Aug 11, 2025

Back to Risk-ON after a textbook shock, stabilisation and rotation week.

Summary:

- A textbook shock, stabilisation and rotation week was seen last week. Last Monday’s ETF stress forced fast de‑risking; by mid‑week, flows normalised and breadth expanded, culminating with ETH reclaiming $4k and BTC dominance printing the lowest weekly level since mid-January.

- Alt leadership was structure-led, staking demand, yield tokenisation, and infra rails absorbed the shock better than short-cycle ETF money.

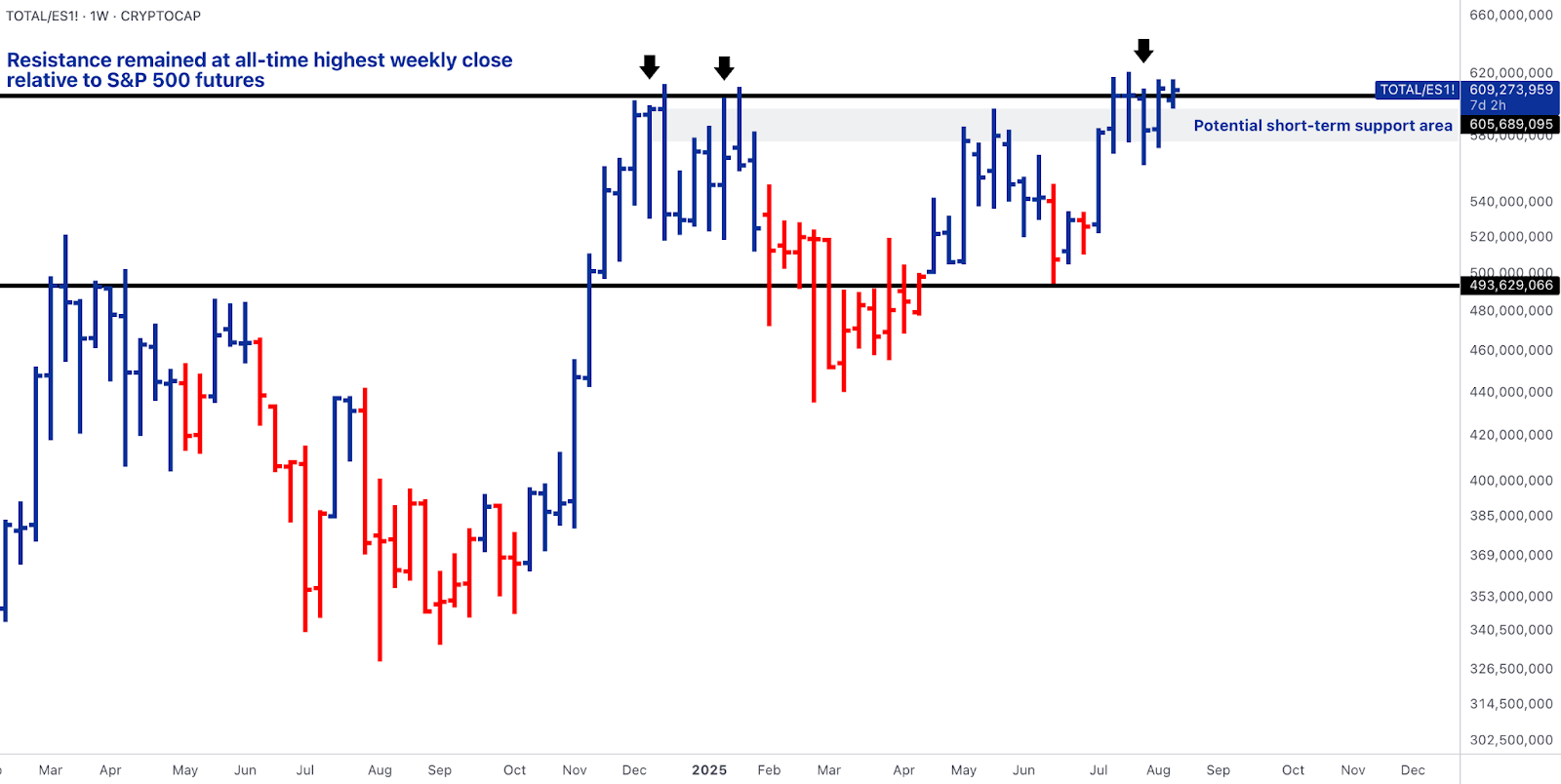

- The TOTAL vs S&P 500 futures relative stayed pinned near record levels, signalling macro risk budgets remain intact.

- Risk assets, including stocks and crypto, started the week on a positive note on Monday thanks to a renewed ‘Risk-On’ mode as solid corporate earnings underpinned high valuations in the tech sector.

- Macro-eventful week ahead: US-China tariff deadline expiring on Tuesday, US CPI data and Trump/Putin meeting.

Ethereum: Record ETF outflow led to orderly reset; $4k reclaim re‑asserts leadership

- ETH began the week last week with its largest single‑day U.S. spot ETF outflow on record (~465M net outflow), the exact kind of “one‑day event” that forces risk budgets to reset.

- Importantly, flows stabilised mid‑week (flattish to small net positives), and spot pushed through $4k into the weekend.

- On‑chain, the validator exit queue remains elevated (8–10 day waits), a residual from the stETH/Aave deleveraging wave, yet entry demand persisted, and exchange inventories continued to look thin.

- Vitalik backs the idea of Ether treasury companies but warns of overleverage, further backing signs that ETH turns into a hot corporate treasury trend on Wall Street.

- Derivatives confirmed the reset‑then‑re‑risk pattern: early‑week funding and short‑tenor basis compressed, then normalised as bids came back.

- Technically, ETH/BTC’s July breakout is now in a clean post‑breakout retest; that’s the rotation backbone as allocators are extending duration back into ETH while BTC bases.

Bitcoin goes from historic redemptions to range stability; BTC.D makes new weekly lows

- The ETF channel followed last Friday’s capitulation with net outflows again Monday and Tuesday (~520M), then flipped to inflows mid‑week, mapping almost one‑for‑one to price behaviour: flush to ~113k, base around ~114k, and higher into the weekend.

- The key structural tell wasn’t price, it was dominance: BTC.D posted its lowest weekly reading since mid-January, confirming breadth expansion rather than a risk‑off regime (chart 1).

- On the surface, futures showed the same pattern as ETH: front‑end basis compressed into Monday’s stress, then rebuilt as liquidity providers re‑opened risk; funding normalised from negative/flat back toward neutral.

- Options skew briefly leaned protective, then mean‑reverted with realised vol coming off intra‑week highs.

- The TOTAL/S&P 500 futures relative hovered near cycle‑highs (chart 2), macro risk appetite hasn’t cracked, so ETF redemptions look like timing/risk‑budget management, not thesis rejection.

- A new weekly low in BTC.D while price holds the 113–119k band is classic rotation confirmation: capital broadened out without undermining the BTC base. The reserve‑asset bid (treasuries/balance sheets) still defines the floor; breadth says alts can lead without undermining BTC’s base.

Solana sees leverage digestion; listed‑derivatives depth + venue liquidity (RAY) lead the tape

- SOL spent the week digesting a high‑teens drawdown while institutional participation held up.

- CME SOL activity stayed elevated (the July step‑change in volume/OI persisted), and on‑chain TVL and DEX/perp volumes remained firm, evidence that usage is cushioning price.

- Inside the ecosystem, Raydium (RAY) outperformed with a ~20% rise in liquidity‑program upgrades and new perp pairs, capturing flows even as SOL consolidated.

- That divergence, which showcases venue/infra tokens leading while the base L1 re‑bases, is classic re‑risk sequencing after a shock.

- The derivatives stack and venue liquidity argue for buy‑the‑dip frameworks as long as we hold a weekly close above ~$150 on SOL, with a break above 0.02 on a weekly close for RAY/SOL, opening the potential of further relative outperformance for the DEFI token.

Pendle: Yield tokenisation is where ETF money goes to work when the tape wobbles

- PENDLE was among the week’s top gainers. Mechanically, when ETF prints wobble, on-chain “durable yield” becomes the redeployment venue: longer-tenor PT/YT pools see tighter discounts, depth concentrates in majors (LSTs, ETH basis), and volumes pick up as ETH stabilises.

- This week followed that playbook: ETH above $4k, BTC in range, and ETF flows back to neutral, exactly when tokenised-yield venues pull capital.

- PENDLE is the fixed-income expression of the same rotation that lifted ETH, an income proxy that doesn’t require ETF sponsorship but does require calm volatility and credible ETH leadership.

Chainlink: product cadence is turning policy clarity into deployable rails

- LINK extended higher on the back of Data Streams for U.S. equities/ETFs, moving regulated market data on‑chain where RWAs, stablecoins, and structured products need it.

- Combine that with CCIP and Proof‑of‑Reserve, and you’ve got the data + messaging + attestation stack allocators can underwrite.

- Importantly, this week’s move didn’t require a broad risk melt‑up; LINK rallied in sync with alt breadth because desks paid for infrastructure that monetises the very flows (tokenised yield, audited stablecoins) that keep working in neutral ETF weeks.

- The market is paying for infrastructure that captures regulated, yield-bearing flows, with LINK being a clean expression of that structural demand, which persisted even through an ETF-shock week.

Outlook for the Week

- Risk assets, including stocks and crypto, started the week on a positive note on Monday thanks to a renewed ‘Risk-On’ mode as solid corporate earnings underpinned high valuations in the tech sector.

- Macro-eventful week ahead:

- The US-China tariff deadline expiring on Tuesday, markets are expecting an extension.

- US CPI data - Street expects a ready of 3% annual pace vs Fed’s target of 2%. An upside surprise might dampen the expectation of a September rate cut, markets have priced in 88% odds for the first rate cut next month.

- Trump/Putin meeting - Due to meet on Friday to discuss Ukraine.

Oops! Something went wrong while submitting the form.