Rails Over Risk: Institutional Infrastructure Advances as Macro Volatility Tests Conviction

Blueprint - Regime, Flows & Macro Context

TL;DR / Key Points

- Market remains in a late-cycle but still constructive risk regime, characterised by selective risk-taking rather than broad beta expansion.

- BTC dominance continues to resolve lower following a confirmed weekly double-top breakdown, signalling rotation pressure rather than outright risk-off.

- TOTAL3 failed to reclaim prior ATH weekly closes and is consolidating below resistance, but structural higher lows remain intact.

- Spot ETF flows were mixed but stabilising, with BTC flows oscillating around neutral and ETH flows showing early signs of bottoming.

- BTC Spot ETFs: +286.6M USD net for the week, with strong creation days mid-week offsetting modest redemptions.

- ETH Spot ETFs: +209.1M USD net for the week, driven by front-loaded inflows early in the week before some late-week consolidation.

- SOL Spot/ETP Products: +36.2M USD net for the week, with consistently positive daily flows supporting a steady participation backdrop.

- Macro catalysts:

- JOLTS confirmed continued cooling in US labour demand without a disorderly collapse.

- FOMC meeting delivered no policy shock; messaging reinforced a data-dependent but patient stance.

- Macro takeaway: No hawkish re-acceleration, no recessionary shock - a “grind with dispersion” regime.

- Next week’s macro:

- CPI and PPI prints

- US NFPs, retail sales, Flash PMIs

- Treasury refunding/rate supply dynamics

- Ongoing QT runoff pace commentary

Our take: Last week reinforced a regime that is neither outright bullish nor distributional. The combination of a cooling but resilient labour market and a Fed that is clearly past peak hawkishness keeps financial conditions permissive enough for rotation and selective alpha, but insufficient to drive indiscriminate risk-on behaviour. The structural signal comes not from macro beta, but from relative performance and product-driven flows, a setup where BTC consolidates, ETH stabilises, and capital expresses itself through specific narratives rather than the index. This is precisely the environment where disciplined allocation into validated themes outperforms momentum chasing.

Bitcoin (BTC) - Structure Over Momentum

- BTC failed to reclaim the $104-105k resistance zone, rolling over below April AVWAP.

- Price is consolidating above the $75-80k structural support band, avoiding trend damage.

- BTC dominance remains capped below former highs, reinforcing the absence of renewed BTC-led leadership.

- Spot BTC ETFs saw choppy but non-capitulatory flows, with IBIT holding above inception AVWAP.

- No miner capitulation or treasury-driven supply stress is evident.

Our take: Bitcoin is behaving as a macro anchor, not a leadership asset. The inability to reclaim resistance keeps upside capped near-term, but the equally important absence of breakdown signals suggests this is absorption, not distribution. In a regime where dominance is slipping, and ETH/BTC has already broken higher structurally, BTC’s role is to provide balance-sheet stability, not directional impulse. This favours relative-value positioning rather than outright directional BTC exposure until a decisive reclaim occurs.

Ethereum (ETH) - Long-term Relative Strength Keeps Building

- ETH is holding just below the April lows AVWAP, a key structural inflexion.

- ETH/BTC completed a confirmed breakout from long-term base support (~0.025), now consolidating above ~0.034 and testing short-term resistance at ~0.035. ETH may have completed its 15-week retracement following its longer-term breakout.

- ETH remains below the 2021 ATH weekly close (~4,600), defining the next macro validation level.

- ETH ETFs showed improving flow consistency, albeit still modest in magnitude.

- No negative protocol-level or regulatory catalysts this week.

Our take: Ethereum continues to quietly reassert itself as the primary relative-strength expression within large-cap crypto. The ETH/BTC breakout is not a momentum signal; it is a regime signal, indicating capital's willingness to move down the risk curve within crypto. As long as ETH holds above AVWAP support and ETH/BTC does not lose its breakout band, the balance of risk favours continued relative outperformance even if absolute price progress remains uneven.

Solana & BNB - Leadership Tests

Solana (SOL)

- SOL rejected at the $200-205 resistance zone, rolling over into support.

- Price is holding above January 2023 AVWAP, preserving long-term structure.

- No negative ecosystem headlines; weakness is technical and flow-driven.

- SOL remains a barometer for speculative appetite.

Our take: Solana’s pullback reflects exhaustion at resistance, not a failed thesis. In the current regime, SOL behaves as a volatility amplifier, outperforming in expansion phases and retracing sharply during consolidation. As long as structural support holds, SOL remains a valid leadership candidate once broader risk appetite re-engages.

Binance Coin (BNB)

- BNB failed to hold above the $1,000 psychological level.

- Structural breakout above ~$740 remains intact.

- No new regulatory or exchange-specific shocks this week.

Our take: BNB continues to act as a cash-flow proxy rather than a speculative asset. The pullback from $1,000 reflects valuation digestion rather than structural weakness. Provided the breakout zone holds, BNB remains a lower-beta large-cap stabiliser in portfolios.

Emerging Alpha Cluster

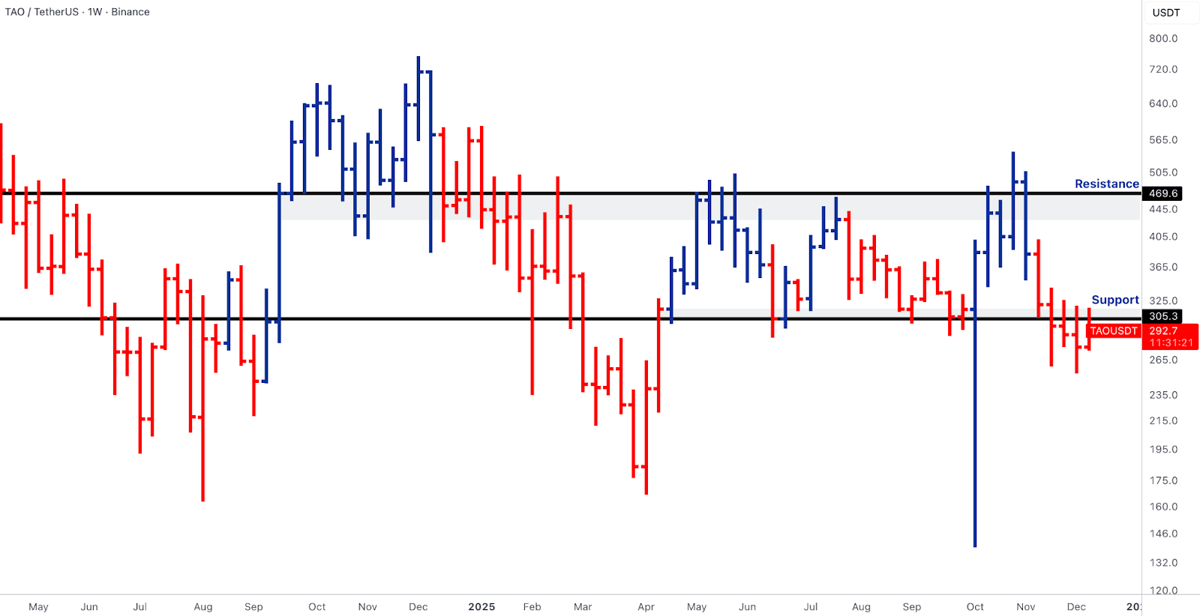

TAO (Bittensor)

- Grayscale’s Bittensor Trust continued trading on public markets, days ahead of TAO’s halving.

- The trust formalises institutional access to the AI-compute narrative, a non-trivial structural catalyst.

- Price remains range-bound but technically constructive relative to broader alt weakness.

Our take: TAO’s inclusion is catalyst-driven, not momentum-driven. Grayscale’s product validates institutional demand for decentralised AI exposure and places TAO firmly in the “thematic infrastructure” bucket rather than speculative beta.

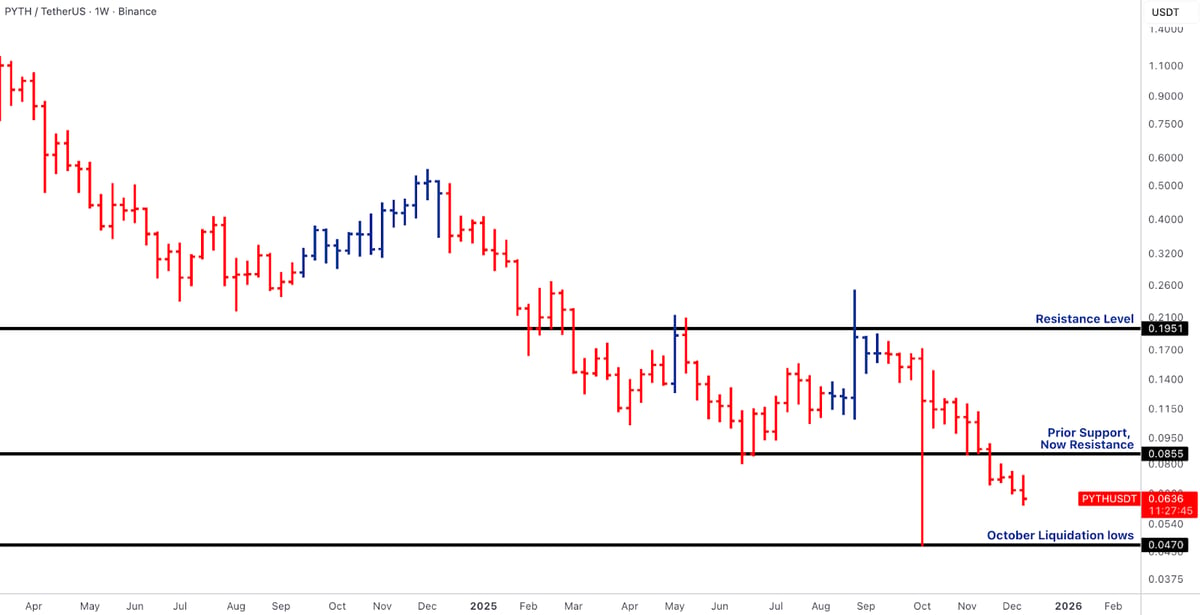

PYTH

- PYTH DAO announced a structured token buyback program funded by treasury revenues.

- The move reframes PYTH from pure oracle growth to capital-returning protocol economics.

- Price remains weak, reflecting macro conditions rather than catalyst invalidation.

Our take: PYTH is transitioning into a cash-flow-aware oracle, which matters long-term. The market is not pricing this yet, but buybacks introduce an institutional-grade capital allocation signal rarely seen in infra tokens.

LINK

- Coinbase and Chainlink announced an exclusive CCIP partnership for wrapped assets.

- This positions CCIP as a dominant interoperability layer for tokenised asset flows.

- Price underperformed short-term, but fundamentals strengthened materially.

Our take: This was a market-structure event, not a price event. CCIP exclusivity reinforces Chainlink’s role as middleware for the tokenised asset internet, a strategic asset, not a trade.

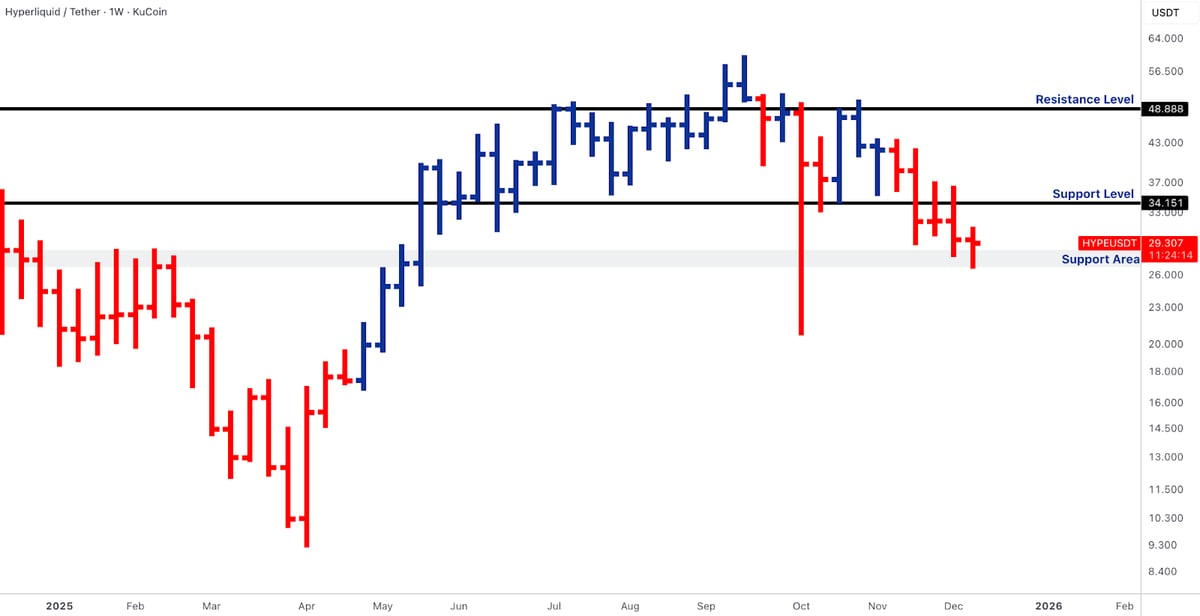

HYPE (Hyperliquid)

- Protocol-level treasury actions and buyback discussions highlighted sustainable revenue generation.

- Derivatives volumes remain structurally strong despite broader risk aversion.

- Price consolidated after earlier strength.

Our take: Hyperliquid continues to behave like an exchange-native equity, with treasury strategy becoming increasingly relevant. This is a rare case of on-chain derivatives translating directly into protocol value capture.

Rails & Productisation - Stablecoins, Tokenised Securities, and Regulated Distribution

- US market structure pressure is shifting from “should tokenisation exist” to “who writes the rulebook.” DeFi industry groups pushed back against proposals framed as tokenisation “guardrails,” highlighting the split between broker-dealer incumbents and on-chain market structure advocates.

- Tokenised securities rails advanced on two fronts:

- DTCC signalled progression toward tokenisation services for US securities infrastructure.

- JPMorgan executed a landmark on-chain financing using a Solana-based permissioned settlement token (USCP) tied to a real-world debt offering.

- Stablecoin regulation and bank-adjacent issuance accelerated:

- Ripple, BitGo, and Paxos received conditional approval for US banking charters.

- Moody’s proposed a stablecoin ratings framework focused on reserve quality.

- UK FCA reiterated a 2026 stablecoin framework timeline.

- Distribution platforms are building stablecoin-native channels:

- Stripe acquired the Valora wallet team to expand stablecoin services.

- Circle expanded regulatory footprint (including ADGM licensing) and distribution partnerships.

- YouTube / PYUSD headlines reinforced embedded stablecoin distribution as an emerging theme.

- Tether remained strategically central, with tokenisation ambitions and regional corridor expansion (including ADGM signalling).

Interoperability consolidation continued:- Coinbase + Chainlink CCIP exclusivity around wrapped assets.

- Hex Trust launched custody-wrapped XRP with DeFi utility across multiple blockchains, extending regulated custody into composable on-chain use cases and reinforcing institutional-grade rails between TradFi, custody, and DeFi.

Our take: This was unequivocally a rails week. From DTCC to JPMorgan to Stripe, Circle, Tether, and Hex Trust, the market keeps moving from experimentation to institutional implementation. The strategic signal is that regulated issuance, settlement, custody, and interoperability are converging into a coherent stack. This is how durable crypto adoption happens, not through speculative cycles, but through infrastructure that institutions can repeatedly use.

Outlook

- The upcoming week shifts focus to forward-looking macro releases, not the already-passed JOLTS/FOMC.

- Key releases include inflation and activity data that will shape real-rate expectations.

- Markets remain sensitive to liquidity rhetoric rather than absolute data levels.

Our take: With last week’s macro catalysts behind us, attention turns to whether incoming data validates continued disinflation without a growth shock. If so, the divergence between strong rail fundamentals and muted price action may begin to close. Until then, selectivity remains paramount.