Stabilisation Under Tension: Institutional Flows Return While Macro Risk Lingers

Key Facts

- BTC ETF flows stabilised and turned modestly positive through the week, signalling the first improvement in institutional demand since the recent drawdown.

- BTC traded between $66k-$72k, repeatedly testing the $71k resistance shelf but failing to reclaim the higher liquidity band.

- BTC dominance remains locked inside the 58-60% range, following the earlier double-top breakdown (chart below).

- TOTAL3 (crypto market cap excluding BTC & ETH) continues to stabilise near the $720B support zone, still below the prior resistance cluster around $900B.

- Geopolitical volatility tied to the Iran conflict and Hormuz shipping risks continues to influence broader risk sentiment and energy markets.

- The BTC/ES ratio rebounded from the ~9.5 cycle low and is now attempting to reclaim the 10-11 support band, suggesting crypto is beginning to stabilise relative to equities after the recent cross-asset risk unwind.

Our take: The market appears to be transitioning from forced liquidation toward early stabilisation, though the structural repair process remains incomplete. Institutional flows have improved, with ETF demand stabilising and downside momentum easing, yet price action across majors continues to trade below key reclaim levels. BTC dominance holding within the 58-60% range following the earlier distribution phase suggests that the market is gradually moving away from a pure BTC-led regime, but TOTAL3’s inability to reclaim the higher liquidity band confirms that broad alt participation has not yet returned. In parallel, the rebound in the BTC/ES ratio from cycle lows indicates that crypto’s relative performance versus equities is beginning to stabilise after the recent cross-asset risk unwind. Taken together, the data points to a market shifting from deleveraging toward consolidation, where improving liquidity conditions are emerging beneath a still-fragile technical structure.

Bitcoin

- BTC traded primarily between $66k and $72k during the week.

- The market continues to react to the August-low anchored VWAP near $88k and the cycle-high AVWAP near $104k, both of which remain overhead resistance (chart below).

- Price is currently attempting to reclaim the $71k resistance area, previously a key breakdown level.

- Options positioning increasingly reflects expectations of a potential move toward $80k, though the level has not yet been technically reclaimed.

- Spot BTC ETFs returned to net inflows on the week, indicating early signs of institutional re-engagement following the recent liquidation phase.

- Macro sensitivity remains elevated as markets respond to geopolitical developments and shifting inflation expectations.

Our take: Bitcoin’s price action currently resembles a retest of broken support rather than a confirmed reversal. Institutional flows have improved, but the inability to decisively reclaim the $71k-$78k region indicates that supply remains active on rallies. Structurally, BTC is attempting to build a higher-low base following the recent liquidation phase, yet the broader trend will remain uncertain until price can sustain acceptance above the former breakdown shelf. For now, the market is stabilising, but conviction remains limited.

Ethereum

- Ethereum traded around $2,100 during the week.

Price remains below both the June 2022 AVWAP (~$2,369) and the April-low anchored VWAP (~$3,025), which continue to act as major resistance levels. - BlackRock’s staked Ethereum ETF launched with strong initial flows, signalling institutional demand for regulated rewards exposure.

- The Ethereum Foundation sold 5,000 ETH OTC to Tom Lee’s BitMine in a ~$10M transaction.

- BitMine expanded its ETH treasury to over 4.5M ETH, reinforcing the emerging institutional accumulation narrative.

- Spot ETH ETFs recorded modest net inflows, supported by strong initial demand for BlackRock’s newly launched staked Ethereum ETF.

Our take: The Ethereum narrative improved materially this week, even though the price structure remains weak. The launch of a staked ETH ETF introduces a regulated pathway for rewards capture, which strengthens the long-term institutional case for Ethereum as an income-generating asset rather than purely a speculative token. However, the chart still reflects a recovery phase rather than leadership, with ETH trading below multiple structural VWAP levels and ETH/BTC hovering near key support. Institutional validation is improving, but price leadership has not yet returned.

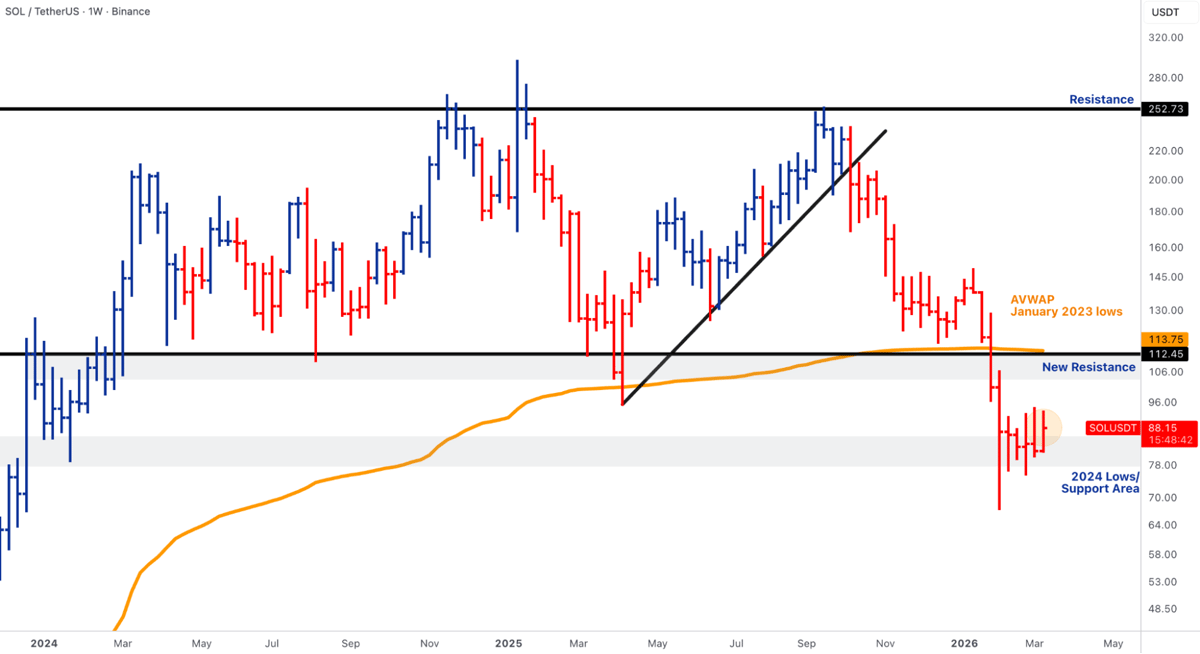

Solana & BNB

- SOL remains below the $112-$115 reclaimed resistance zone (previously January-2023 anchored VWAP).

- Price continues to consolidate near the 2024 lows around $80-$90, forming a potential stabilisation base.

- Institutional exposure to SOL remained broadly stable, with crypto investment products tracking the asset, posting roughly neutral weekly flows as the market continues to rebuild positioning.

- BNB rebounded toward the $660 area, approaching the former breakout level near $742, which now acts as resistance.

- Solana ecosystem activity remains robust, with Pump.fun reportedly becoming the first Solana platform to surpass $1 billion in revenue.

Our take: Solana continues to display strong application-layer activity despite a technically damaged price structure. Usage metrics remain among the strongest in the industry, but SOL itself remains trapped below the key reclaim zone that would signal a trend reversal. BNB’s recovery toward its prior breakout level highlights similar dynamics: the ecosystem remains fundamentally stable, yet price action still reflects a broader market repair process. Neither asset has yet regained leadership status, but both are showing signs of stabilisation.

Alpha Cluster - Early Signs of Selective Rotation

- Bittensor (TAO) rallied more than 50% during the week, leading performance among large-cap altcoins.

- Render (RNDR) gained over 30%, reflecting renewed interest in decentralised GPU infrastructure.

- TRUMP memecoin rose roughly 34% following promotional events and whale accumulation.

- The rally coincided with continued discussion around AI infrastructure expansion and decentralised compute networks.

Our take: The week’s strongest performers suggest that the first pockets of rotation are emerging not in traditional Layer-1 leadership but in AI-linked infrastructure tokens. Both TAO and RNDR sit at the intersection of decentralised networks and the accelerating global investment cycle in artificial intelligence infrastructure. While the moves remain selective rather than broad-based, they highlight how investors are beginning to reintroduce risk in specific narrative-driven sectors rather than across the entire altcoin complex. The sharp rally in memecoins such as TRUMP also hints at a gradual return of speculative liquidity, though it remains far from the euphoric conditions typically associated with full altseason.

Rails & Institutional Infrastructure

- HSBC and Standard Chartered advanced stablecoin initiatives in Hong Kong.

- Wells Fargo filed a trademark covering crypto trading, payments, and tokenisation services.

- Nasdaq partnered with Kraken’s parent company Payward to connect tokenised equities with DeFi networks.

- Coinbase expanded crypto futures trading in Europe.

- Tether invested in programmable finance infrastructure on Bitcoin, backing Ark Labs.

Our take: While price action remains volatile, the institutional infrastructure surrounding crypto continues to advance rapidly. The expansion of stablecoin rails, tokenised financial instruments, and regulated derivatives markets suggests that traditional finance institutions are steadily integrating blockchain-based systems into their existing infrastructure. This process is unlikely to drive immediate price appreciation, but it represents one of the most important structural trends in the industry: the gradual financialization of blockchain rails.

Outlook - Macro and Geopolitical Volatility to Drive Direction

- The upcoming week will be dominated by the Federal Reserve policy decision.

- Key macro releases include the US Producer Price Index (PPI) and industrial production data.

- Additional indicators, such as existing home sales and regional manufacturing surveys, will provide further insight into economic momentum.

- Global central-bank decisions from the Bank of England, ECB, Swiss National Bank, and Bank of Japan will also shape liquidity expectations.

- Markets remain sensitive to geopolitical developments tied to energy markets and shipping security in the Strait of Hormuz.

Our take: Macro conditions will likely continue to dictate short-term market direction. If inflation data remains contained and central banks maintain a cautious but stable policy stance, the recent stabilisation in crypto could extend into a broader recovery phase. Conversely, renewed inflation pressure or escalating geopolitical tensions could quickly reintroduce volatility across risk assets. For now, the market appears to be transitioning from liquidation toward consolidation, but confirmation of a new trend will depend on both macro stability and the ability of crypto markets to reclaim key technical levels.

Thanks for reading this week's Market Pulse.