ETF Drains, Privacy Mania and the Rise of Banking-Grade Rails

Market Overview

- Last week reinforced a selective-liquidity regime where capital is rationed, not withdrawn, by a lack of fresh impulse for beta.

- The 10-year Treasury reward's narrow climb (4.05% to 4.15%) confirmed a late-cycle environment and slight tightening of funding conditions.

- Credit data showed slow, measured deterioration (rising consumer/corporate delinquencies), indicating measured systemic friction but no immediate funding stress.

- In the absence of major macro catalysts, the crypto market traded entirely as a flow-led adjustment mechanism, with ETF channels dominating price action.

- ETFs were the primary adjustment mechanism: BTC and ETH ETFs posted some of their largest weekly redemptions since the summer, while SOL ETFs again attracted steady inflows.

- The outflows were a recalibration of exposure at the top of the cycle, not a structural concern. Exchange depth and stablecoin liquidity remained orderly, absorbing the shock without systemic strain.

- Structural adoption accelerated: Harvard's endowment increased its spot BTC ETF exposure, marking a watershed moment for academic allocators.

- Institutional Perimeter strengthened: Visa, JPMorgan, DBS, and MAS advanced tokenised settlement pilots.

- Regulatory alignment advanced: Regulators in the US, UK, Brazil, and Japan pushed forward frameworks on stablecoins, staking, and compliant token issuance.

- The result was a week in which weaker beta met stronger rails. Prices corrected through the most transparent channels, i.e. ETFs, while the underlying infrastructure, policy trajectory and institutional adoption all strengthened.

BTC - AVWAP Lost, Leverage Washed Out, Endowments Step In

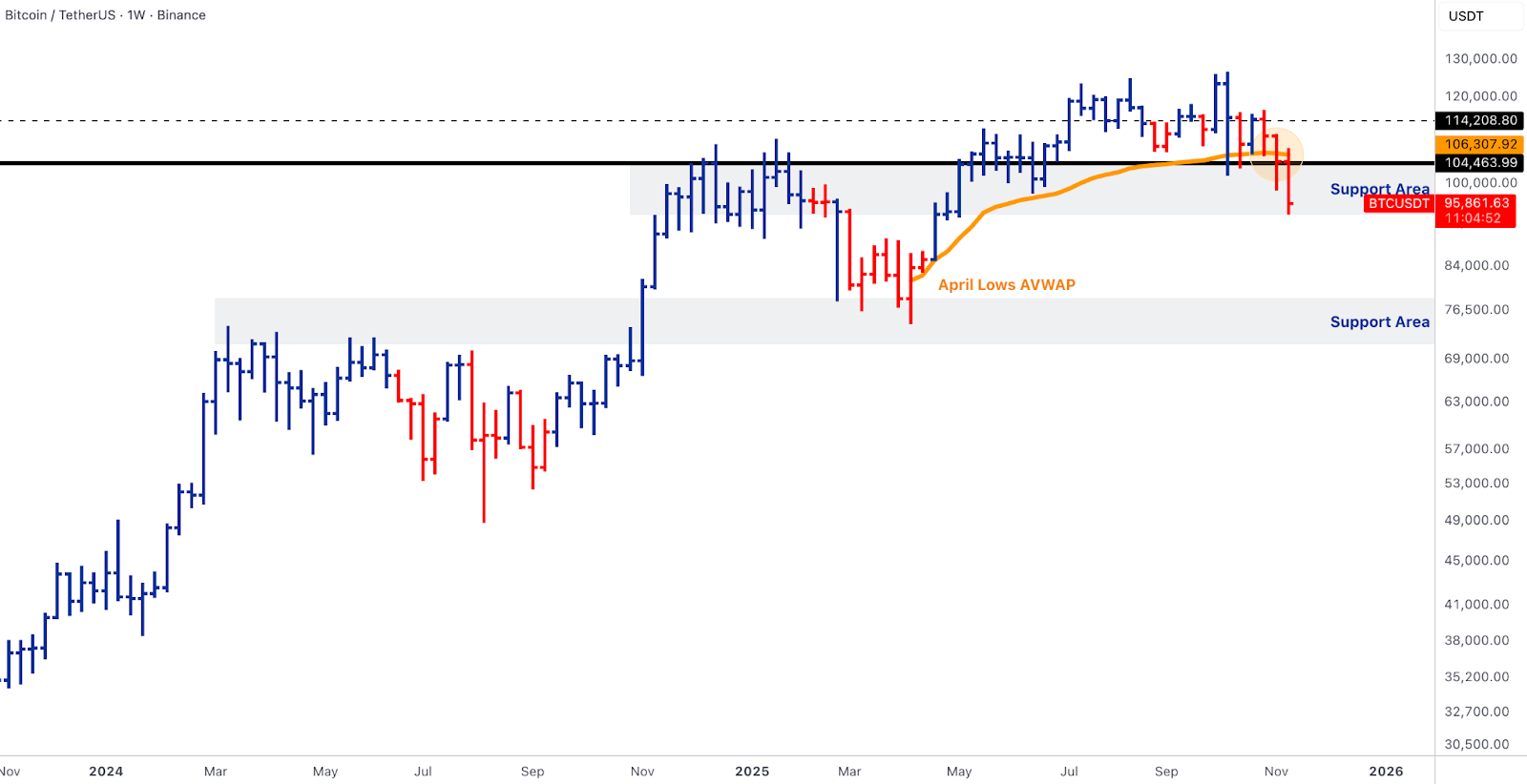

BTC extended last week’s technical break by closing decisively below the April lows AVWAP around $106k and settling near $96k, squarely inside the $93-104k support band highlighted in prior notes. The breakdown converts $106-107k into first resistance, with the previous consolidation shelf at $114-115k and the prior spike highs near $126-128k now acting as progressively tougher supply zones. Below, the next structural support remains the large grey band around $76.5k drawn from the 2024 range, though that only comes into play if the current zone fails. The weekly structure, a continuation bar lower after last week’s rejection at AVWAP, confirms that the bias is now corrective, not a simple sideways pause.

ETF flows were the main incremental shock. Over the five trading days, US spot BTC ETFs saw roughly $1.11B of net outflows, with three particularly heavy days: about $280M out on 12 November, nearly $870M on 13 November, and roughly $460M on 14 November, partially offset by a ~$525M two-day inflow mid-week. Those prints match CoinShares’ observation of more than $1.2B of global crypto ETP outflows centred on US BTC funds. The flow data explain why each intraday bounce back through $100k was sold: ETF channels, which had steadily absorbed supply earlier in the cycle, became net providers of liquidity into a thinning order book.

At the same time, this was not a structural unwind. Harvard’s endowment effectively tripled its BTC ETF holdings over 2024, signalling that the “university endowment” cohort has moved beyond pilot allocations and into programmatic exposure. MicroStrategy reiterated its buy-and-hold stance as Saylor publicly denied any sales; on-chain, whale accumulation and shrinking exchange balances backed up that narrative of sticky long-term ownership. The sharp dip below $100k triggered about $460M of cross-asset liquidations, flushing out late leverage and normalising funding. The combined picture is of a market digesting ETF redemptions with a large, patient holder base underneath: rallies into the $106-115k band are likely to meet ETF-driven selling until flows stabilise, while a decisive break of $93-95k would probably require either a fresh macro shock or evidence that those long-term holders are blinking.

ETH - ETF Headwinds, Ratio Break and Quiet Structural Tailwinds

ETH underperformed across every axis. On USD pairs, it lost the lower boundary of the descending channel that has contained the price since early summer and trades around $3,170, just below the April lows AVWAP near $3,200. Immediate resistance now sits in the $3,500-3,600 zone defined by the underside of the broken channel, with the broader resistance area between $4,000 and $4,300, and the 2021 ATH weekly close at $4,626 is still miles above. Below, the $2,900-3,000 band becomes the first genuine support if AVWAP fails. The ETH/BTC ratio broke its short-term support near 0.034, slipping back into the no-man’s-land between the 0.025 breakout zone and the 0.04 structural resistance. The double-bottom structure built earlier in the year is not invalidated, but neither is it confirmed; until ETH/BTC reclaims roughly 0.034, the short-term tactical signal remains one of potentially weak BTC leadership.

Flows amplified the technical damage. US ETH ETFs bled about $728M over the week, almost entirely through outflows from spot products such as BlackRock’s ETHA and Grayscale’s ETHE, with no offsetting inflows from smaller entrants. Those redemptions mirrored the global pattern, where CoinShares flagged ETH as one of the heaviest laggards among major ETPs. As with BTC, ETF channels turned from structural buyers into marginal sellers just as ETH approached a major AVWAP, converting what might have been a typical pullback into a more forceful de-risking.

Structurally, however, the rails narrative around ETH and EVM continues to deepen. The IRS issued guidance allowing crypto ETPs to stake digital assets, opening the door to potential staked-ETH ETFs or hybrid income products once issuers are comfortable with the framework. Coinbase simultaneously unveiled a compliant public token-sale platform, positioning itself as an “ICO 2.0” venue for regulated distributions that will almost certainly be EVM-first. Circle launched its ARC on-chain FX engine and multi-currency stablecoin programme, effectively turning USDC’s underlying infrastructure into a programmable cross-currency settlement layer that is deeply anchored in the ETH/L2 universe. Together with Visa’s USDC payout pilot and JPMorgan’s JPM Coin deposit-token expansion, EVM rails remain the default environment for institutional tokenisation experiments, even as ETH, the asset endures ETF outflows and ratio pressure. The conclusion is unchanged: ETH is tactically weak but structurally central, and leadership will not rotate back until the ratio turns up and ETF flows at least neutralise.

SOL and BNB - ETF Accumulation versus Tape Damage

Solana’s tape delivered a classic “strong asset under distribution” look. SOL extended its correction from the $200-210 breakdown zone toward roughly $140, firmly below short-term resistance at $200 and the former rising trendline. The next cluster of support sits around $114-115, where the January 2023 lows AVWAP aligns with a broad horizontal demand zone that has repeatedly absorbed risk in prior cycles. As long as that band holds, SOL retains its structural leadership profile, but the message is clear: the market is now willing to tolerate a 35-40% drawdown from the highs in exchange for digesting prior excess.

ETF flows, however, told a very different story. Solana ETFs (BSOL and GSOL) recorded net inflows of about $46.4M over the week, with steady buying on four of the five days and no material outflow session. Since inception, these products have now attracted roughly $380M of capital, and they are doing so in the teeth of a sizeable spot correction. That dynamic stands in contrast to BTC and ETH, and even to the new spot XRP ETF in Australia, which, while posting an impressive $58M in first-day volume, remains tiny in AUM terms compared with the SOL complex. On-chain, the treasury story strengthened too: Upexi, a data-and-tech firm with a Solana-centric narrative, not only added roughly 2.1M SOL to its treasury but also approved a stock buyback programme that explicitly leans on its SOL-linked balance sheet as part of the pitch to equity investors. Despite memecoin froth fading and active addresses retracing to 12-month lows, the asset is increasingly treated as a growth-equity proxy with real corporate-finance hooks rather than just a speculative L1.

BNB, by contrast, delivered its first meaningful retest since the parabolic breakout through $742. Price slipped below the round-number $1,000 level but closed the week comfortably above prior resistance near $742, leaving the breakout structure technically intact, though no longer euphoric. The fundamental tape stayed busy: BlackRock’s BUIDL fund integrated with Binance and is set to launch on BNB Chain, reinforcing BNB’s status as a programmable wrapper for tokenised Treasuries. Standard Chartered pressed ahead with experiments around a stablecoin-linked credit card, and OKX rolled out in-wallet DEX trading that taps Base, Solana and its X Layer, further cementing the logic of exchange-native chains driving transaction and fee volume back to their L1 tokens. BNB continues to behave more like a high-beta exchange equity than a generic L1 bet: as long as the $742 breakout area holds, large allocators will treat dips as opportunities to add a fee-generating rail rather than a pure narrative coin.

Emerging Rotation and Alpha Cluster - DeFi Cash Flows, Privacy Mania, Multi-VM Bets

The alpha cluster remained anchored by privacy mania, adding DeFi cash-flow rerating and infrastructure optionality rather than memecoins.

UNI rallied last week, lifting from the $5.5-6.0 support band, though still trapped beneath the major horizontal resistance around $10.95. The catalyst was clear: Uniswap Labs and the Uniswap Foundation jointly proposed activating the long-debated “fee switch,” redirecting a portion of trading fees from LPs to UNI token-holders, subject to governance, alongside a new framework for continuous clearing auctions aimed at smoothing MEV and order-flow execution. The market is now beginning to treat UNI less as a governance badge and more as a nascent equity-like claim on protocol revenues. While the exact parameters and regulatory optics remain to be finalised, this is one of the clearest examples of a top-tier DeFi venue moving toward explicit, on-chain cash-flow distribution, and the price reaction reflects multiple expansions more than simple beta.

ZEC extended its extraordinary vertical move, with price accelerating from the prior $74-80 base-breakout zone through the May 2021 weekly close near $305 and sprinting past $700 at the high, pushing market cap above $10B at peak. Under the surface, fundamentals have turned meaningfully more constructive: Zcash’s shielded pool has climbed to roughly 23% of circulating supply, with shielded transactions and addresses rising sharply, signalling that actual privacy usage, not just speculation, is driving on-chain activity. Winklevoss-backed Cypherpunk, meanwhile, announced plans to accumulate up to 5% of ZEC’s total supply, seeding the effort with a $58M treasury, effectively acting as a long-term, non-levered buyer of last resort for the asset. Zcash’s co-founder underscored in parallel interviews that demand for financial privacy is structurally rising as surveillance and data-sharing expand globally. The mix of reflexive price action, credible treasury demand and genuine usage growth justifies ZEC’s promotion to a key privacy proxy, but the asymmetry is now skewed heavily toward downside if the narrative cools or if regulators sharpen their focus. The May-2021 close around $305 is the obvious line in the sand: a weekly close back beneath it would mark the end of the blow-off phase.

Infrastructure and L1-adjacent plays also earned a place in the cluster. Injective (INJ) continued to trade heavily on the week, grinding lower toward the $6.0-6.5 area and approaching the next horizontal support around $5.7. On pure price action, it looks like a failed breakout; however, the fundamental story turned decisively more interesting as Injective launched its native EVM mainnet, bringing full Ethereum-equivalent smart-contract support to its high-performance Cosmos-based chain as part of a broader MultiVM roadmap. This allows Ethereum dApps to deploy directly onto Injective without rewriting code while tapping its derivatives-oriented modules and low-latency infrastructure, setting the stage for shared liquidity and state across EVM, WASM and eventually even Solana-style VMs. In other words, price is digesting prior gains at precisely the moment the chain’s addressable market expands, making INJ a classic “fundamentals up, chart down” watchlist candidate for patient capital.

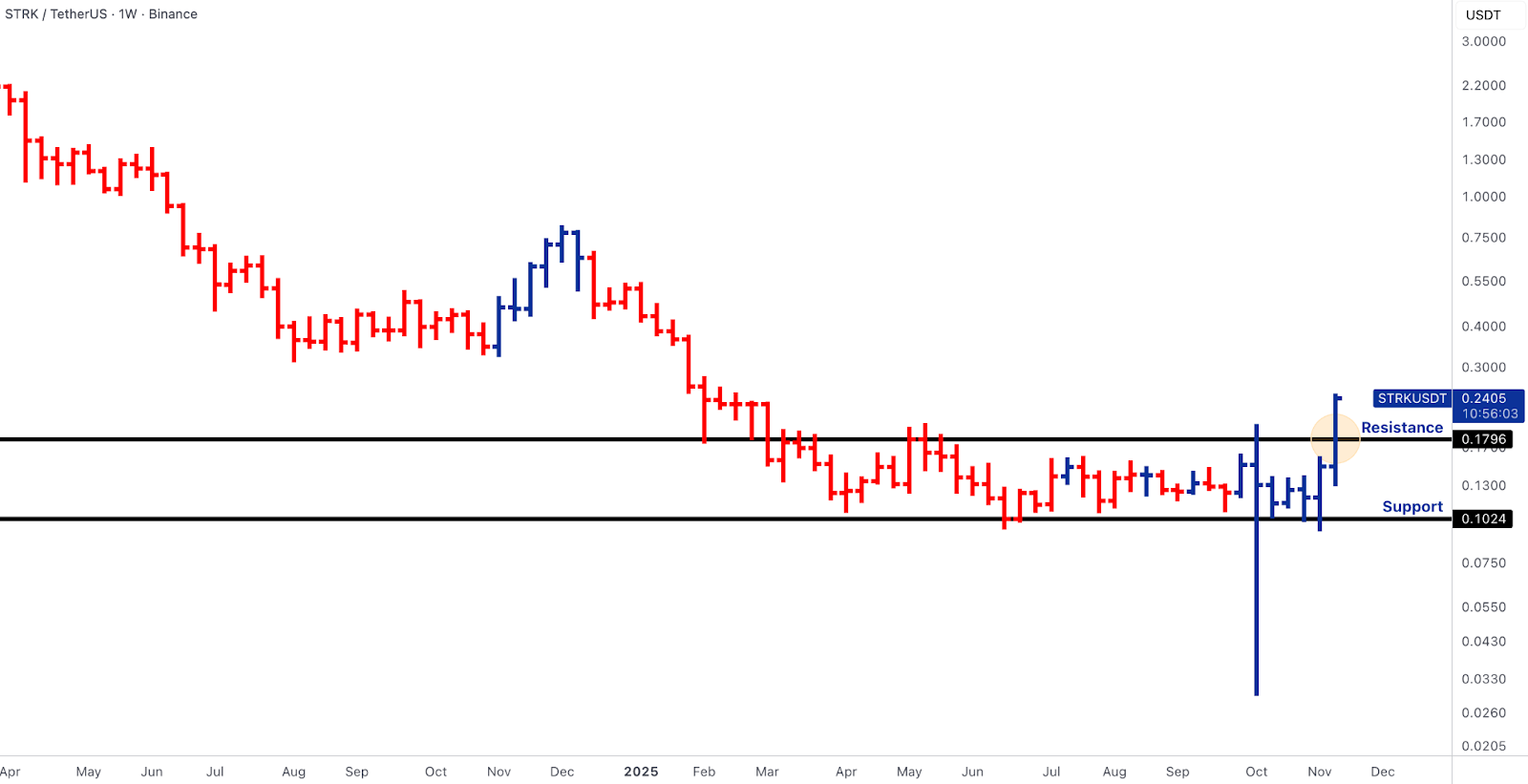

Starknet’s STRK token finally broke free from its bruising downtrend, surging through the long-defended $0.18 resistance to trade above $0.20 and outperforming on the back of by real activity data: Starknet’s DeFi TVL has been climbing sharply, with TVL up ~200% since July and a particularly strong October-November run, plus ~900m STRK staked via the staking program. A lot of flows are into perp DEXs and DeFi apps building on its high-performance L2, combined with incremental progress on Cairo 1.0 tooling and ecosystem grants.

Rails and Tokenisation - Stablecoins, Deposit Tokens and the New FX Stack

If ETFs were the week’s release valve, rails and tokenisation were its quiet power train. On the stablecoin side, Tether was reported to be leading a potential $1.2B funding round into a German robotics startup, continuing its pattern of recycling USDT’s cash-flow engine into off-chain assets and strategic equity stakes. Circle, for its part, delivered a resilient Q3 as USDC revenues held up despite rate-cut chatter, and announced its ARC on-chain FX engine alongside a multi-currency stablecoin programme that effectively turns Circle into a programmable cross-border FX and payments stack. RedStone’s analysis that crypto’s rewards gap is closing as tokenised treasuries and RWA stablecoins proliferate dovetails with this: stablecoins are no longer just “dollars on-chain,” they are increasingly the front-end for rewards, FX and corporate treasury management.

Global payments and card networks moved in lockstep. Visa rolled out a pilot enabling stablecoin payouts to USDC creators and other partners, underscoring its conviction that stablecoins will be a standard settlement asset on its network. Standard Chartered tested a stablecoin-linked credit card product, while DBS and JPMorgan expanded their tokenised-deposit initiatives, including experiments where tokenised deposits act as collateral in repo-style transactions or settle cross-border trades in near-real time. Singapore’s Project Guardian pilots progressed to tokenised bills of lading financed via wholesale CBDC, and Brazil advanced a clearer regulatory framework for domestic crypto service providers, reinforcing the theme that banks and regulators are building parallel fiat-linked rails rather than attempting to shut stablecoins down.

On the capital markets and token-launch side, Coinbase’s forthcoming public token-sale platform, together with SEC Commissioner Paul Atkins’ push to clarify which tokens qualify as securities, and a16z’s policy work around decentralised stablecoins and the so-called Genius Act, sketch the regulatory contour of a future where “compliant ICOs” and bank-grade stablecoin issuance are both possible. R25’s launch of a reward-bearing RWA stablecoin on Polygon, 21Shares’ debut of new multi-asset crypto index funds (including DOGE exposure), and the DTCC’s listing of Bitwise’s Chainlink ETF all highlight that tokenisation is spreading both into on-chain primitives and into traditional wrappers. In parallel, derivatives and prediction-market rails kept building: Lighter raised fresh venture capital at a $1.5B valuation to expand perp-DEX infrastructure, and Polymarket inked an exclusive data-sharing partnership with Yahoo Finance, pointing to a future where on-chain prediction markets are integrated with mainstream financial media. The core message is that, while ETFs bleed, the underlying transaction and issuance rails are becoming more bank-like, more geographically diverse and more tightly wired into existing financial infrastructure.

Outlook

- The reopening of the U.S. government means macro data will soon return to market focus, sharing influence with ETF flows.

- Catalysts to monitor include the Fed meeting minutes and the key NVDA earnings release on Wednesday.

- Critical levels to monitor remain BTC's $93-95k support band, ETH's $3.2k structural defence, and TOTAL3's $0.93T breadth floor.

- The next directional inflexion likely hinges on whether the returning data supports or undermines the current selective-liquidity regime.

- Strategic Stance: The regime remains one of rotation into utility. Focus must remain on long-horizon capital deployment into reward-accretive and regulatory-aligned rails that will govern the asset class's next phase of growth.