ETF stabilisation meets a global divergence in policy while rails accelerate

TL;DR / Key Points

- BTC & ETH ETFs printed their first net-positive weekly flows since October,

- Prices stabilised: BTC held the low-90ks stress floor, ETH found support near ~2,600, and TOTAL3 defended its lower support band

- Institutional activity surged: CME crypto derivatives hit all-time-high daily volumes

- Treasury participation broadened: Texas added $5M of IBIT to reserves; corporates like Metaplanet, Xapo and Bitmine expanded BTC/ETH treasury exposure.

- Rails accelerated: Visa, US Bancorp and Klarna/ Stripe scaled stablecoin settlement; Tether’s USDT0 transfers surpassed $50B.

- Tokenisation advanced: Amundi tokenised a money-market fund on Ethereum; Securitize gained EU approval for a tokenised trading system.

- Policy divergence widened: China reaffirmed its full ban, while the US/EU/JP continued integrating digital-asset rails into traditional financial architecture.

- Solana flows stayed uniquely resilient, 20 consecutive days of ETF inflows despite spot drifting toward its Jan-2023 AVWAP; BNB remained stable above support.

Our Take:

ETF inflows, treasury accumulation, record derivatives activity and accelerating tokenisation collectively point to early-stage base-building, even as prices stay below key AVWAP levels. Ownership quality improved, rails expanded, and regulated-market participation strengthened — but the market still needs persistent ETF inflows and AVWAP reclaims before a trend-resumption can be confirmed..

Key Points

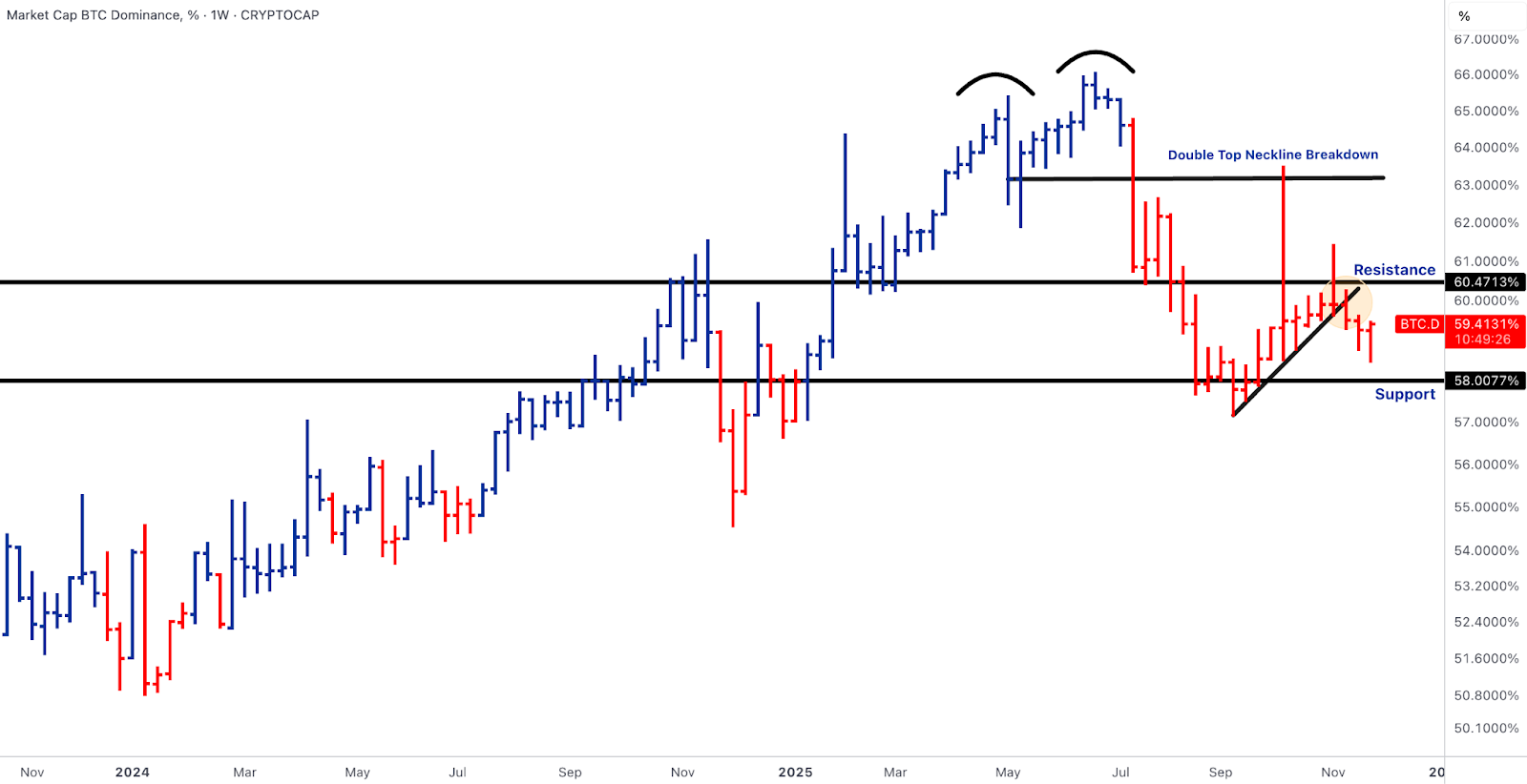

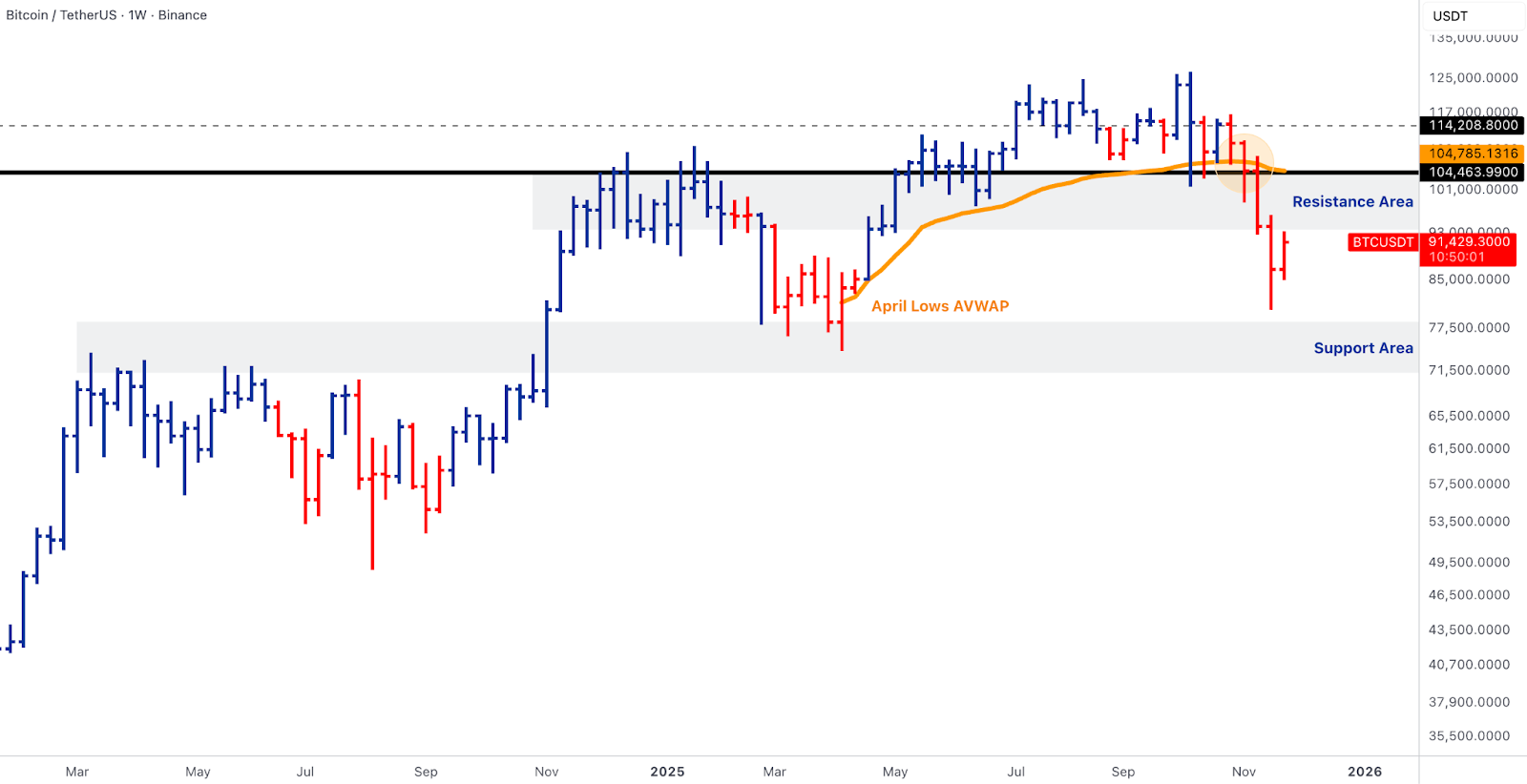

Last week marked the first meaningful turning point for crypto since October. After two weeks of forced selling, BTC and ETH ETFs finally recorded net-positive flows, their first weekly inflows in months. While modest, this shift signals that the mechanical redemptions weighing on the market are easing, and new ETF creations are starting to appear. Prices responded accordingly: BTC stabilised above the low-90ks stress floor, ETH followed suit, and TOTAL3 held its support band rather than sliding to new lows. Bitcoin dominance remained steady around 58–60%, suggesting the market is resolving stress rather than confirming a return to BTC leadership.

Macro conditions supported this stabilisation. US 10-year yields stayed steady at 4.0–4.1%, providing a tight but non-disruptive liquidity environment. Equities showed signs of improvement, with broader market participation increasing despite thinner overall volume, creating a supportive backdrop for risk assets. Cross-market signals, such as the BTC/ES ratio, indicated that equities were absorbing liquidity more efficiently while crypto remained in repair mode.

Institutional activity reinforced the shift from stress to repositioning. CME crypto derivatives hit all-time daily volumes, highlighting active hedging and renewed engagement. Corporates mirrored this trend: miners like Hive and CleanSpark reported record BTC-linked revenues, and treasuries expanded or adjusted their digital asset exposure.

Regulatory dynamics further shaped the environment. China doubled down on its crypto ban and flagged stablecoin risks, while the US, Europe, and Japan accelerated integration, expanding tokenisation and embedding digital assets into regulated financial systems. The result is a clear bifurcation: the East restricts, while the West normalises.

Overall, last week delivered a multi-layered stabilisation. Prices found footing after stress-driven lows, ETF flows turned positive, institutional derivatives activity reached new highs, and real-world digital asset infrastructure continued to expand. The market remains fragile below key AVWAP levels and requires persistent ETF inflows for confirmation, but structurally, foundations strengthened across treasury accumulation, tokenisation momentum, regulated participation, and major-market policy alignment.

BTC - stress floor defended as ETF flows turn positive and institutional rails deepen

- BTC reclaimed ~$91k mid-week, holding the low-90ks stress floor.

- Weekly candle closed above the stress-floor band; April-lows AVWAP (~$100–106k) still defines medium-term resistance.

- BTC ETFs posted first net-positive flows since October, with IBIT and FBTC redemptions easing and new creations returning.

- CME crypto futures hit all-time daily volume, indicating active hedging and institutional re-engagement.

- Public-sector and corporate demand grew: Texas bought $5M IBIT; Metaplanet, Xapo, and SpaceX expanded BTC positions.

- Miners (Hive, Cleanspark) reported record revenues and expanded into AI-compute, showing controlled balance sheets and manageable hash-prices.

- Overall, mechanical selling appears largely cleared, liquidity is returning, and the market is in a rebuild phase, though trend leadership is not yet restored.

Our take: BTC is stabilising after the November unwind. ETF inflows, rising institutional futures activity, and treasury accumulation underpin a solid floor. The market remains below key AVWAP levels, so while recovery is underway, sustained flows and AVWAP reclaims are needed to confirm a broader trend resumption.

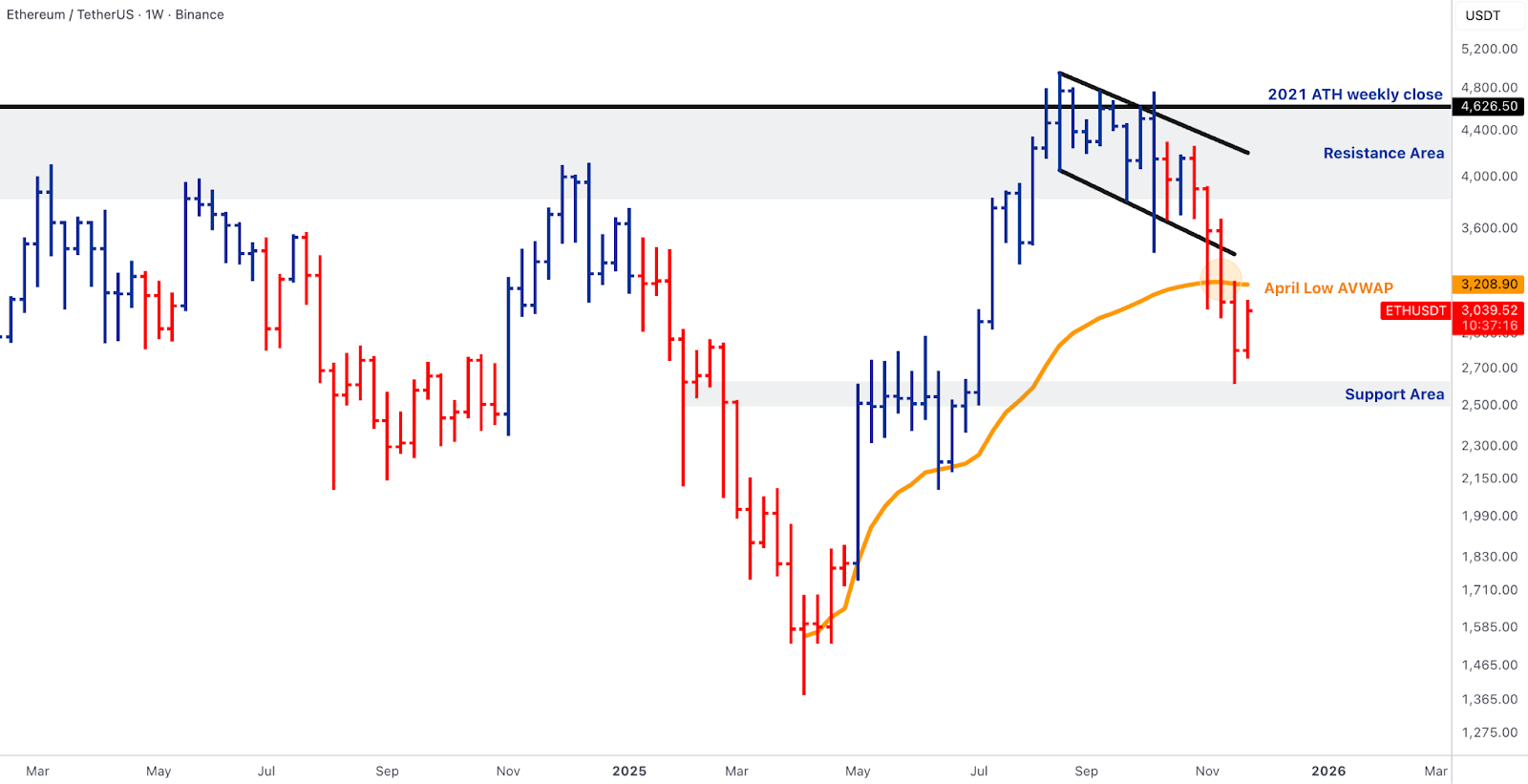

ETH - Stabilising flows, treasury accumulation and strengthening tokenisation rails

- ETH recorded first net-positive ETF flows since October, breaking the prior steady bleed in ETHE products.

- Price stabilised above ~2,600, rebounding with BTC, though the ETH/BTC ratio remains subdued below 0.0342.

- Bitmine expanded its ETH treasury with $44M new purchase plus a $200M commitment, establishing ETH as a corporate treasury asset.

- Tokenisation adoption accelerated: Amundi tokenised a money-market fund on Ethereum; Securitize gained EU approval for a tokenised trading system on Avalanche.

- Protocol-level improvements continued: Fusaka’s block gas limit update signals scaling and throughput readiness, supporting staking yields and institutional usage.

- Structural demand remains strong, with ETF inflows, treasury accumulation, tokenisation adoption, and protocol capacity all improving fundamentals.

Our take: ETH is stabilising alongside BTC but continues to lag in ratio terms. Corporate treasuries and tokenisation initiatives are solidifying ETH’s role as an institutional settlement layer. While price hasn’t reclaimed trend leadership, the underlying structural bid is materially stronger.

Solana & Policy-Aligned L1s - ETF resilience meets treasury volatility

- SOL spot ETFs extended 20 consecutive days of inflows, outperforming BTC and ETH in sustained demand.

- Despite ETF strength, SOL price drifted toward the Jan-2023 AVWAP (~112), reflecting leveraged unwinds and chart-level vulnerability.

- ETF inflows created a structural divergence: SOL accumulated through market stress, while BTC and ETH were still stabilising.

- Treasury positioning remains volatile; corporate adjustments can create micro-shocks that affect short-term price despite long-term fundamentals.

- Regional policy developments shaped L1s: Korea saw the Upbit $37M hack and Naver-Upbit restructuring, highlighting consolidation and AI/blockchain integration in CeFi-adjacent rails.

- BNB remained technically heavy, trading below $1,000 resistance but above ~742 support, acting mainly as a liquidity barometer rather than reflecting protocol weakness.

Our take: SOL’s ETF strength cushions downside and sets up a potential advantage when risk appetite returns, though treasury volatility adds short-term swings. BNB reflects broader market stress rather than asset-specific issues. Both highlight the evolving interplay of ETF flows, treasury management, and policy dynamics in L1 ecosystems.

Conviction Pockets: Where Price and Narrative Align

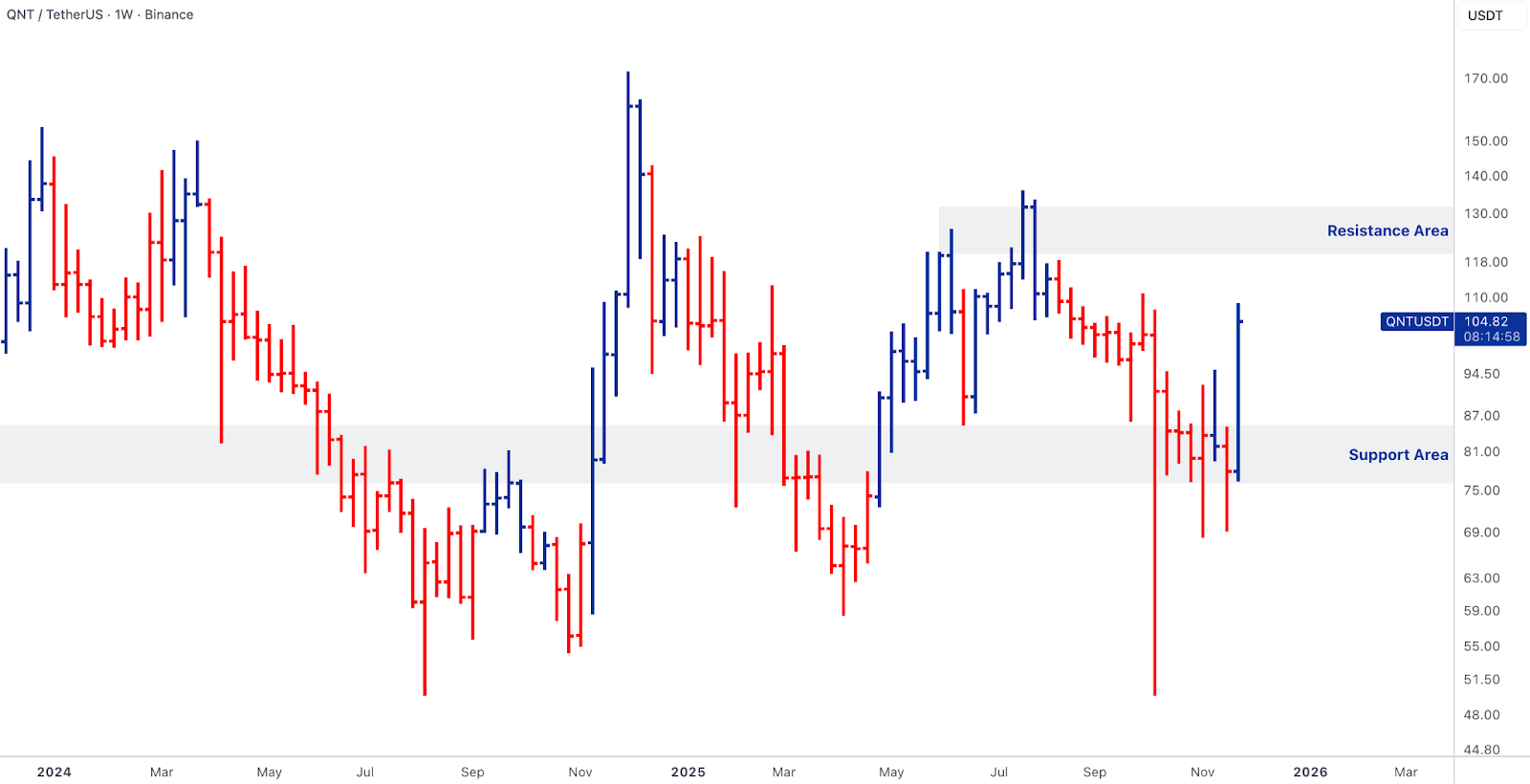

- QNT rebounded sharply from structural support, benefiting from ongoing institutional tokenisation initiatives and regaining visibility as an interoperability asset.

- Kaspa rallied toward overhead resistance despite no discrete catalyst; ETF flows turning positive and BTC stabilisation drove cyclical re-risking. Institutional accumulation (~$15M) and high development activity support its structural case.

Source: TradingView [KAS/USDT]

- Zcash (ZEC) gained a structural boost as Grayscale filed for the first-ever ZEC ETF, reinforcing its role in the privacy-asset narrative and improving regulated liquidity access.

- Monad (MON) stabilised post-mainnet volatility; Magma staking went live and allocation distributions settled, highlighting credible engineering pedigree despite price remaining in a corrective trend.

Our take: These assets demonstrate selective rotation into structural opportunities rather than broad market risk. ETF flows, institutional accumulation, and tokenisation catalysts are driving targeted upside, highlighting the market’s early-stage rebuilding phase beyond the major coins.

Rails & Tokenisation - The strongest pillar

- Visa expanded stablecoin settlement across MEA/EU in partnership with Aquanow, moving integration from pilot to scale.

- US Bancorp tested stablecoin on Stellar; Klarna introduced USD stablecoin via Stripe; Paradigm’s Tempo integrated BNPL flows on-chain.

- Tether USDT0 transfers surpassed $50B, showing transactional adoption is outpacing perceived reserve concerns.

- Tokenisation advanced: Amundi’s tokenised money-market fund on Ethereum; Securitize gained EU approval for a regulated trading system on Avalanche.

- Institutional participation intensified: CME crypto futures and options hit all-time daily volumes, completing the triangle of ETF flows, derivatives depth, and on-chain rails.

Our take: Rails are accelerating even as prices consolidate. Stablecoin adoption, regulated tokenisation, and robust institutional participation are creating a stronger structural foundation for digital assets, signalling that the infrastructure layer is maturing and ready to support sustained growth.

Outlook - Early signs of base-building as structural flows return

- Stabilising ETF flows, record CME participation, and expanding settlement rails support a constructive medium-term outlook.

- BTC tests the low-90ks stress floor, ETH capped near 3.2k AVWAP, and SOL sits atop its Jan-2023 AVWAP despite strong ETF demand.

- Market not yet ready for trend resumption, but structural rebuilding is underway.

- Macro updates this week (PCE, jobless claims, ISM) in a tight but stable 10-year yield environment (~4.1%) could support incremental risk-taking.

- Foundations strengthened: positive ETF flows, accelerating rails, tokenisation progress, surging derivatives activity, and clarified global policy dynamics.

Our take: The market is entering the early stages of base-building. Ownership quality is improving, institutional participation is expanding, and structural flows are returning. Persistent ETF inflows and continued macro stability will be key to confirming trend recovery.

Thanks for reading this week's Market Pulse.

We’re watching flows in real time. If you want early alerts, customised sizing analysis, or routing paths for your trade, we’re here to help you execute on your strategy.

Get in touch with your Relationship Manager.

- The Hex Trust Markets Team