Jul 28, 2025

Rotation, not Repricing, Defines Market Tone

Summary

- Crypto paused this week amid strong equity outperformance, with rotation, not repricing, defining market tone.

- BTC.D failed to reclaim its neckline after last week’s breakdown, reinforcing a structural shift toward alt-driven narratives.

- 80,000 BTC sales from a Satoshi-era Bitcoin whale created a short-lived spook with Bitcoin briefly dipping below $115,000 before a quick recovery.

- ETH flows surged, but the token lagged as capital rotated into Solana and RWAs.

- Catalysts behind the ETH rotation narrative: Continued Institutional Demand from ETF, drop in BTC dominance while ETH/BTC ratio jumped, 10 year anniversary.

- SOL maintained its breakout and ecosystem momentum, while TON edged toward a technical breakout on the back of its U.S. wallet launch.

- Institutional interest continued to build around tokenization rails, with OSL’s $300M raise and CCIP traction underscoring the crypto infra buildout.

- The market remains selective, narrative-driven, and technically anchored, awaiting a broader reacceleration.

- With crypto-equities correlation remaining positively intact, stock markets' small celebration for Trump’s EU trade agreement and anticipated US-China trade truce extension has boosted cryptomarket to start the week in the green.

- Action-packed week with megacap earnings (e.g Apple, Microsoft, Amazon) and Fed, BOJ meetings due this week.

Macro Signals Pause as Crypto Cools with Rotation, Not Repricing, Dominating

- U.S. equities again took the lead this week, with both the S&P 500 and Nasdaq reaching new highs (S&P +1.5%, Nasdaq +1.4%).

- June core PCE inflation printed at 2.6% YoY (0.1% MoM), aligning with expectations and offering limited impetus for any immediate rate cuts.

- 2-Year Treasury yield settled at 3.92%, and the U.S. Dollar Index (DXY) closed around 97.67, rejecting prior resistance and signaling currency stability without safe-haven pressure.

- Total crypto market cap was flat WoW, led by BTC and select alts. Stablecoin supply growth was muted (+$100M) and DeFi TVL barely budged to $106.4B.

- Institutional flows favored thematic exposure, staking, tokenization infrastructure, messaging rails, rather than broad market beta.

- This is not a risk-off environment, but a tactical pause.

- Equities continue to benefit from macro stability and positioning momentum, while crypto waits for fresh catalysts.

- Until continued ETF throughput with staking-enabled ETFs, or credible macro shocks emerge, crypto remains in a rotation phase: narrow, selective, and driven by narrative-specific flows.

BTC Dominance Rejected at 63%, Rotation Signals Structural Inflection

- Following last week’s double-top breakdown, Bitcoin Dominance (BTC.D) staged a modest rebound, retracing to ~62.5% before failing at former support turned resistance.

- The rejection, paired with persistent bearish RSI divergence on the weekly chart, reaffirms the potential loss of structural trend, a 13-month regime that began in June 2023.

- BTC.D closed the week near 61.3%, validating the neckline as a technical ceiling and reinforcing the shift toward alt-led dispersion.

- This isn’t just a chart anomaly, it reflects deeper reallocations in market structure. Despite a subdued BTC spot gain of ~0.6%, ETF inflows into ETH surged to ~$1.8B, outpacing BTC ETF net additions, which totaled a modest ~$72.3M.

- At the same time, news that Galaxy facilitated 80,000 BTC sales from a Satoshi-era Bitcoin whale, caused BTC to briefly drop below $115,000 before quickly recovering. This is a testament to liquidity resilience and the absorption power of long-only capital.

- BTC remains institutionally anchored, but the marginal bid is rotating elsewhere.

- TOTAL2 (market cap ex-BTC) ended the week down just ~1.5%, recovering from an intraweek drawdown of nearly 7%, as ETH, SOL, and RWA-adjacent names saw renewed inflows.

- This underscores a more selective, thesis-driven rotation, not a broad altcoin rally. The emerging pattern of BTC consolidation, dominance rejection, alt narratives absorbing flow, mirrors early-stage rotation regimes seen in prior cycles.

- Should BTC.D decisively breach 60%, it would mark the first confirmed dominance reversal since early 2021, and formally initiate a structurally broader risk-on environment for the crypto complex.

ETH Holds Ground, Structural Bid Firms Despite Underperformance

- ETH ended the week broadly flat near $3,750, underperforming top alts as capital rotated toward SOL and select mid-cap beta.

- Yet under the surface, ETH’s structural bid continues to firm with US spot ETH ETF recording 16 consecutive days of inflows. Net inflows into ETH ETFs reached ~$1.81B, the largest weekly print since launch, lifting cumulative AUM above 2.1M ETH (~1.75% of supply).

- On-chain fundamentals reinforce this: total staked ETH climbed to 36.2M, while exchange balances declined to 8.85M ETH, continuing the tightening liquid float environment.

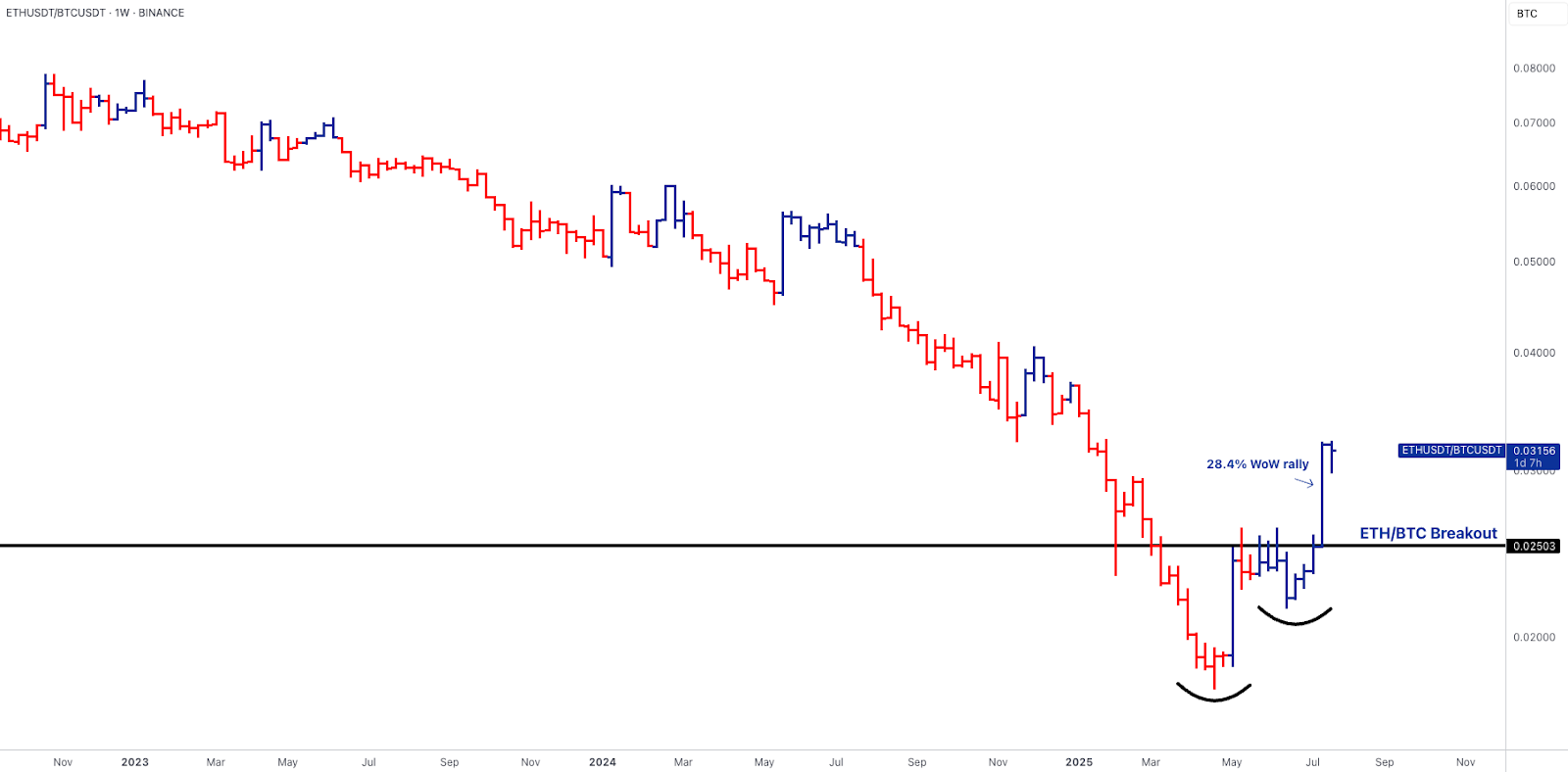

- ETH/BTC ratio pulled back modestly after last week’s stellar rally and breakout above 0.025, but remains above short-term support at 0.03.

- This is less a reversal than a rotation pause. While short-term flows chase alt-beta upside elsewhere, ETH’s dual yield and institutional alignment continue to attract sticky capital.

- Technically, ETH would confirm narrative and technical strength by, at least, making new 52-week highs to confirm leadership.

- With staking, ETF flows, 10 year anniversary context and treasury allocations now reinforcing each other, ETH remains the most structurally sound large-cap in crypto, even as near-term relative performance may consolidate.

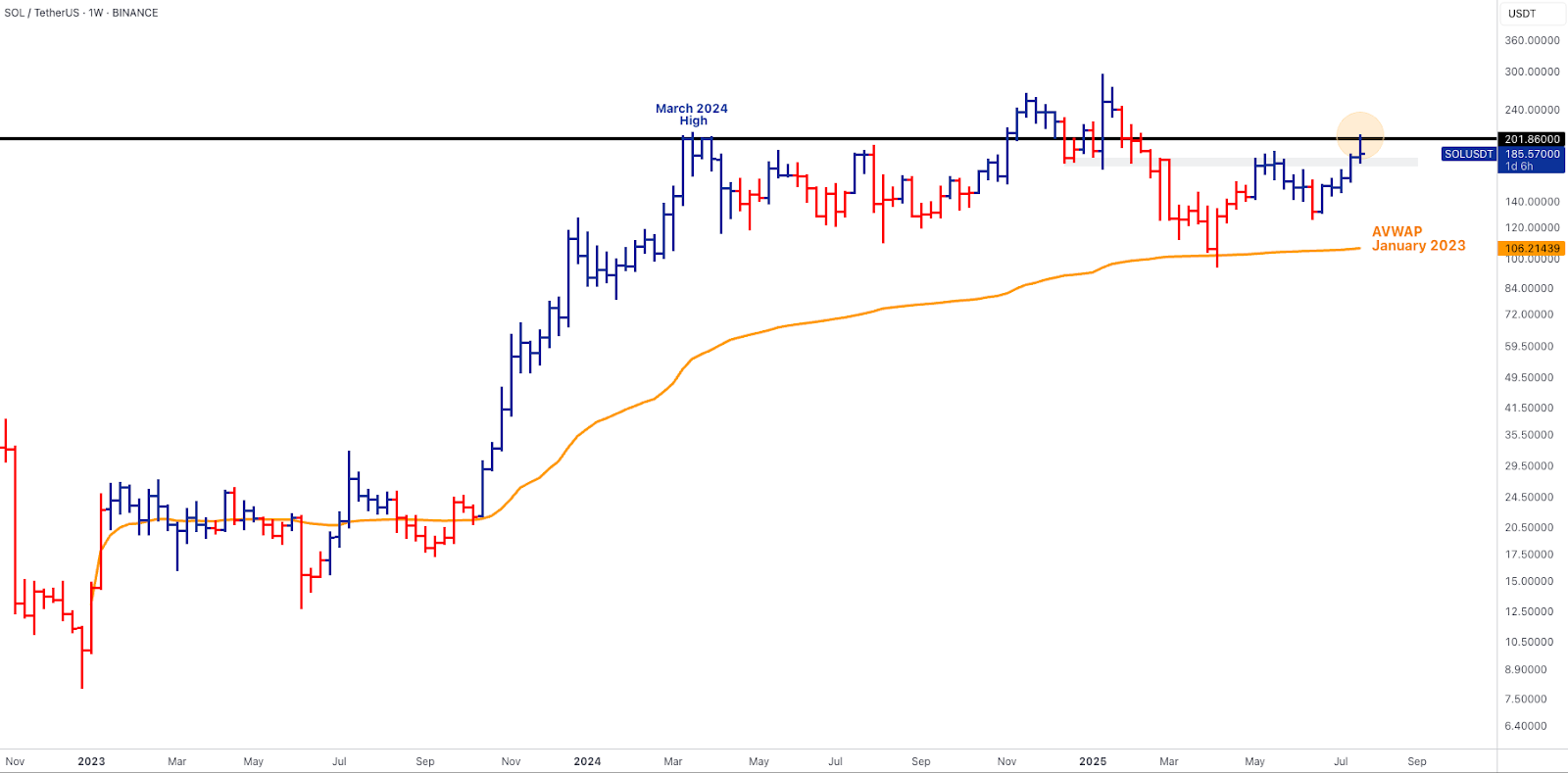

Solana Consolidates Above Breakout, Ecosystem Activity Anchors Flow

- Solana closed the week up ~3%, consolidating above its recent breakout from a continuation "cup‑and‑handle" formation.

- According to DeFiLlama, SOL’s TVL rose to ~$10.1B, reflecting a +3.4% 7-day increase. Daily DEX volume on-chain approached ~$2.94B, with weekly volume around ~$22.8B, and perpetual trading up ~11.2% over the same period, highlighting both spot and derivatives activity bulking up across the ecosystem.

- While average price action saw SOL climb from ~$186 to around ~$192 midweek before consolidating, the week’s technical structure remains constructive. The asset held the breakout level near $180, a zone that previously acted as peak resistance and now appears to be firming as support.

- Technically, a sustained recovery above $200–$202 remains key to unlocking targets toward the ~$250 range.

- What’s most notable is the diversification of flows underpinning this strength: GameFi applications like Access Protocol continued attracting attention, while memecoin volume (e.g. WIF, MEW) contributed to deepening ecosystem engagement.

- Meanwhile, Solana Mobile’s Chapter 2 reached ~143K pre-orders, reinforcing a growing consumer-layer stickiness beyond speculative dynamics.

- SOL’s strength last week is not hype, it is usage-driven. The chain’s ability to convert attention into throughput, from DeFi TVL to retail flows, underscores its evolving role as a blockchain offering tangible engagement rather than narrative inflation.

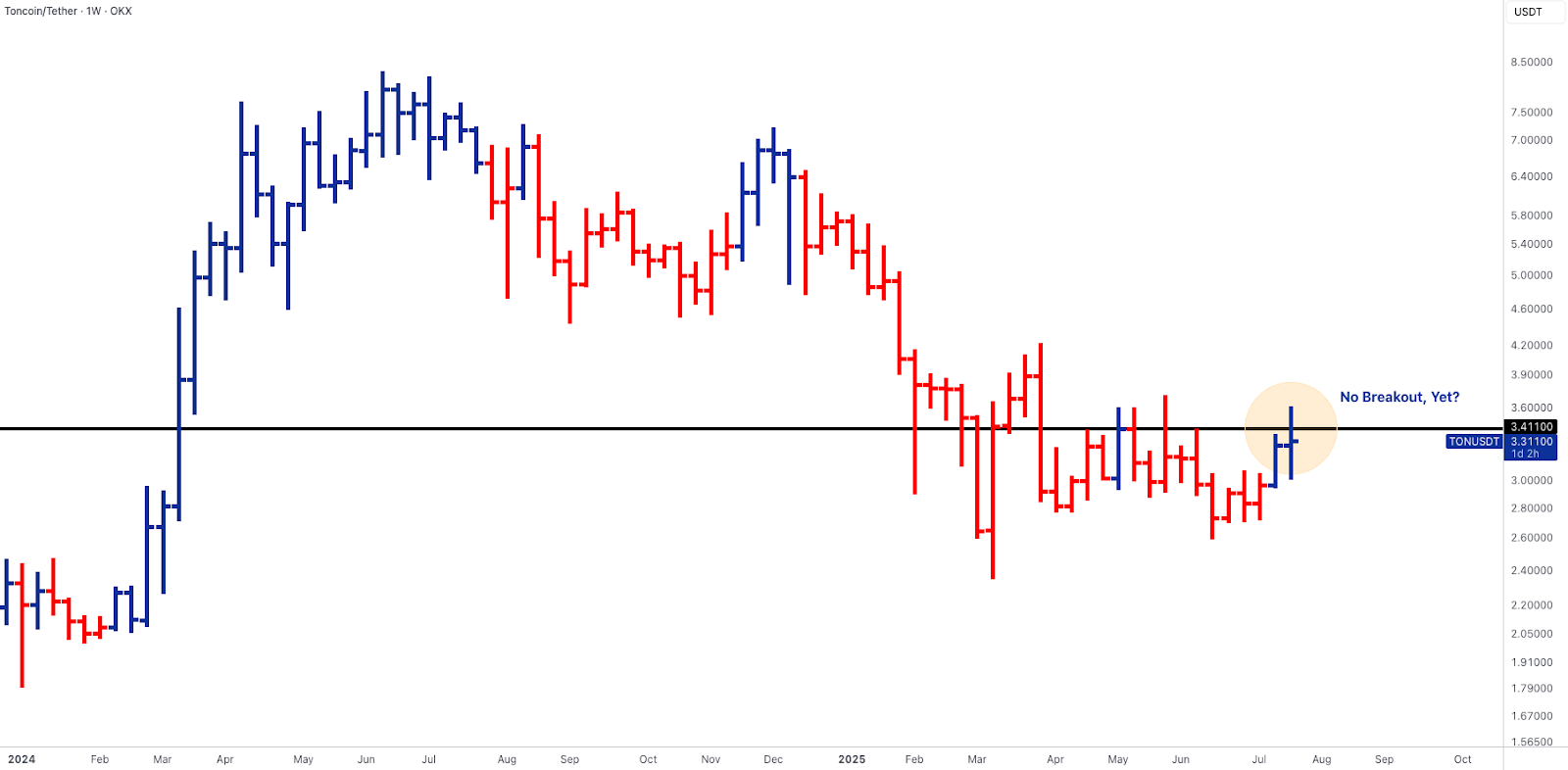

TON Eyes Breakout as Telegram Wallet Goes Live for U.S. Users

- TON gained ~1.1% on the week to close near $3.31, holding just below a key resistance zone around $3.41.

- The move followed Telegram’s official U.S. rollout of its self-custodial TON-based wallet, now available to ~87M American users directly within the app. This includes support for in-app token swaps, staking, and access to Telegram’s expanding Mini App ecosystem, lowering friction for mass-market crypto onboarding. Notably, this follows prior reports confirming over 100M TON wallets activated globally.

- Despite the structural significance, TON remains in a technical pause: it has yet to close above the critical $3.40–$3.60 zone on a weekly basis (see chart), though repeated retests suggest growing momentum.

- With the TON wallet now live in the largest consumer market globally, the chain is moving from speculative beta to platform-grade infra.

- Continued engagement data or on-chain activation could finally confirm a breakout, making TON one of the only tokens with a direct user acquisition engine embedded in a mainstream communication app.

RWA and Crypto Infrastructure Thesis Gathers Momentum

- This week, OSL raised $300M to expand tokenization and custody operations across Ethereum and Solana, tapping former BlackRock and JPMorgan executives to the board.

- This follows last week’s migration of BlackRock’s BUIDL fund to Chainlink CCIP, reinforcing the infrastructural case for RWA rails.

- On-chain, CCIP burn increased +6.2% WoW, though LINK underperformed with a ~4.6% weekly decline to ~$18.30.

- Elsewhere, MKR gained +12.9%, as DAI supply expanded ~2.6%, and Frax governance passed updates to support institutional lending via permissioned venues.

- The story across RWA and stablecoin infrastructure is shifting from narrative to capital deployment.

- Protocols building regulatory-compliant bridges between fiat, RWAs, and DeFi are now being funded and staffed at a Tier-1 level. While token prices have yet to reflect the full shift, the foundation is solidifying.

Outlook for the Week

- Developments on Trade Tariffs: Countries are scrambling to finalise trade deals ahead of August 1 deadline with headline focus on US-China set for Monday in Stockholm amid expectation of another 90-day extension.

- Action-packed week as Fed, BOJ monetary policy meetings await, both central banks are expected to put rates on hold.

- Monthly US employment report and earnings from megacap giants due this week including Apple, Microsoft and Amazon.

Oops! Something went wrong while submitting the form.