Aug 4, 2025

August Opens with Macro Uncertainty, but Institutional Support Builds

Summary:

This week confirms crypto’s ongoing maturation into an institutional‑grade asset class:

- A fresh round of macro jitters spooked the cryptomarket last Friday: Bleak July US jobs data, buoyant USD with DXY index rose over 100 on Friday after the latest round of sweeping U.S. tariffs.

- Risk assets, including crypto, started the week on a steadier ground as investors continue to assess US tariffs and jobs data, and pricing in a higher chance of more easing on the back of concerns of exacerbating inflation and economic slowdown.

- Mounting bets of 84.5% odds in a Fed rate cut next month according to CME watchtool.

- ETH absorbed validator exits while maintaining structural inflows and treasury demand.

- BTC weathered record ETF outflows as corporate treasuries defined the floor.

- SOL and TON illustrate utility‑driven resilience and adoption‑led rotation.

- Hong Kong anchors a regulatory and RWA hub, attracting capital beyond narrative flows.

- Capital now seeks structured, compliant, and flow‑supported opportunities, rewarding allocators who align with institutional demand regimes rather than short‑cycle speculation.

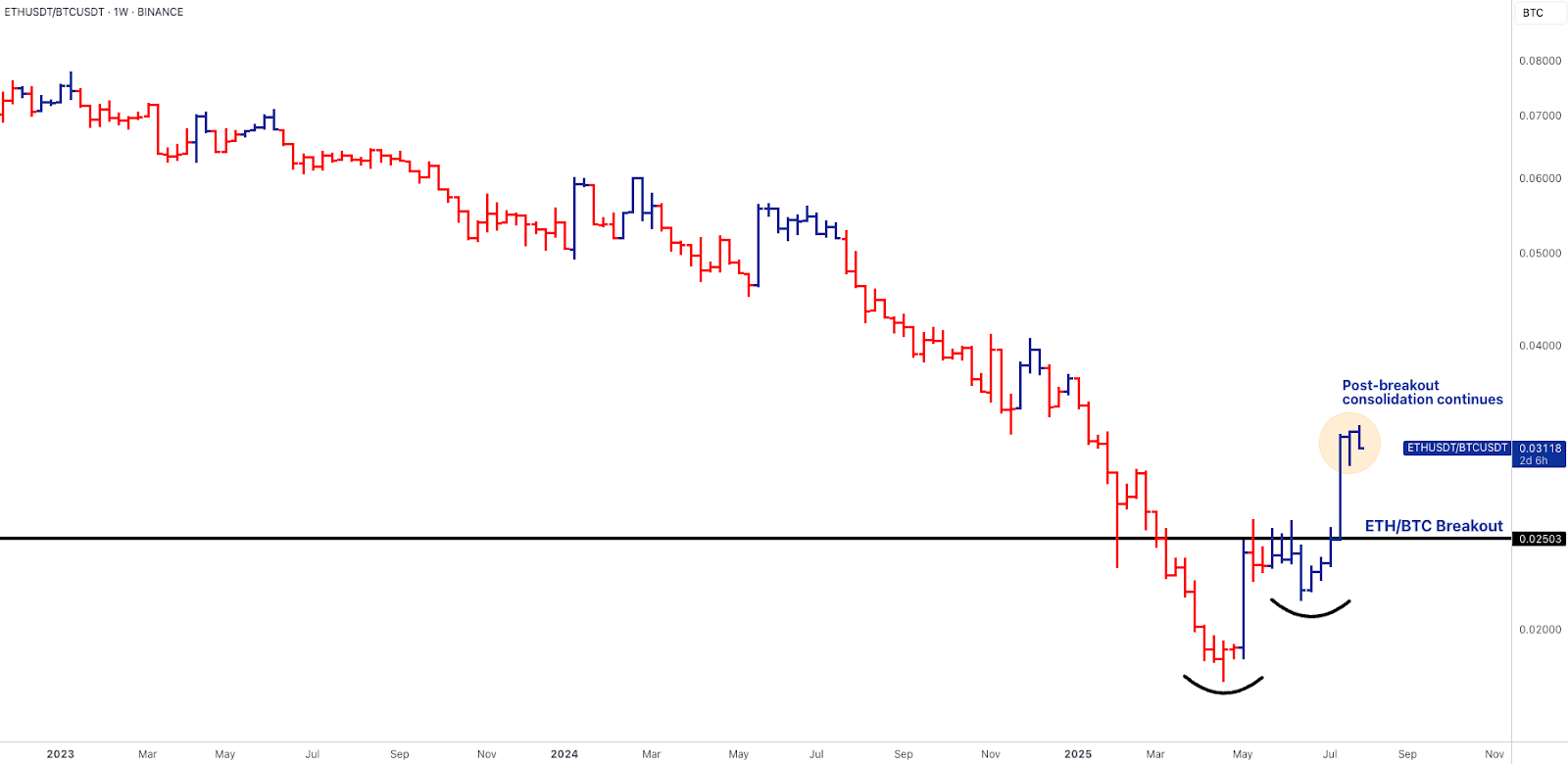

Ethereum Validator Exit Spike Meets ETF Rotation. Post‑Breakout ETH/BTC Consolidation

- Ethereum entered August with its largest validator exit queue on record, peaking July 26 at 744K validators (~$2.6B), with 559K ETH ($1.93B) still pending withdrawal as of August 3.

- Exit wait times stretched to 9-10 days as leveraged stETH/Aave positions unwound, led by 167K ETH (~$630M) in protocol‑level withdrawals.

- Yet, the entry queue of ~123.7k ETH (~$427M) underscores that institutional onboarding remains intact, supporting staking yield mechanics despite short‑term liquidity stress.

- Spot ETH ETFs snapped their 20‑day inflow streak with muted net flows of ~$154M and a single‑day outflow on August 1, reflecting profit‑taking rotation rather than a structural demand break.

- On-chain analytics shows a whale has been dip buying $300M worth of ETH over the past 3 days, evidence of on-going demand from high-conviction players.

- July still delivered ~$5.43B inflows, with total ETF holdings now 2.3M ETH (~2.5% of supply). Coupled with treasury wallet additions (~790K ETH), liquid supply on exchanges remains historically thin.

- Technically, ETH/BTC achieved a clean breakout above 0.025, now consolidating near 0.031 in a post‑breakout retest structure, reflecting capital rotation from BTC into ETH even as BTC absorbed ETF outflows.

- This structural ETH/BTC turn signals that institutional flows are seeking duration in ETH, aligning with ETF growth and validator participation. ETH is demonstrating mature, two‑sided market structure: leveraged exits coexist with ETF and treasury absorption, while the ETH/BTC breakout confirms a rotation bid that positions ETH as a core institutional hold in H2 2025.

Bitcoin Weathers Record ETF Outflows as Corporate Treasuries Anchor Market

- Bitcoin endured historic ETF redemptions this week: ~$643M net outflows, including a record $812M single‑day outflow on August 1 (led by Fidelity and ARK), ending a seven‑week net inflow streak.

- Price flushed to ~$113K intraday before stabilizing near $114K, holding the $113K–$119K range. July still closed at a record ~$115,800, confirming the higher‑timeframe uptrend.

- Corporate balance‑sheet accumulation is now the structural floor. Strategy Inc. lifted holdings to 628,791 BTC (~3% of supply), while Metaplanet advanced a $3.7B capital raise for BTC adoption. These strategic inflows absorb ETF volatility, reinforcing that long‑horizon treasuries, not short‑cycle ETF flows, now define price stability.

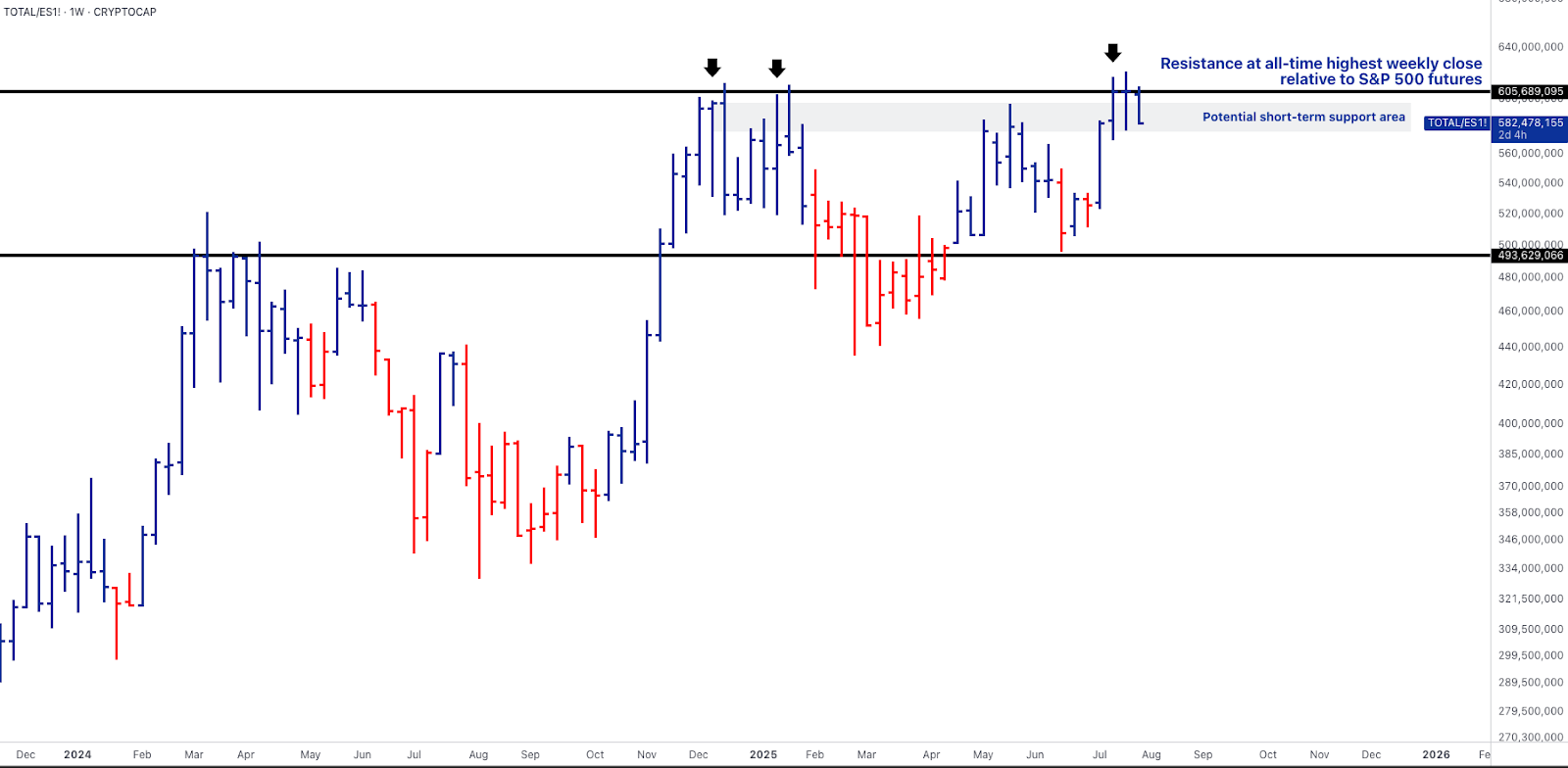

- The TOTAL/ES1 ratio illustrates this: despite record ETF redemptions and a ~$113K flush, crypto remains near ATHs relative to S&P 500 futures, signaling that macro risk appetite and institutional rotation remain intact.

- BTC’s capacity to absorb historic outflows without cascading liquidation cements its reserve‑asset role. Corporate treasuries are emerging as the market’s structural stabilizer, with asymmetric upside building as ETF flows normalize.

Solana Absorbs Leverage Unwind as Futures and On‑chain Demand Persist

- SOL retraced ~14% to ~$162 this week, but institutional participation is accelerating. CME SOL futures volume surged to $8.1B (+252%) with OI climbing 203% to $400M, showing tactical positioning for either ETF catalysts or structural adoption.

- On‑chain metrics remain robust: TVL hit ~$9.85B (+14% MoM), and July’s DEX + perp volume exceeded $82B, confirming persistent user engagement.

- The technical retrace still reflects absorption, not rejection, supported by developer momentum, mobile wallet traction, and DeFi‑native flows.

- Solana’s utility‑driven adoption curve is cushioning speculative drawdowns. Deepening futures liquidity while sticky on‑chain usage points to rotation resilience, setting up for potential renewed trend momentum as macro inflows return.

- A weekly break below ~150 could negate this in the shorter-term.

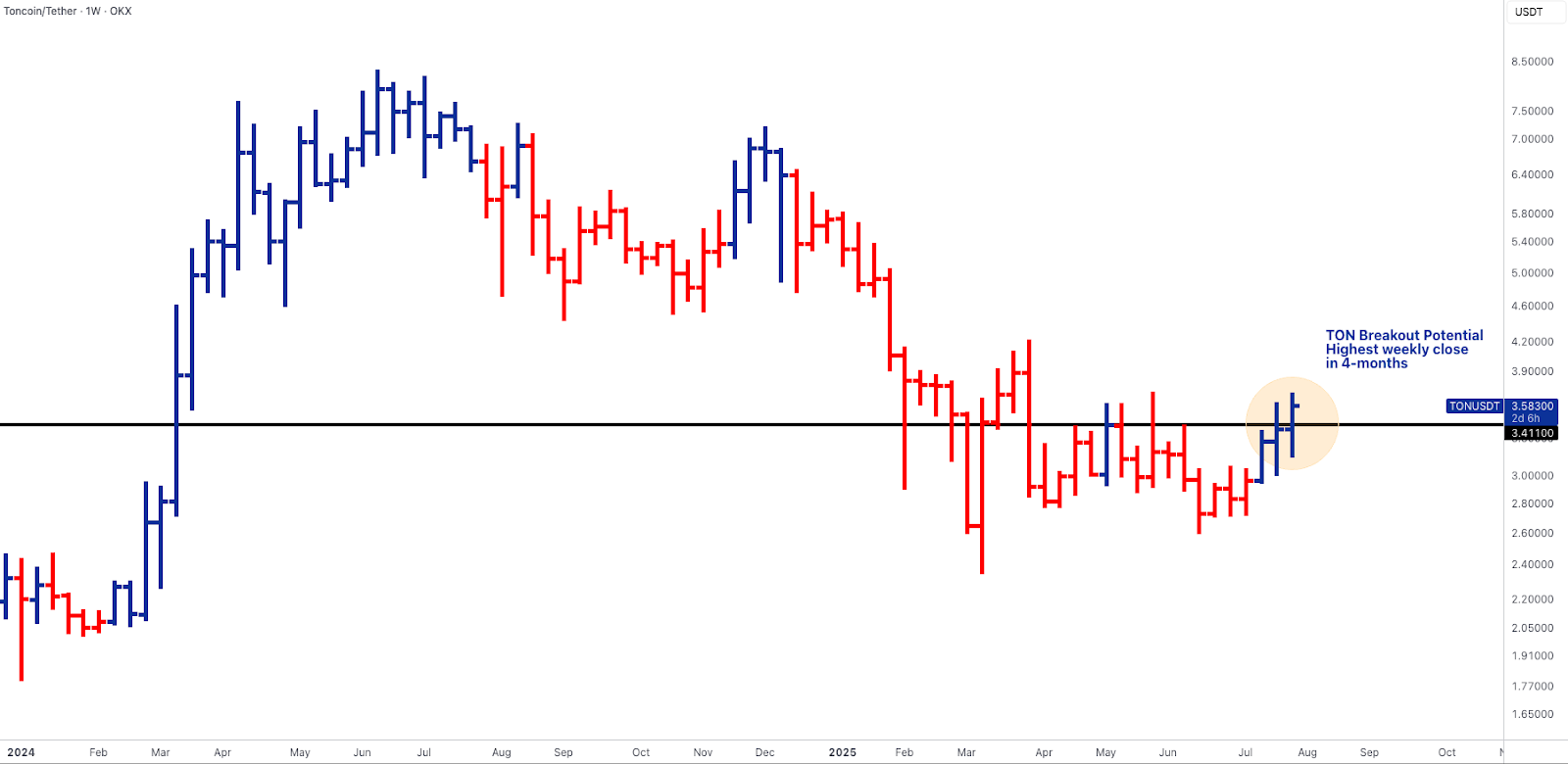

Toncoin Eyes Breakout as Telegram Ecosystem Demand Drives 4‑Month High

- TON is poised for its highest weekly close in four months, trading at ~$3.58 after reclaiming the ~$3.4 structural level.

- The move is backed by a resurgence in Telegram ecosystem adoption, with TON‑based wallets surpassing 11M active users and mini‑app integrations expanding in Q3.

- Daily active wallet growth hit ~8.2% WoW, signaling a sustainable network bid rather than speculative rotation.

- On‑chain flows show exchange balances dropping to 62M TON (~12% of supply), a 10‑month low, while staking participation exceeds 59%, creating structural float compression.

- Venture unlocks remain light through August, further supporting the breakout potential.

- The TON/USDT weekly chart reflects a textbook range reclaim and potential breakout setup, aligning with the macro rotation into high‑utility Layer‑1s amid ETH and BTC consolidation.

- TON is quietly transitioning into a structural L1 rotation leader, supported by Telegram network effects and sustained staking participation.

- A weekly close above ~$3.70 would confirm a breakout trajectory toward the $4.20-$4.80 range, with limited immediate supply headwinds.

Hong Kong Solidifies Asia’s Institutional Crypto Hub with Stablecoin & RWA Framework

- Hong Kong’s Stablecoin Ordinance (Cap. 656) officially went live on August 1, delivering Asia’s first fully-licensed framework for fiat‑backed stablecoins.

- The regime enforces 1:1 reserves, segregated custody, daily attestation, and quarterly audits, with the HKMA targeting fewer than 10 issuers by 2026.

- The scarcity of licenses itself establishes an early‑mover moat, positioning licensed issuers as critical on‑ramps for regional capital flows.

- Simultaneously, the RWA Registration Platform launches August 7, inviting tokenized treasuries, commodities, and private credit instruments under explicit regulatory approval.

- This move cements Hong Kong’s ambition to become the primary Asian hub for tokenized capital markets, bridging TradFi liquidity into on‑chain structures.

- July saw $1.5B raised across tokenization‑focused firms, while Ondo Finance (ONDO) and Chainlink (LINK) attracted renewed inflows as investors positioned for regulated yield‑bearing tokenized assets.

- LINK’s CCIP and Proof‑of‑Reserve integrations are emerging as core infrastructure for RWA settlement and stablecoin auditability, further anchoring the narrative.

- Hong Kong is building the digital capital corridor of Asia, where regulated stablecoins are the entry point and RWAs are the destination for institutional yield rotation.

- Ondo, Chainlink, and early licensed issuers stand to benefit as compliant liquidity migrates into tokenized Treasuries and private credit on‑chain.

Outlook for the Week

- Risk assets, including crypto, took a hit last Friday after a fresh bout of macro jitters: Bleak July US jobs data, buoyant USD with DXY index rose over 100 on Friday after US latest round of sweeping tariffs.

- Risk assets, including crypto, started the week on a steadier ground as investors continue to assess US tariffs and jobs data, and pricing in a higher chance of more easing on the back of concerns of exacerbating inflation and economic slowdown.

- With trade tensions back on the table, investors are going to keep a close eye on US-China trade talks ahead of a key review on 12 August in which tariff pause will expire.

- Focus will be on key PMIs (July Global Services PMI & ISM Non-manufacting PMI), initial jobless claim and another round of US earnings due this week.

- ~⅔ of S&P 500 companies have reported and 63% have beaten forecast.

- Several Fed officials are due to speak this week as well, and investors will be looking for clues on easing indications at this coming FOMC meeting in September.

Oops! Something went wrong while submitting the form.