Sep 15, 2025

Gear up for a Central Bank action-packed week

Summary:

- A week that shifted from “retest” to “attempted escape”.

- BTC pressed back into the $114-116k reclaim band, ETH closed the week hovering above the 2021 ATH weekly-close band (~$4,626), ETH/BTC defended the ~0.040 shelf, and SOL accelerated through the $202-210 cap toward the $250-253 supply shelf.

- Flows were constructive rather than euphoric: spot ETF prints skewed firmer for BTC and mixed for ETH, derivatives normalised after mid-week wobbles, and liquidity was deep enough for breakouts to stick into the weekend.

- With the FOMC on deck, positioning is long but not crowded.

- The market has clearly marked its levels: acceptance above reclaimed resistance should confirm the turn, while failure there keeps the prior ranges in play.

- Heavy central bank action-packed week, rate cuts expected from Fed, BoC, while BoE and BOJ are expected to hold rates steady.

- A dovish/benign tone from the Fed should keep duration in control, expect to see basis re-steepening, funding trending constructive, and ETF daily prints stringing green.

- A hawkish Fed surprise would likely first show up as basis/funding compression and red ETF prints, then a retest of reclaimed shelves, to see if they act as demand.

- Investors will also be watching the US-China talks in Spain.

1) BTC - pressing the lid, structure intact

- BTC spent the week coiling just beneath and intermittently poking above ~114.2-116k, the same area that capped rebounds throughout late August.

- Intraday tests down into 108–109k were absorbed, keeping price well above the 104-105k support shelf that anchored the late-August wick.

- Spot ETF flows leaned net positive on balance, consistent with derivatives-led de-risking and subsequent re-risk, not spot abandonment: front-end funding and short-tenor basis compressed into mid-week and normalised into the close.

- Gemini’s IPO priced at $28 and traded north of $40 intraday, adding a second public-markets rail alongside ETFs and signalling healthy equity appetite for crypto operators.

- A headline 13-year dormant BTC wallet moved coins, the kind of flow that can disturb microstructure near resistance, but rarely changes the bigger picture when ETF demand is positive.

- The playbook remains clean: weekly acceptance above ~116k re-opens the path toward range highs; failure back beneath ~111.5k risks dragging the tape back toward 102–104k, with the broader $95–105k structural shelf still defining downside risk.

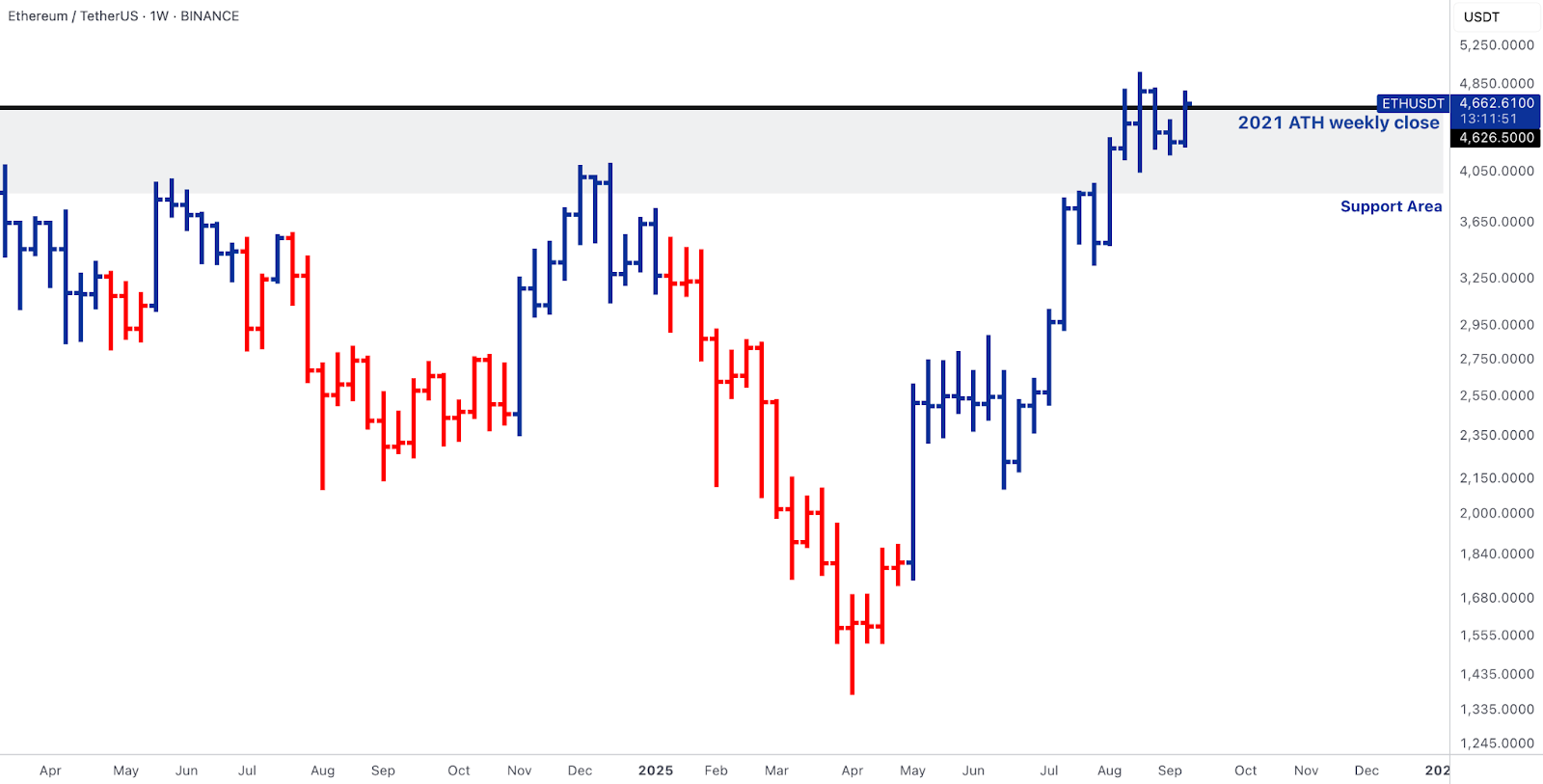

2) ETH - reclaim and absorb; ETH/BTC shelf holds

- ETH held a ~$4.25k weekly low and spent the back half of the week reclaiming and leaning on the 2021 ATH weekly-close band around $4.6k.

- The task from here is classic absorption: convert that prior supply band into durable support via steady closes above it and thinner offer stacks on retests.

- Microstructure aligned with digestion rather than stress, as funding and short tenor basis compressed during the early-week wobble, and normalised into the weekend, with inventories being orderly.

- On the tech side, the Ethereum Foundation published an end-to-end privacy roadmap (private writes, reads and proving), not a near-dated catalyst but a clear, investable utility arc for rollups, RWAs and compliance-sensitive apps.

- Policy-wise, the SEC delayed decisions on staking-enabled ETF proposals (ETH/XRP/SOL), which may cap immediate yield-wrapper optionality, but doesn’t impair spot-ETF demand.

- Relative performance did its job: ETH/BTC defended the 0.038-0.040 shelf and finished the week perched on top of it, keeping the 0.043-0.046 extension in play if acceptance persists; losing ~0.038 would just argue for a 0.034-0.035 back-fill rather than a thesis break, so long as ETH keeps absorbing around the reclaimed band.

3) SOL - stubborn ceiling, then ignition into $250s

- Weeks of higher lows along a rising trendline finally met a decisive push: SOL cleared the $202-210 lid that had repeatedly repelled price and drove toward the next supply at ~$250-253.

- That March-2024 reference has been a stubborn resistance, evidenced by multiple failed probes without higher weekly highs, until now.

- The trade is “prove-it” by weekly acceptance above ~$253 (which would validate a measured extension toward the $275-285 zone), while slips back into $201-206 would simply flag a first retest of the breakout shelf.

- SOL built coiled energy beneath a stubborn shelf, and once that inventory thinned, follow-through was swift.

- Importantly, the demand mix is broadening, and corporate treasury disclosures have begun to show SOL on balance sheets, adding non-speculative demand behind the breakout.

- What confirms durability from here: perps OI continuity without a funding blow-out, spot-led bids on pullbacks (basis not doing the heavy lifting), and no widening in LST spreads. This would signal that demand is absorbing the overhang rather than renting it.

4) Flow-linked Leaders - catalysts that add (or remove) real bid

- PUMP transitioned from thesis to tape. After establishing ~$0.0040 as support, the price rose above that area and accelerated; the core idea keeps being a revenue to buyback to float-compression loop.

- As long as the event-VWAP and the ~$0.0040 shelf hold on pullbacks, and buyback/burn cadence continues to print, the impulse remains programmatically funded rather than purely speculative.

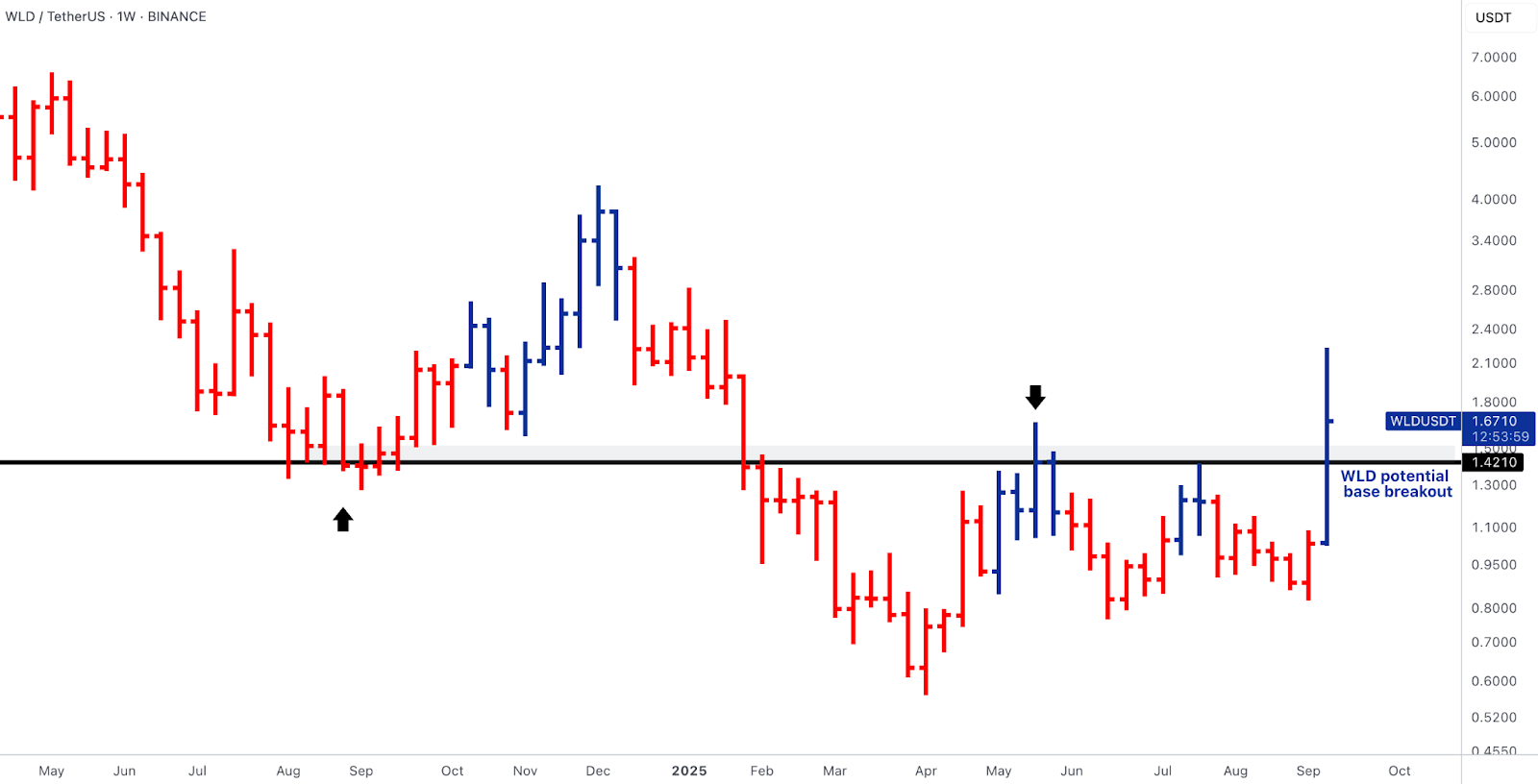

- WLD printed a base breakout through ~$1.42-1.45 after months of range-building and prior rejections.

- The move resets the medium-term structure: holding above the base flips it into support and keeps $1.80-2.00 tractable; repeated closes back below the band would mark a failed breakout.

- What matters now is sustained usage and distribution progress showing up in volumes and fee capture, so the breakout remains flow-validated.

- MNT delivered precisely what prior weeks telegraphed: after grinding against the $1.30-1.45 resistance zone, MNT pushed through to new highs (~$1.60s).

- The constructive read is that L2 activity + native yield rails (mETH) continue to attract deposits and router routes, tightening carry loops on-chain.

- Provided the breakout shelf holds on retests and funding stays contained, momentum can extend into price discovery.

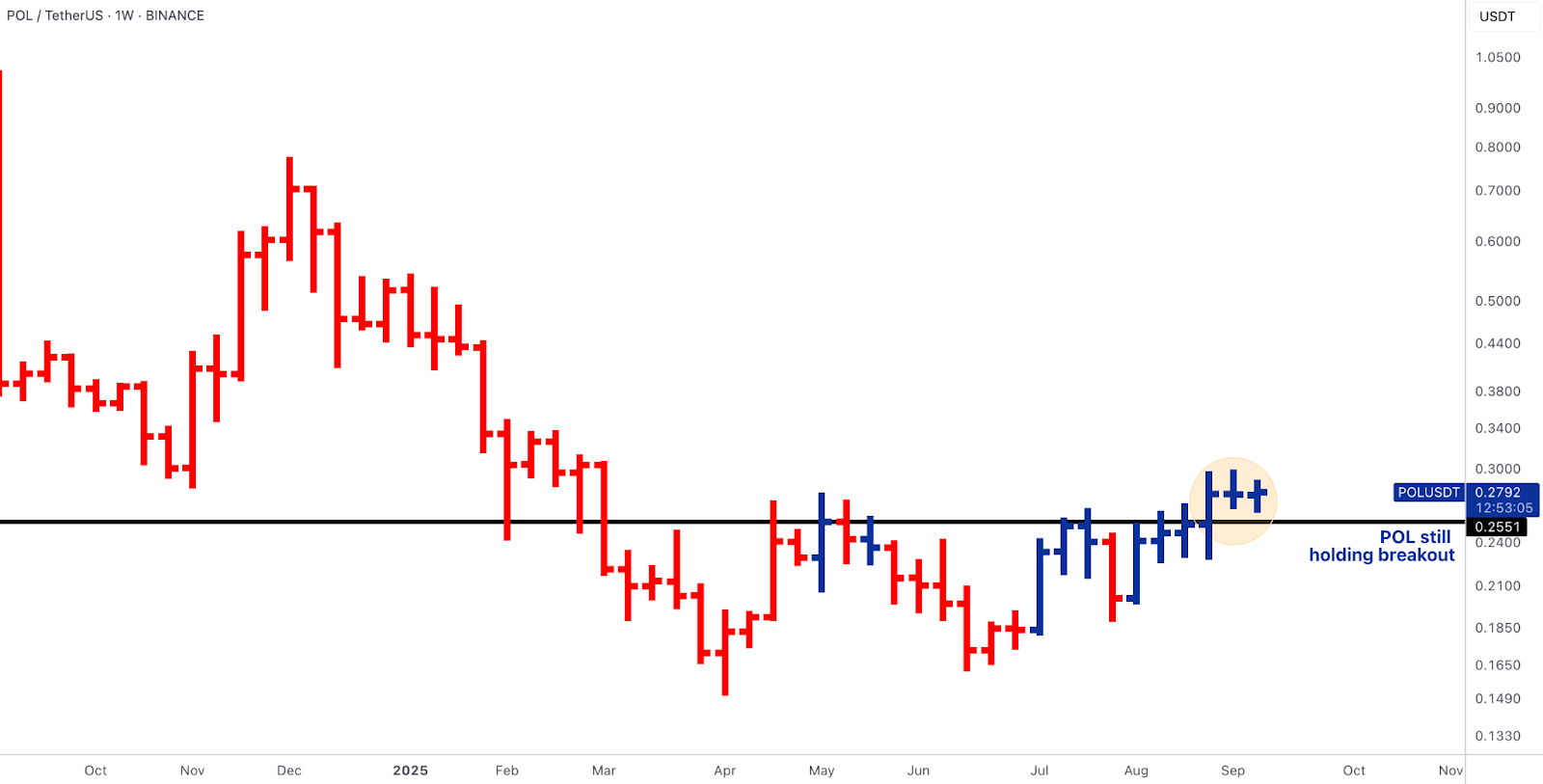

- POL remains orderly above ~$0.255, preserving the base breakout we flagged earlier.

- With migration largely complete and staking/gas economics aligned, accrual now maps cleanly to POL; weekly holds above ~0.255 keep $0.32-0.34 in scope (stretch $0.37-0.38), while a weekly close back below that level would classify the move as failed rather than consolidative.

5) Policy Rails & FOMC - The next-leg gatekeeper

- Institutional plumbing improved in ways that matter for real flow: Binance and Franklin Templeton advanced a tokenisation distribution tie-up, strengthening the RWA pipeline that pulls fiat balance sheets on-chain, while Tether’s work on a “USAT” stablecoin (if launched) would expand dollar-rail capacity that historically tightens spreads and deepens top-of-book on bounce days.

- With the Fed decision mid-week, policy now decides whether this week’s reclaim attempts confirm or fade.

- A dovish/benign tone should keep duration in control, validating BTC weekly acceptance above ~116k and ETH holds above the ~$4.6k band, with basis re-steepening, funding trending constructive, and ETF daily prints stringing green.

- A hawkish surprise would likely first show up as basis/funding compression and red ETF prints, then a retest of reclaimed shelves, to see if they act as demand.

- Positioning is constructive but not stretched, so confirmation or rejection should be visible quickly in ETF cadence, derivatives term-structure, and how those shelves trade in the 24-48 hours after the announcement.

6) Outlook for the week

- Heavy central bank action-packed week, rate cuts expected from Fed, BoC, while BoE and BOJ are expected to hold rates steady.

- Dovish and hawkish surprise reaction from the Fed was mentioned in the previous session.

- Investors will be keeping a close eye on the talks between the US and China in Spain, which started Sunday, high up on the agenda, including the upcoming deadline to divest TikTok and US tariffs.

- China’s retail sales and industrial production will be released on Monday.

- A slew of US data is also due later this week, including retail sales, industrial output, housing starts and weekly jobless claims.

Oops! Something went wrong while submitting the form.