one of internal rotation over headline moves. If macro data cooperates and liquidity normalises, the disconnect between advancing rails and consolidating prices may begin to close. Until then, disciplined positioning around structure, flows, and validated themes remains the optimal approach.