Deleveraging bites, institutional rails refuse to blink

TL;DR / Key Points

- BTC dipped to $80k, stabilising above $83k; ETH lagged on USD and BTC ratio

- ETF redemptions remained heavy. BTC >$300M headline days; ETH outflows smaller

- SOL ETF inflows persisted (~$130M), BNB treasuries continued accumulation

- Institutional & policy rails strong: OCC, Japan, tokenised ETPs, corporate treasuries acting opportunistically

- Key desk questions: Can ETF outflows stabilise? Will BTC hold $80–85k stress floor without another liquidation cascade?

Our Take:

The market is still in controlled deleveraging. Flow stress is real, but the institutional footprint and regulatory clarity provide a floor, not panic.

Market Overview - Deleveraging vs. Institutional Entrenchment

- Last week was marked by mechanical deleveraging on the markets while institutional activity remained steady.

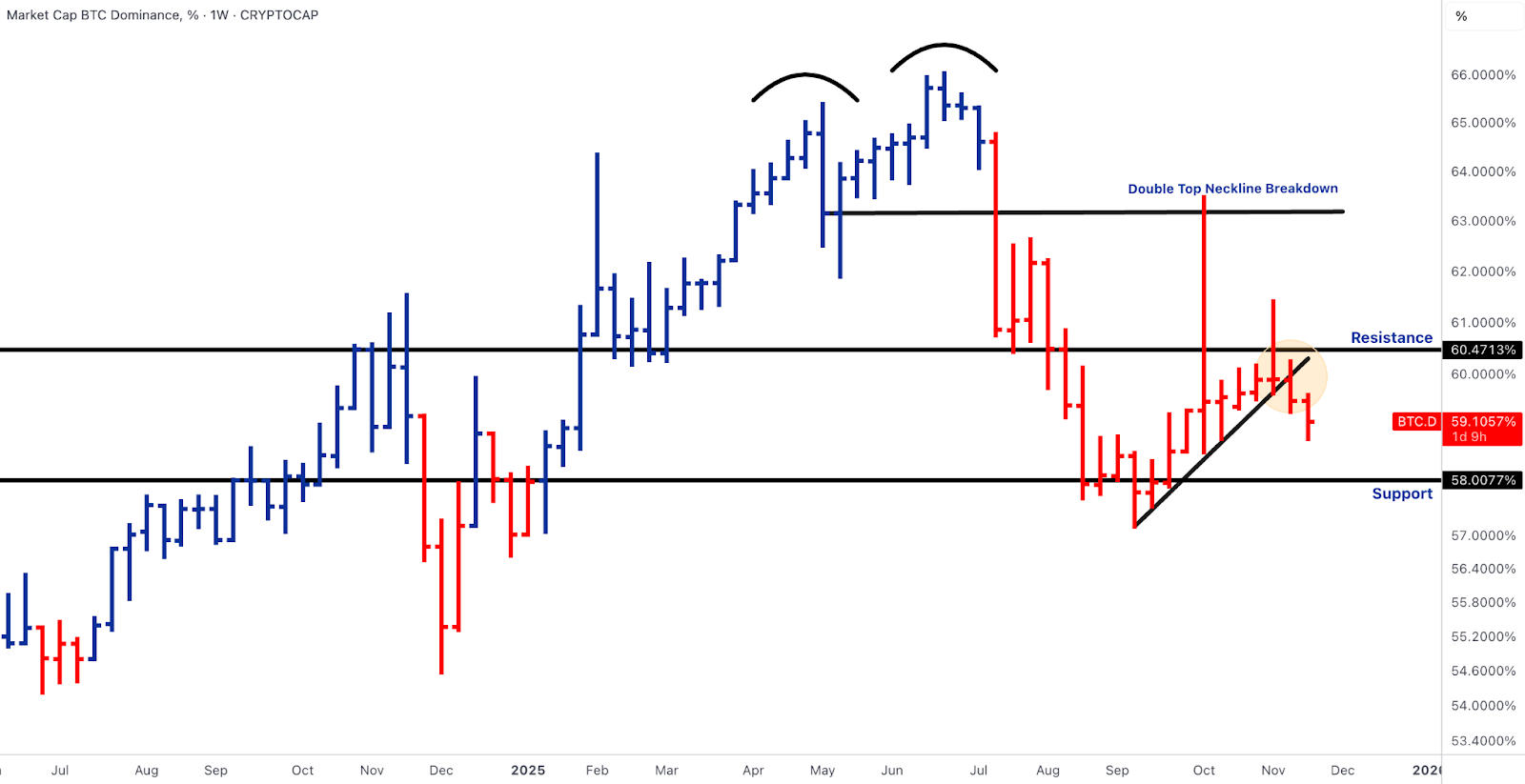

- BTC briefly fell to ~$80k before recovering above ~$83k. ETH underperformed in both USD and BTC terms. TOTAL3 retested $0.7T, now acting as the market’s stress band. BTC dominance slipped below 60%, showing limited core leadership.

- Flows: US BTC ETFs saw heavy outflows, one of the worst since August; ETH ETFs also declined. SOL ETF flows moved from strong debut inflows to neutral. Retail and leveraged positions exited first, while long-only investors and corporate treasuries added selectively.

- Institutional & policy moves: OCC confirmed banks can custody crypto and pay gas fees. Japan advanced tax relief for corporate crypto. Brazil clarified regulations. ETP providers launched new leveraged and sector ETFs. Corporates (miners, treasuries) remained opportunistic, rotating ETH into staking and basis-yield strategies.

- Takeaway: Price action reflects a controlled deleveraging phase. Strong infrastructure, policy clarity, and balance-sheet activity suggest this is position management, not abandonment. Key questions for December: will ETF outflows stabilise, and can BTC hold the $80–85k stress floor without forced liquidations?

Our Take:

Markets are in a controlled shake-out. Retail and leveraged positions are exiting, but institutional players are selectively adding. Price dips reflect short-term technical stress rather than fundamental abandonment.

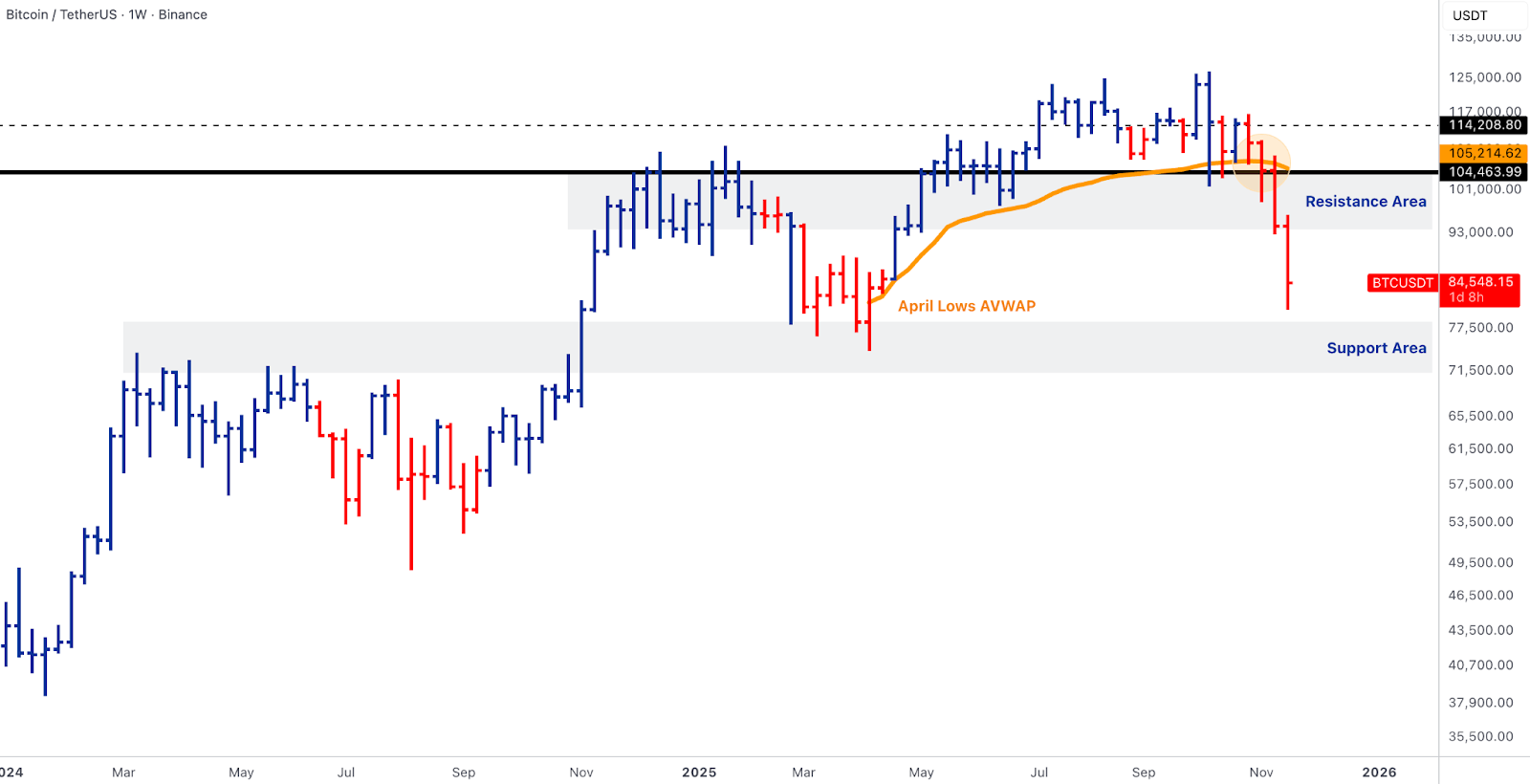

BTC — Below AVWAP, Above the Abyss

- BTC shifted from consolidation to corrective mode, failing to reclaim the $100–104k range and dipping into the mid-$80ks before stabilising. Closed mid-$80ks to low-$90ks, below April-lows AVWAP (~$106k). Resistance now $100–106k, secondary at $114–115k, prior extension $126–128k.

- IBIT ETF sits in a high-volume support band. Heavy outflows did not trigger disorderly selling as authorised participants matched redemptions with secondary-market demand.

- US BTC ETFs recorded another large net outflow week, including two days exceeding $300M. Weakness linked to retail and ETF de-risking, not hedge-fund shorting.

- Medium-term sponsorship bids remain: Tether moved $100M BTC to reserves, Kazakhstan plans $1B crypto fund, MicroStrategy holding.

- Tactical map: support $80–85k (stress floor), failure opens $70s. Resistance $93–104k primary, $114–115k secondary. BTC is in a rebuild phase, not a chase phase.

Our Take:

BTC remains in a rebuild phase. The latest wave of ETF redemptions forced price into the $80-85k stress band, where responsive bids have begun to appear, but this support should be treated as tactical rather than structural. A sustained reclaim of the April-lows AVWAP cluster around $100-106k would be the first sign that confidence is returning to the benchmark, yet until flows stabilise, rallies into that zone are likely to meet supply from de-risking ETF holders and systematic sellers.

ETH — Collateral Damage, But Rails Strengthen

- ETH lagged BTC again. Broke $3,200 (April-low AVWAP), dropping toward $2,500–2,600 support. Weekly candle shows lower high and lower low; $3,800–4,000 range confirmed as lost.

- ETH/BTC ratio fell below 0.034, hovering 0.032–0.033. Market favours BTC over ETH when volatility spikes.

- Flows: ETH spot ETFs recorded continued outflows, smaller than BTC. Treasury vehicles trimmed ETH for buybacks/diversification; structured products saw NAV compression.

- Staking/credit dynamics remain strong: over 1.5M ETH queued for staking. BlackRock filing for staked ETH ETF. Coinbase lending extended. Aave Labs launched a high-yield savings product. Large treasuries maintained or increased holdings while managing drawdown with derivatives.

- Tactical map: defend $2,500–2,600 spot and 0.032–0.033 ratio. ETF flows need to stabilise. Reclaim ~$3,200 and 0.035–0.037 ratio signals potential ETH leadership recovery, especially into 2026 with Fusaka upgrade and L2 consolidation.

- Ethereum Foundation continues interoperability and privacy work via Kohaku framework.

Our Take:

ETH remains structurally sound but tactically pressured. Outflows and ratio weakness weigh on short-term performance, while staking, credit, and institutional interest continue to strengthen the medium-term outlook.

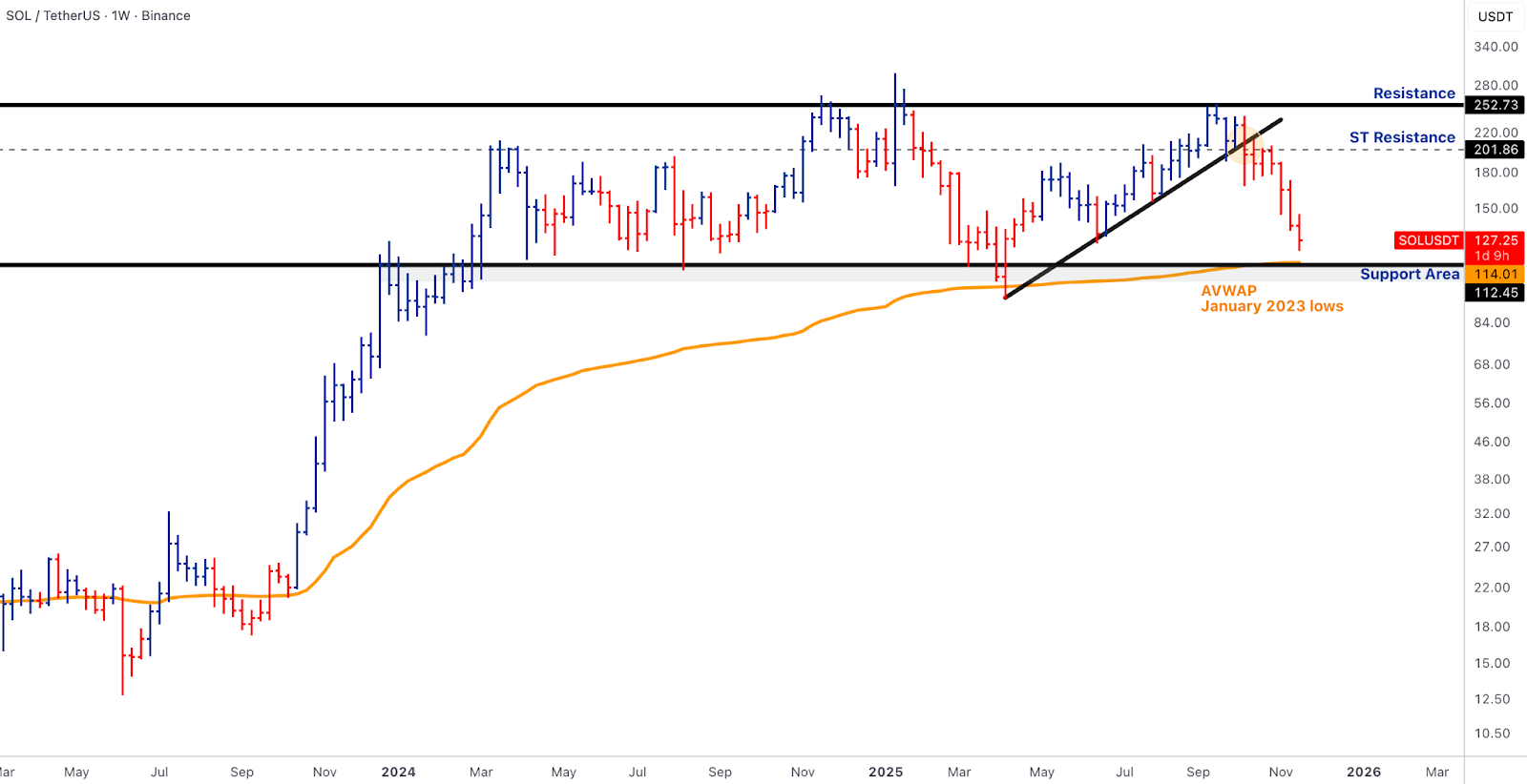

SOL & BNB — Divergent Themes

SOL

- SOL ETF inflows remain strong at ~$130M, the only major line with consistent positive demand in a weak tape.

- ETF wrapper set continues to expand: 21Shares joins Fidelity and VanEck. Institutional SOL staking strategies are gaining traction.

- Spot price remains corrective, trading in the low $120s, approaching $115 AVWAP from January 2023.

- On-chain activity cooling, including active addresses, highlights the need for re-acceleration before ETF flows can drive outright leadership.

BNB

- Binance treasury continues accumulation, adding $13M+ in BNB despite market sell-off.

- OCC guidance supports banks holding crypto for operational purposes. Kraken IPO and regulatory clarity strengthen institutional infrastructure.

- Price retraced from $1,000 but remains above $742 breakout. Behaves more like a cash-flowing exchange equity than a speculative L1 token amid deleveraging.

Our Take

SOL ETF demand remains solid, but momentum and on-chain activity lag. BNB demonstrates treasury-led resilience and acts as a structural, institutional-focused asset rather than a pure speculative play.

Emerging Rotation — Defensive Alpha

- The market favoured defensive rotation over fresh speculative risk.

- PI Network (PI) outperformed, driven by community narratives, mainnet migration, and alignment with European standards (MiCA, ISO-20022). Serves as a gauge for how far retail will reach in a drawdown.

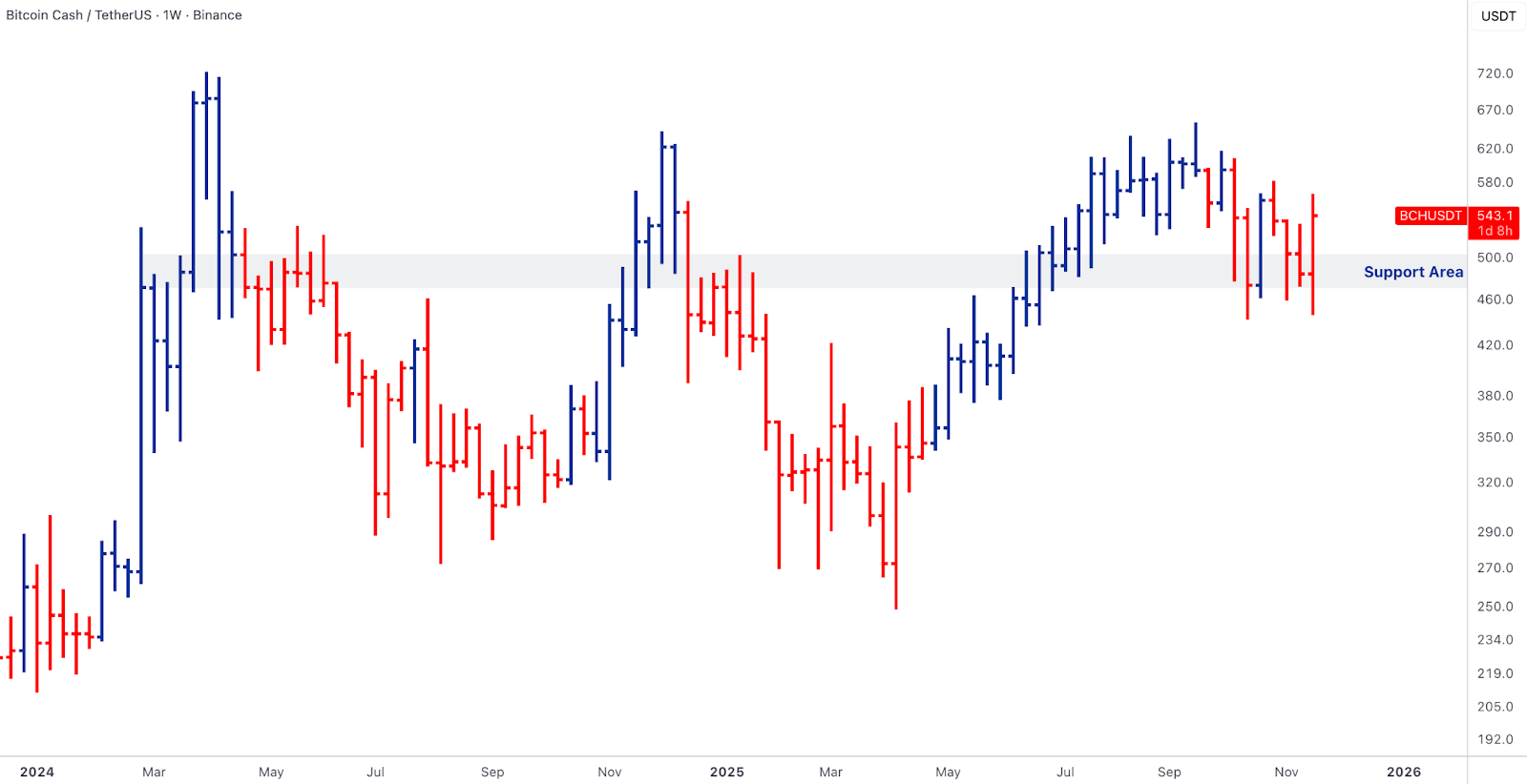

- BCH performed steadily as a “cheap Bitcoin” proxy with minimal ETF overhang. Coverage around halving and low-fee payments reinforced the narrative; on-chain metrics are stable.

- UNUS SED LEO benefited from buyback-and-burn mechanisms and exchange-linked cash flows, insulating it from broader market drawdown.

- ASTER and WLFI showed idiosyncratic strength: ASTER through developer activity and EVM-RWA infrastructure niche; WLFI via political/speculative narratives and media attention.

- None of these indicate a new structural leadership, but show capital targeting carry, treasury support, and narrative optionality in assets less exposed to ETF redemptions.

Our Take

Investors are rotating into assets with cash-flow, scarcity, or structural support. This is tactical positioning in a deleveraging environment, not the start of a new risk cycle.

Rails, Policy & Tokenisation

- Price stress contrasts with ongoing infrastructure and policy improvements.

- US: OCC guidance allows banks to hold crypto for operational purposes.

- Hong Kong: tokenisation pilot launched for real-value assets.

- Institutions: JPMorgan, DBS expanding tokenised deposits and on-chain settlement.

- Investor products:

- Grayscale approved for DOGE/XRP ETFs.

- 21Shares launched leveraged DOGE/index ETFs.

- Coinbase derivatives expanding altcoin futures coverage.

- Legislation: Japan advancing tax relief for token issuers; US proposals floated for paying taxes in BTC.

Our Take

Institutional rails and regulatory frameworks continue to strengthen. Volatility is near-term, while the market’s backbone is steadily solidifying.

Outlook — Ownership Upgrade

- ETF redemptions are clearing retail and systematic exposure.

- Endowments, corporate treasuries, and miners are maintaining or adding exposure.

- SOL continues to attract net ETF inflows despite the corrective spot price.

- Macro: 10-year Treasury low-4s, Fed communication “higher for longer,” credit delinquencies rising gradually.

- Desk stance: patience, not aggression.

- Opportunity: higher-quality BTC and ETH ownership on strong balance sheets, paired with hardened rails, may drive a narrower but more durable recovery than prior indiscriminate beta rallies.

Our Take

The current phase is a controlled shake-out. Smart positioning now sets the stage for a higher-quality, more resilient market recovery.

Thanks for reading this week's Market Pulse.

We’re watching flows in real time. If you want early alerts, customised sizing analysis, or routing paths for your trade, we’re here to help you execute on your strategy.

Get in touch with your Relationship Manager.

- The Hex Trust Markets Team