Stress Regime into FOMC: Liquidity Fragility Meets Structural Progress

TL;DR / Key Points

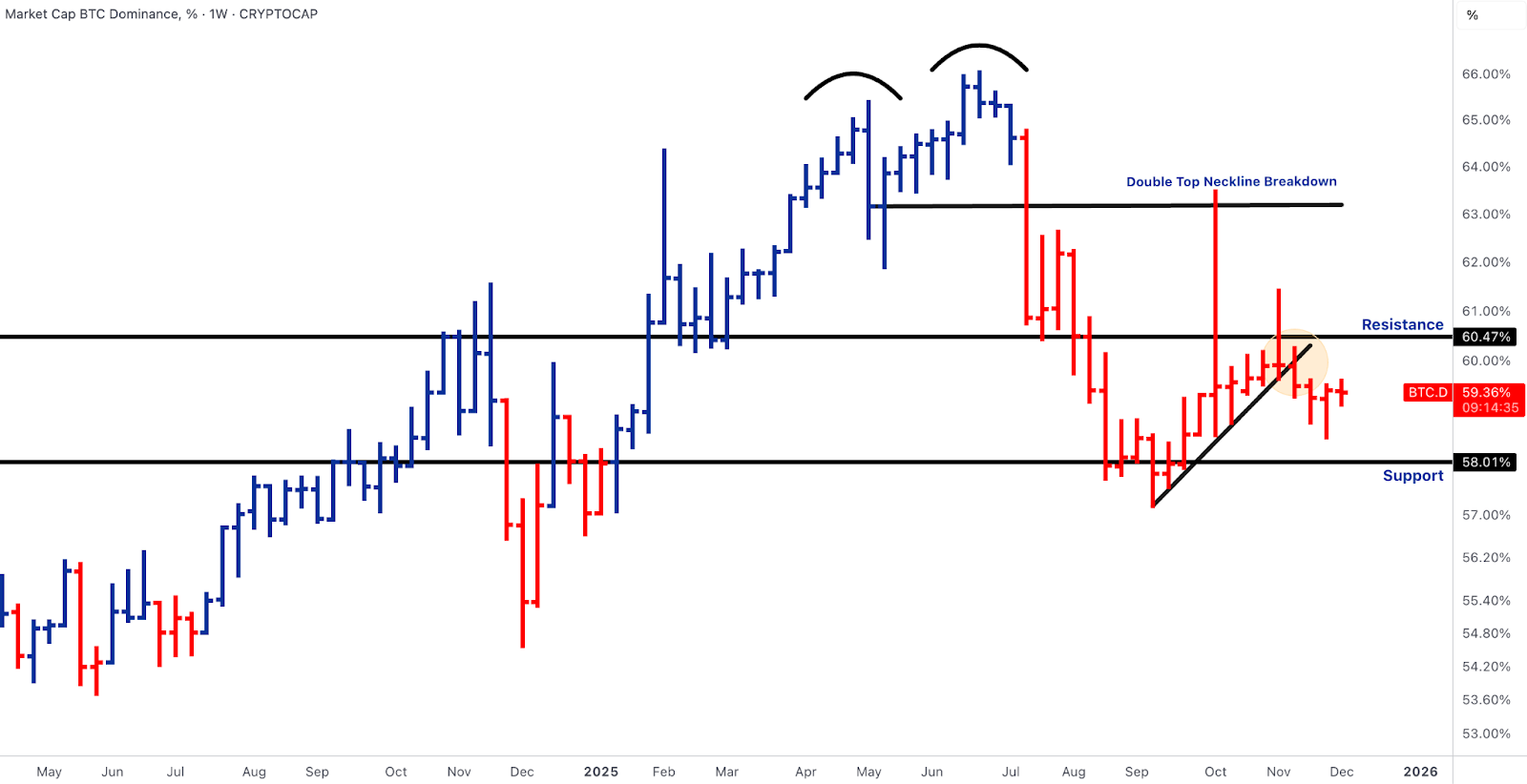

- Liquidity thinned into JOLTS/FOMC window, with BTC/ES turning lower, BTC dominance stuck under 60–61%, and TOTAL3 drifting toward the ~776B support.

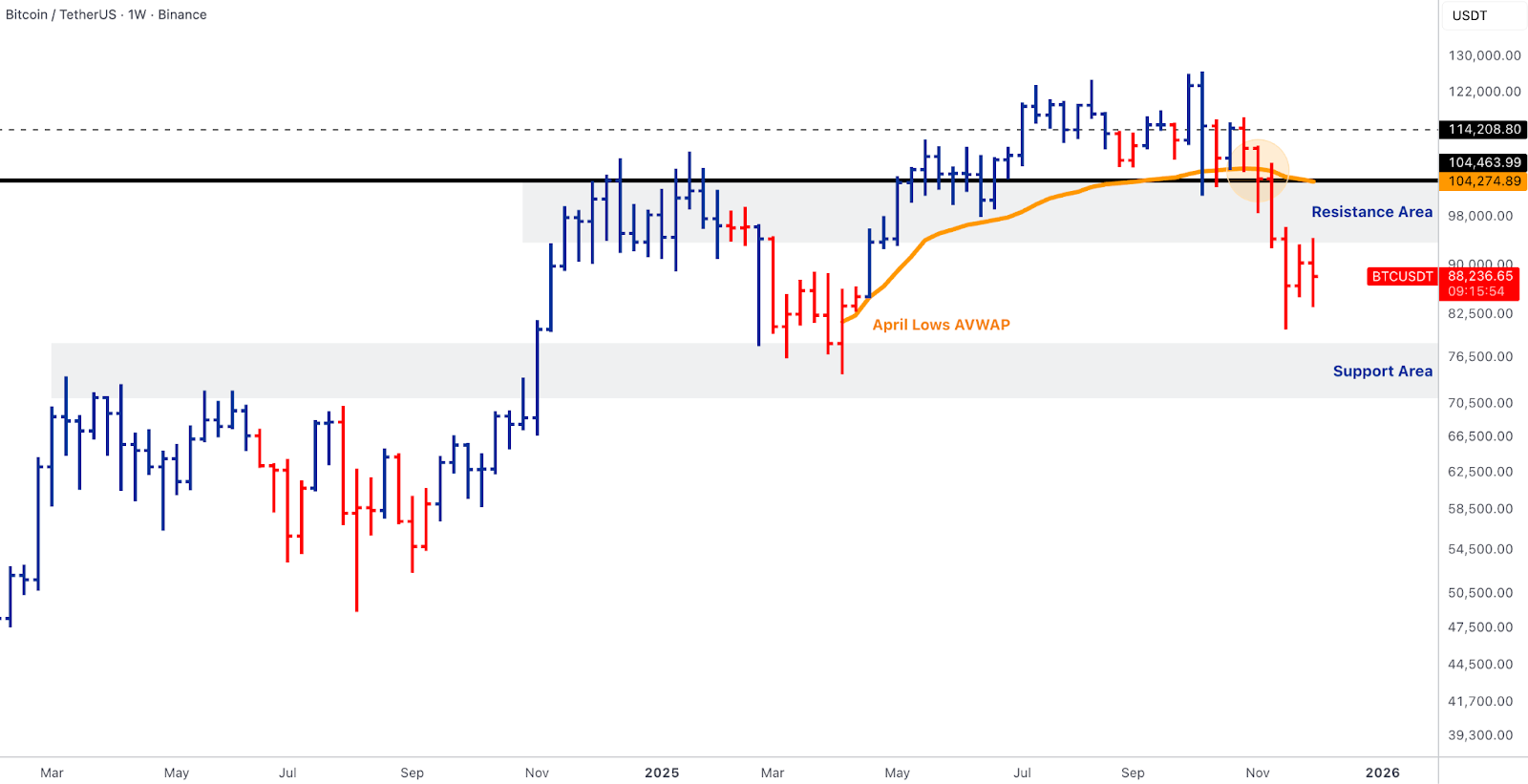

- BTC failed to reclaim 104–106k, leaving 88–90k exposed and 70–75k still untested. Spot ETFs saw another negative week at roughly –162M in outflows.

- ETH held a weak range as the ETHE redemptions outweighed inflows into BlackRock and Fidelity. Bias remains toward the 2,500–2,700 zone.

- Solana maintained positive ETF inflows whilst spot continued to drift toward the 114–115 AVWAP support cluster.

- Rotation remained catalyst-only: BCH, LINK (GLNK Launch), and AAVE outperformed on isolated drivers.

- Rails/tokenisation advanced with MoneyGram stablecoin settlement, Kraken’s integration with Backed Finance/Deutsche Börse, and WisdomTree’s first stETH ETP.

- Macro remained the dominant driver. Markets are unusually fragile, ahead of JOLTS and FOMC communication.

Our take: Market conditions remain tactically weak, but the structural picture continues to strengthen. Price action reflects thin liquidity and persistent ETF outflows, yet institutional rails, tokenisation pipelines and targeted flows into selective assets show the deeper architecture still improving. For direction to turn, the market needs a cleaner macro backdrop and an inflection in ETF flows. Until then, BTC and ETH trade defensively, while only catalyst-supported names show meaningful relative strength.

Market Overview

Crypto starts the week in a fragile liquidity environment, with markets highly sensitive to the upcoming JOLTS report and FOMC meeting. The BTC/ES ratio continued to weaken, ETF flows in BTC and ETH remained insufficient to stabilise price action, and BTC.D stayed capped below the 60–61% band. TOTAL3 drifted toward the ~776B support zone, confirming narrow market breadth and catalyst-driven rotation.

In contrast, regulatory clarity advanced across the UK, Italy and South Korea, and institutional rails strengthened with MoneyGram expanding stablecoin settlement, Kraken enhancing its tokenisation stack, and WisdomTree launching the first ETH staking ETP using stETH.

These structural gains stand in sharp contrast to current liquidity stress, leaving the market dependent on macro tone heading into Powell’s Wednesday press conference.

BTC – Failed Reclaim Ahead of Macro Volatility

- BTC consolidated below the 104–106k reclaim band, with the April-lows AVWAP acting as a precise ceiling on each retest.

- Weekly candle closed below the reclaim band, leaving the 88–90k liquidity pocket open and the broader 70–75k shelf untested.

- BTC ETFs recorded –$162M net outflows, led by IBIT, ARKB, and FBTC; IBIT now trades at inception AVWAP, signalling institutions are back at cost basis and marginal demand remains absent.

- Miner profitability remains pressured, with elevated breakevens forcing disciplined treasury management.

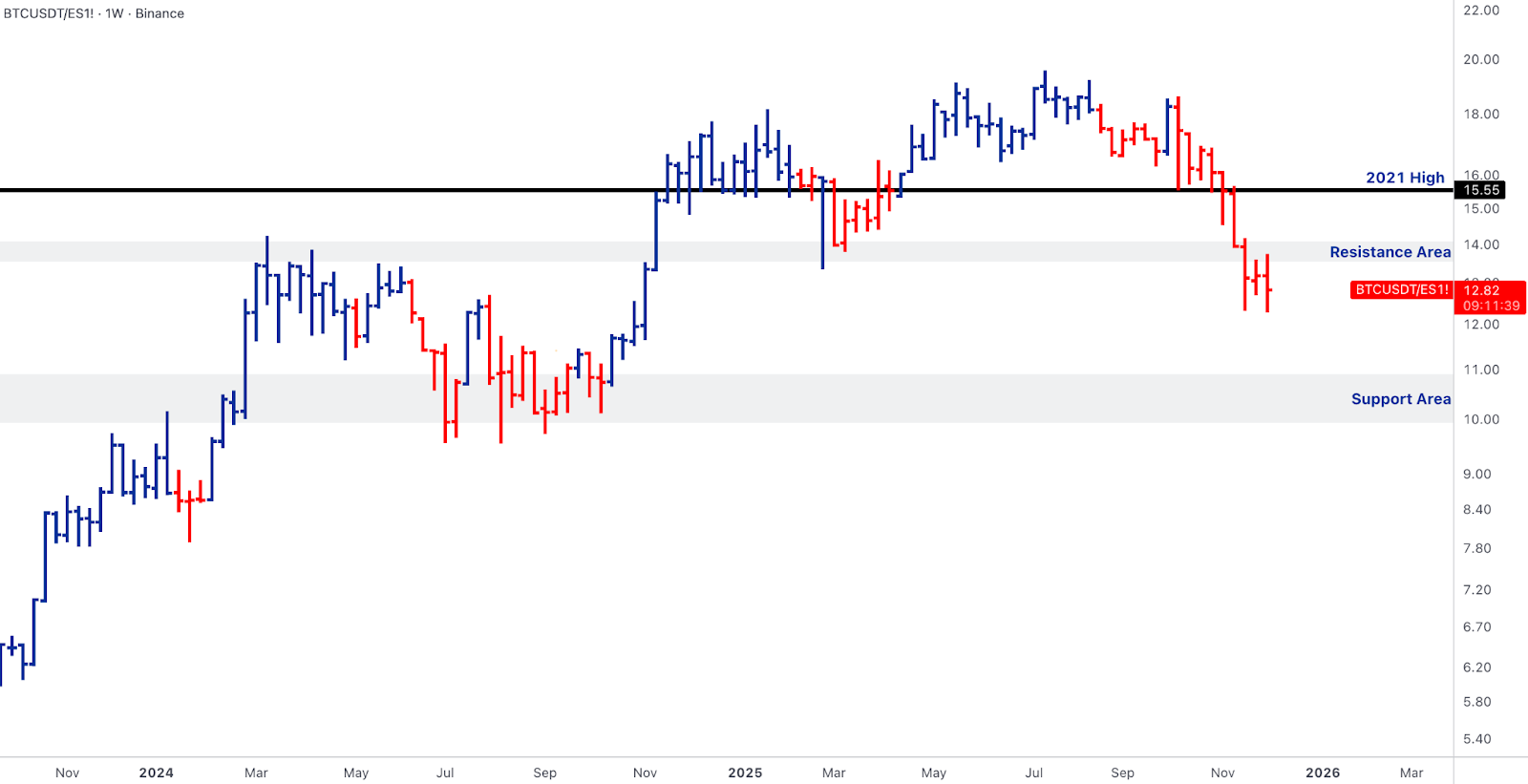

- Crypto is weakening relative to equities, while ETF flows failed to re-accelerate.

- Heading into the FOMC, BTC remains tactically fragile, requiring either a dovish macro tone or a clear inflow inflection to avoid deeper structural support tests.

Our take: BTC remains under structural pressure. Failed reclaim attempts, muted institutional demand, and miner supply pressure suggest the market could test 88–90k and potentially 70–75k without supportive macro signals or renewed inflows. Tactical caution is warranted ahead of the FOMC.

ETH – Fundamental Strength, Structural Repair

- ETH continued to lag BTC and macro beta, declining after failing at the April-lows AVWAP near 3,200 and losing the 3,850–4,000 structural defence earlier in the month.

- Price now leans toward the 2,500–2,700 demand cluster, with no clear leadership pivot observed.

- ETF flows were mixed: modest inflows from BlackRock and Fidelity were offset by continued ETHE outflows, leaving ETH without a sustainable inflow base.

- Fundamental developments remain strong:

- WisdomTree launched the first market stETH staking ETP using Lido.

- BitMine disclosed $150M ETH accumulation for its treasury strategy.

- Coinbase advanced Base bridging toward Solana.

- ETH remains the central settlement layer in tokenisation debates at the SEC and IMF.

- ETH/BTC ratio remains below 0.0342, far from the 0.0396–0.041 decision band that historically signals the start of ETH leadership cycles.

- ETH carries structural strength in narrative and rails, but price remains in repair mode until ETF flows stabilise and the ratio regains upward momentum.

Our take: ETH shows strong fundamental positioning, with staking, treasury accumulation, and layer-1 adoption reinforcing long-term value. However, price action remains weak, ETF inflows are insufficient, and the ETH/BTC ratio has yet to signal leadership. Structural repair continues, and ETH needs stabilised flows and ratio momentum to confirm a broader recovery.

Solana & Policy L1s – Positive ETF Demand, Price in Repair

- SOL remained the only major L1 with consistent positive ETF demand, registering $19.1M net inflows across BSOL, VSOL, and FSOL.

- Price did not follow flows: SOL extended its corrective downswing, losing the short-term rising trendline and failing below 201–210, leaving the 114–115 AVWAP confluence as the next meaningful support.

- L1 narrative benefited from policy-aligned catalysts:

- Franklin Templeton reiterated commitment to the Solana ETF.

- Solana Treasury’s Solmate equity rallied on the RockawayX merger announcement.

- Regulatory developments in Europe and the UK continued to favour institutional-grade infrastructure.

- Despite positive ETF flows, TOTAL3 remains under pressure and BTC liquidity is draining, leaving SOL in a leader-under-repair structure: supportive flows exist, but broader liquidity is insufficient to reprice high-beta L1s sustainably.

- BNB held above the 742 breakout zone after losing the 1,000 handle in November, but muted newsflow relative to SOL made its relevance secondary this week.

Our take: SOL shows strong institutional ETF support, but price remains in repair mode due to broader market liquidity constraints. Positive policy and corporate catalysts reinforce the narrative, yet high-beta L1s need wider market engagement to recover meaningfully. BNB remains less relevant this week, reflecting muted momentum and newsflow.

Emerging Rotation Leaders – Catalyst-Driven Outperformance

- With TOTAL3 failing its trendline and BTC.D stuck in containment, this week’s outperformance was concentrated in catalyst-driven names.

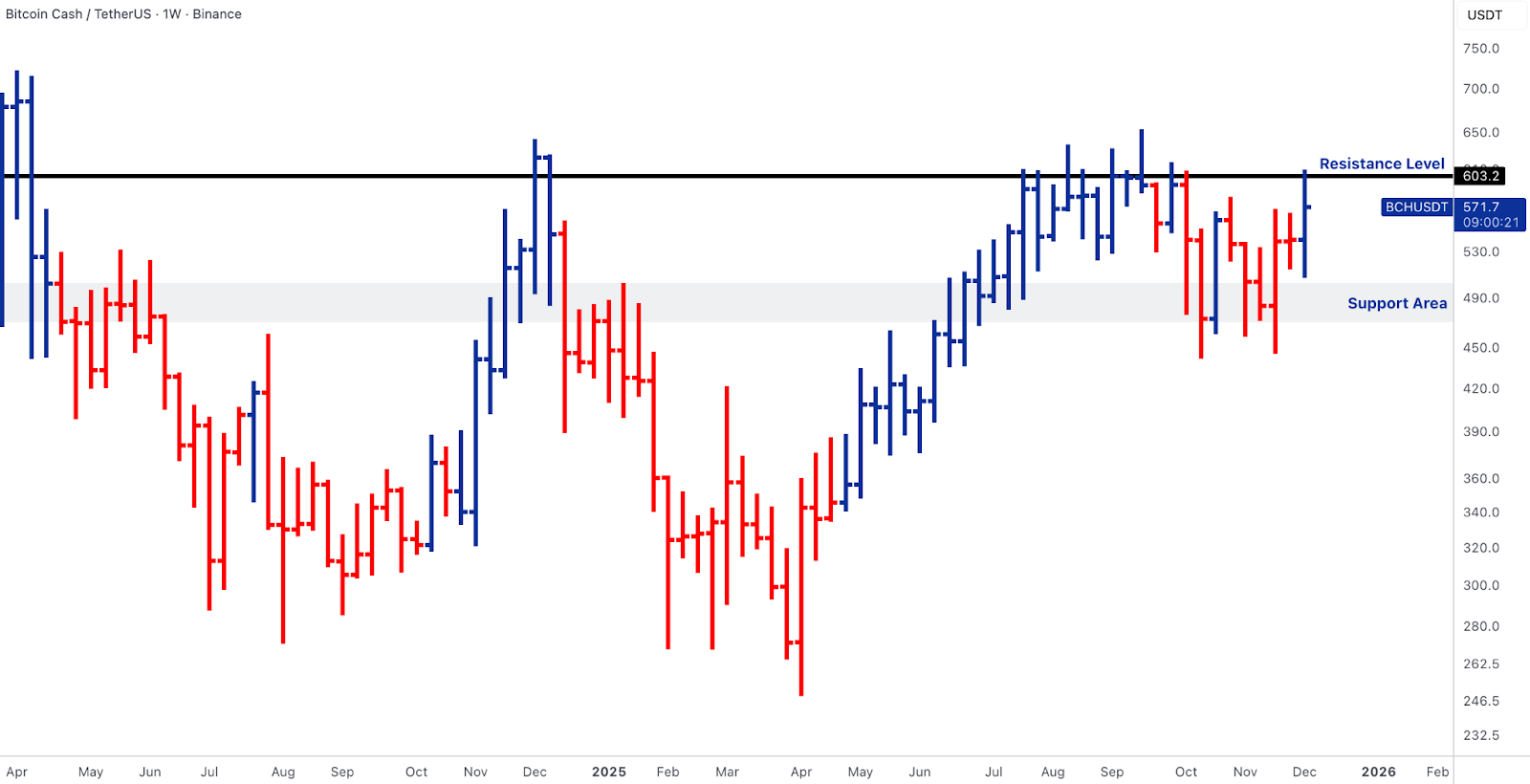

- Bitcoin Cash (BCH) continued its hard-money rotation, grinding toward the ~603 resistance zone as investors sought simpler monetary narratives during BTC stagnation.

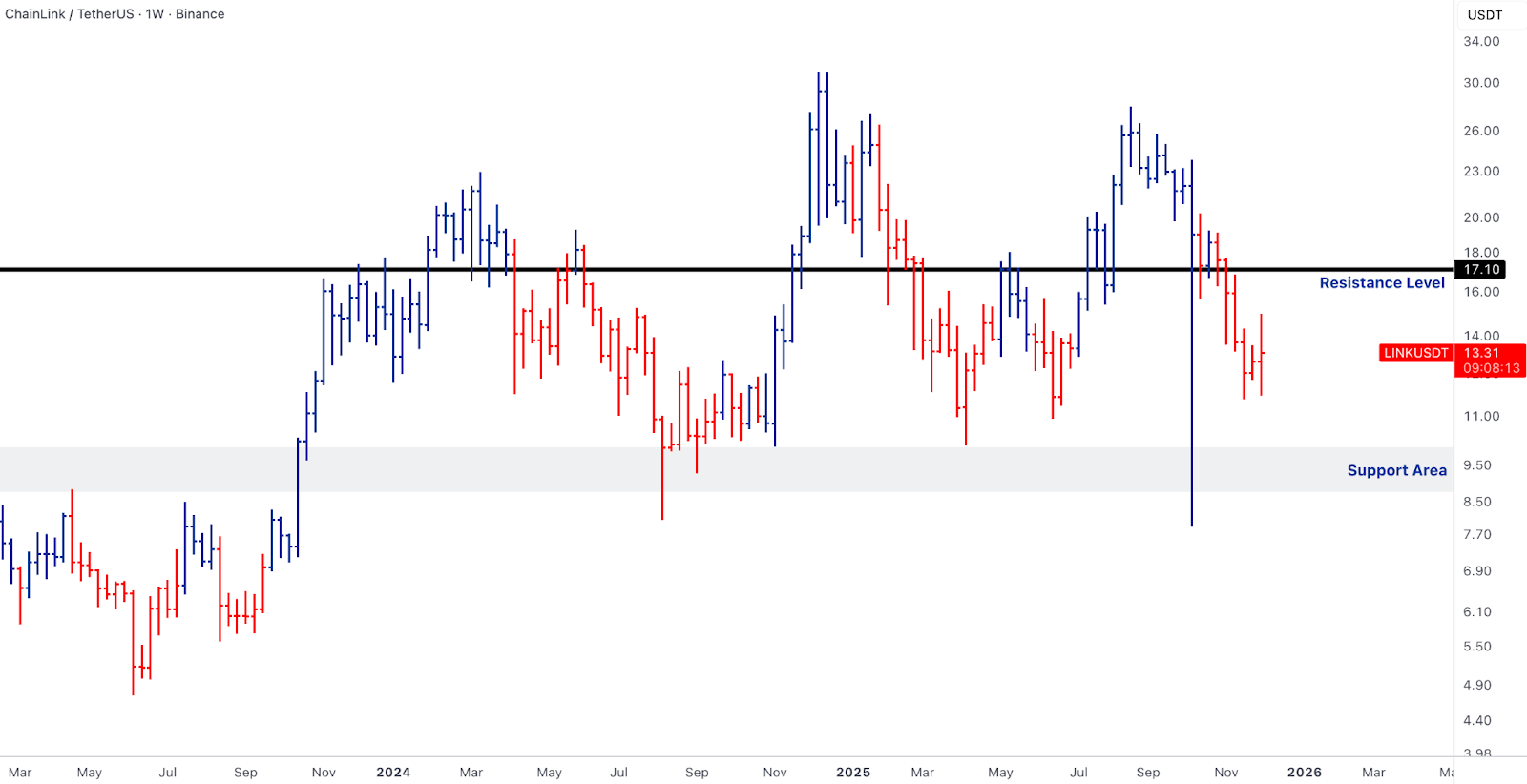

- Chainlink (LINK) benefited from the launch of Grayscale’s GLNK ETF, introducing oracle infrastructure into regulated product wrappers for the first time; LINK remained capped below 17.1, but the structural story around data-layer settlement strengthened materially.

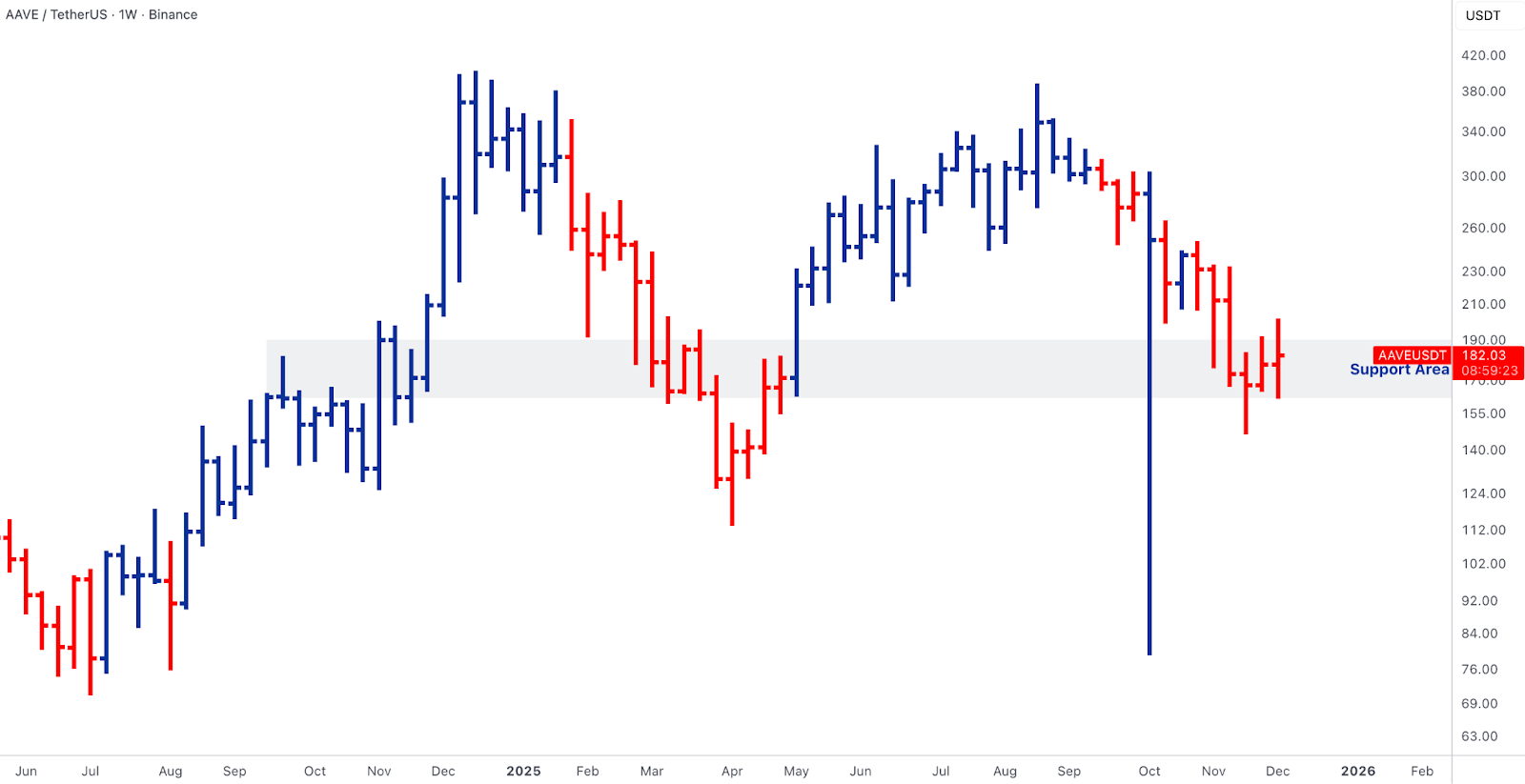

- Aave (AAVE) found support in the 170–180 region as Lighter, the perps DEX, rolled out spot trading, signalling a broader uptick in decentralized liquidity venue development.

- Overall, these outperformers reflect the market’s prevailing condition: tactical rotation into catalysts rather than broad structural breadth expansion.

Our take: Tactical rotation continues to dominate, with catalyst-specific names outperforming amid BTC stagnation and contained market breadth. BCH, LINK, and AAVE highlight that narrative and product-driven catalysts are driving short-term positioning, while broader market leadership remains under repair.

Rails & Tokenisation – Structural Progress Despite Cyclical Stress

- MoneyGram deployed stablecoin settlement via Fireblocks, signalling that remittances are shifting on-chain at scale.

- Kraken expanded its tokenisation stack through the acquisition of Backed Finance and announced a partnership with Deutsche Börse, bridging digital and traditional markets within a regulated framework.

- At the policy level, a US SEC panel debated the architecture of tokenised markets, while BlackRock executives reiterated that tokenisation is the future of settlement infrastructure across credit, money markets, and real-world assets.

- Ethereum continued to dominate rails developments via:

- WisdomTree’s stETH ETP

- Ongoing treasury demand

- Base-Solana bridging

- TON advanced ecosystem monetisation via a ~$420M shelf registration filing for Telegram-native token issuance.

- These developments highlight that the structural bull market in rails is accelerating, even as spot prices remain in cyclical correction.

Our take: Structural progress in settlement rails and tokenisation remains robust. Major deployments, regulatory engagement, and ecosystem expansions signal accelerating adoption, reinforcing long-term growth in digital infrastructure despite short-term price weakness.

Outlook: Macro - Sensitive Stabilisation or Extension Risk

- Next week’s market pivots on JOLTS and the FOMC.

- Softer JOLTS would support gradual labour-market cooling, bullish for financial conditions, providing a tactical window for BTC and ETH to stabilise above immediate supports.

- Firmer JOLTS risks re-tightening liquidity expectations into Powell’s press conference, where a “higher-for-longer but flexible” narrative remains the base case.

- Crypto enters these events from a position of tactical vulnerability:

- BTC below 104–106k reclaim.

- ETH trades below all structural bands.

- SOL drifting toward major AVWAP support despite positive ETF demand.

- Market breadth remains constrained until TOTAL3 can reclaim 900B+, and leadership cannot shift until ETH/BTC approaches 0.0396–0.041.

- The burden of proof lies not in macro data alone, but in re-acceleration of ETF inflows and improved alt-market structure.

- Current regime is stress-plus-dispersion, where catalysts matter but liquidity dictates direction.

Our take: Crypto remains tactically fragile ahead of key macro prints. Stability depends on either softer labor data or renewed ETF inflows, while structural leadership and broader breadth remain impaired. Liquidity, not narratives alone, will dictate near-term market direction.

Thanks for reading this week's Market Pulse.

We’re watching flows in real time. If you want early alerts, customised sizing analysis, or routing paths for your trade, we’re here to help you execute on your strategy.

Get in touch with your Relationship Manager.

- The Hex Trust Markets Team