Aug 11, 2025

Recipe for Altcoins Season brewing in the kitchen

Summary:

- Bitcoin touched a new ATH of over $124,000 last week, but ETH stole the spotlight with flows.

- ETH leadership this week was flows-first, price-second. US Spot ETH ETFs made a remarkable record of over $1Bn net-flow day.

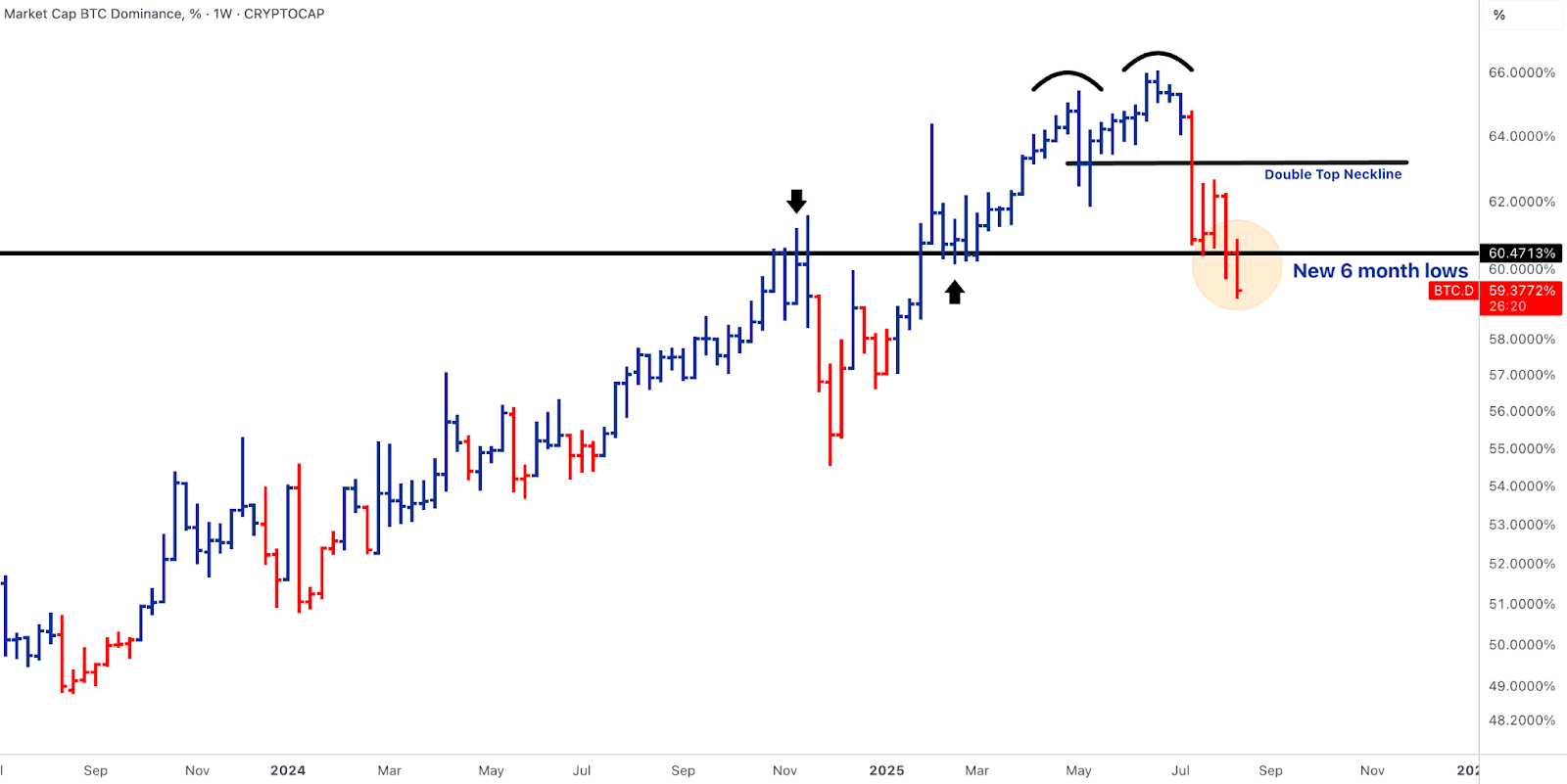

- Despite BTC printing new ATH but Bitcoin’s dominance broke to new 6-month lows (~59%–60%). This is a strong signal of a leadership handoff as capital rotates into higher beta altcoins.

- Front-end basis and perps funding re-normalised, and downside skew bled back toward neutral even as Bitcoin’s dominance continued to leak, i.e. classic rotation-without-stress.

- The clear divergence between BTC vs ETH volatility further supports this narrative.

- All eyes are on Jerome Powell’s speech at the Jackson Hole Symposium, and worth keeping a tab on the US-Ukraine talks.

ETH ETF engine re-engages; leadership is flow-confirmed

- ETH leadership this week was flows-first, price-second. After the early-August reset, U.S. spot ETH ETFs printed two of their largest daily inflows since launch mid-week and Friday, restoring a multi-day positive streak and outpacing BTC ETFs on several sessions.

- Spot held above $4k into the back half as cash demand re-tightened exchange float.

- Microstructure matched the tape as front-end funding and short-tenor basis, which compressed during the prior shock, normalised as bids returned.

- Technically, ETH/BTC’s July breakout is still running a clean post-breakout retest as pullbacks attracted demand and relative momentum stayed constructive.

- The sequence of ETF shock, stabilisation and cash inflow re-acceleration argues this is cash-flow validation, not a squeeze as leadership is re-established, not rented.

- The ETH/BTC July breakout continues to track a textbook playbook. After clearing the 0.0250 neckline, the pair has driven into the first major weekly resistance at ~0.04 (resistance we pointed out last week).

- This is the prior breakdown zone and the natural place for the first reaction. Acceptance above ~0.04 on a weekly close would confirm trend extension and open room toward the next liquidity band (~0.046), while failure/close back below ~0.032 would point to a standard post-breakout retest rather than a trend failure.

- The fact that we arrived here on re-accelerating ETH ETF inflows argues the test is flow-supported, not purely technical.

BTC ETFs stabilise; dominance stays heavy; Gemini IPO adds a capital-markets pillar

- BTC set new all-time highs this week, but the more important signal was relative: BTC dominance broke to new 6-month lows (~59%–60%). That tells you the rally is not monolithic; it’s broadening.

- Flow-wise, U.S. spot BTC ETFs were net-positive on several sessions (incl. a large single-fund intake late week), holding the 113–119k base.

- But incremental risk budgets chased ETH and select alts, helped by near-record ETH ETF days, so the TOTAL2 market cap index outpaced BTC, and BTC.D rolled over.

- Microstructure matched the tape: after a brief rates/FX wobble mid-week on the US PPI release, front-end basis and perps funding re-normalised, and downside skew bled back toward neutral even as BTC.D continued to leak, i.e. classic rotation-without-stress.

- Printing ATHs without dominance confirms a leadership hand-off, not a tired top.

- The reserve-asset channel (ETFs, balance sheets) kept BTC structurally supported, while alpha migrated to flows-in-favour sectors (ETH, infra rails, cross-chain/messaging).

- Until BTC.D reclaims ~62% on a weekly close, the base case is ongoing breadth rather than a snap-back to BTC-only leadership.

- On Aug 16, Gemini named bulge-bracket bookrunners for its Nasdaq IPO, evidence that the public-equity funding rail is reopening for crypto operators. That complements the ETF channel and de-risks the medium-term reserve-asset/exchange narrative that helped anchor BTC’s base through volatility.

- Heavy BTC.D with a stable BTC range is rotation without stress; ETF behaviour looks like positioning normalisation, while the IPO pipeline underscores that capital formation is alive.

- The recipe for a rotation into altcoins is here, and to add to the narrative is the compression of BTC volatility. Shall Bitcoin continue to sustain this range pause, investors will venture out seeking higher returns through higher beta names altcoins.

- And evidence supporting this narrative, as we have seen, Bitcoin’s volatility has been compressed over the past few months. Clear divergence with ETH as ETH’s volatility continues to creep up over the same period.

LayerZero (ZRO): Stargate consolidation and dated unlock create a tradable event path

- LayerZero proposed consolidating Stargate (STG) into ZRO, retiring STG and unifying governance and economic accrual under a single token.

- Markets repriced both tokens because consolidation removes token fragmentation and clarifies value capture (bridge revenues/treasury levers can map to ZRO).

- Near-term, a dated unlock (~25–26M ZRO around Aug 20) introduces a measurable supply overhang, creating a two-sided, event-driven setup (structural rerate from unification vs issuance into an unlock window).

- This week’s flows into ZRO priced a corporate-action rerate (consolidation mechanics) plus a calendar catalyst (unlock).

- Expect perp basis and borrow spreads to reflect that into the date; post-event resolution hinges on message throughput (LayerZero usage) and the STG to ZRO migration pace.

Distribution rails: Coinbase in-app DEX routing pushes liquidity discovery into Base venues (AERO)

- Coinbase continued rolling out in-app DEX trading to U.S. users (ex-NY), routing via 0x/1inch into Base-native DEXes (e.g., Aerodrome, Uniswap).

- That moves liquidity discovery inside a >100M-user retail gateway, compressing the listing-to-depth window for Base assets.

- The tape reflected it: AERO volumes/fees/TVL remained elevated as more order-flow surfaced in-app.

- This remains a distribution-side shock as discoverability, depth and fee velocity now happen inside the main app.

- In an alts over BTC regime, rails that upgrade access and surface area (not just listings) become price-relevant quickly for venue tokens.

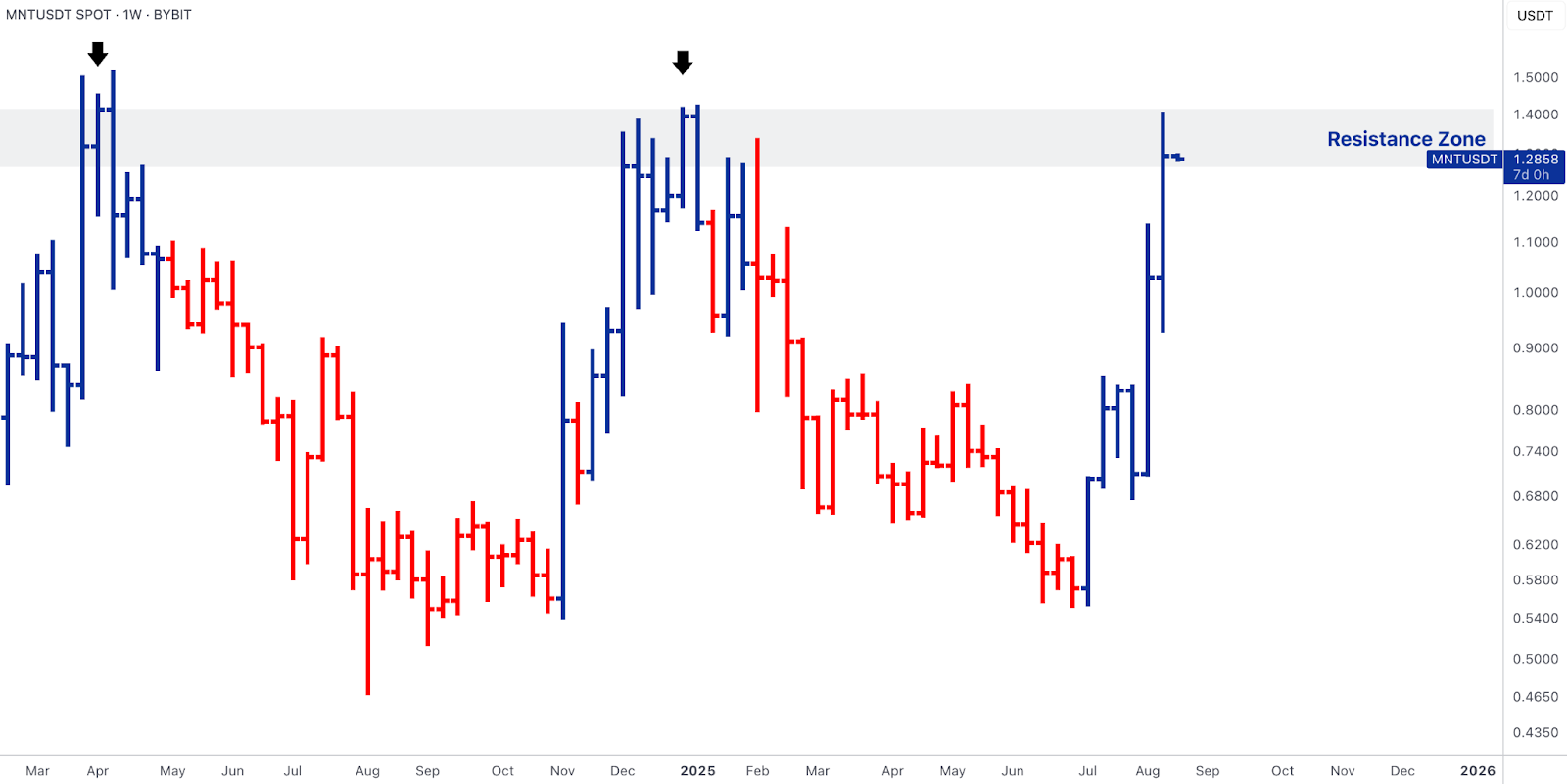

Mantle: L2 beta with native yield rails (mETH) turned ETH above $4k into a sustained bid

- MNT caught a clean rotation bid this week and is pressing back into the March 2024 swing zone, now within striking distance of the late-2024 cycle highs.

- The advance wasn’t a wick-and-fade: spot strength was confirmed by healthier depth on the main WETH/USDC pairs, tighter spreads, and a steady rebuild in perps contango rather than blow-off funding.

- Router telemetry showed more best-price routes landing on Mantle, and mETH (Mantle’s native LST/restaking rail) kept absorbing deposits, which tightened the carry loop across on-chain venues.

- In other words, the bid lined up across spot liquidity, derivatives microstructure, and yield rails, exactly the mix that sustains L2 leadership when BTC.D is making 6-month lows and ETH held above $4k.

- Mantle is functioning as ETH-beta-plus with embedded carry: as ETH ETF inflows re-accelerated, risk broadened, and Mantle captured both the transaction flow (L2 throughput, cheaper execution) and the yield leg via mETH.

- As long as BTC.D stays heavy and ETH leadership holds, MNT/ETH has room to extend through the prior March/late-2024 highs into price discovery.

- The tell for durability will be simple: bridge net inflows over outflows, mETH supply growth with a stable peg, router share that continues to land on Mantle pools, and funding that remains constructive, not euphoric.

Outlook for the Week

- Markets trading sidelines as volatility dropped across asset classes ahead of Fed Chairman Jerome Powell’s speech at the annual Jackson Hole Symposium scheduled for 21-23 Aug this week.

- Traders are implying an 82.7% chance of a 25bps cut in the September FOMC meeting.

- Investors also await details of the US-Ukraine talks later today on Monday.

- Solid corporate earnings season so far as S&P 500 EPS rose 11% YoY and 58% of companies raised their full year guidance.

- This week’s earnings will give us some guidance on the health of consumer spending, with Home Depot, Target, Lowe’s and Walmart earnings due.

Oops! Something went wrong while submitting the form.