Sep 8, 2025

Divergent-flow digestion ✅ Deleveraging ❌

Summary:

- A divergent-flow digestion week rather than a deleveraging: BTC coiled between ~109-113.5k reclaim band after the late-August wick to ~107k, while ETH held a ~$4.25k weekly low and worked the prior resistance shelf as potential demand.

- ETF tapes diverged, as BTC funds net-inflowed while ETH funds net-outflowed.

- Yet, dollar rails and on-chain supply tightened: ~$2B fresh USDT on Ethereum expanded executable fiat, and a dormant ICO wallet staked 150k ETH ($600-650M), shrinking tradable float.

- Breadth paused rather than reversed: BTC.D stayed inside last week’s range and below the ~60.5–61% resistance.

- With liquidity refilled, the market is offering rule-based levels: ETH must convert the prior resistance shelf into support via absorption; BTC must accept back above ~111.5-113k to re-open range highs.

- US Inflation data is on the radar after last Friday’s dismal jobs data. This will give us a better indication of the degree and pace of the Fed’s rate cut.

- Markets are pricing in a 100% chance of a September FOMC rate cut, according to CME Watchtool, with a 90% chance of a 25bps cut.

1) BTC - ETFs net-buy; shelf defended; resistance unchanged at ~113.5-114k

- BTC set a contained weekly range just under resistance, with daily lows testing the 108-109k band, i.e., holding above the 104-105k support level while attempting to reclaim the ~113.5-114k without success.

- Spot ETF prints skewed positive overall (strong mid-week inflows, modest Thu/Fri give-back), consistent with derivatives-led de-risking rather than spot abandonment; basis/funding dipped into the mid-week wobble and normalised into the weekend.

- The relative lens is unchanged week-over-week: BTC dominance did not print fresh lows and did not regain resistance either; it traded inside last week’s range and still sits below ~60.5–61%.

- Breadth remained in pause mode rather than reversing, as alts retain the benefit of the doubt unless BTC.D regains momentum above resistance.

- Near-term guardrails remain crisp: weekly acceptance back above ~111.5–113k re-opens range highs; failure to do so keeps ~102–104k as the first magnet while the broader $95–105k structural shelf anchors the downside.

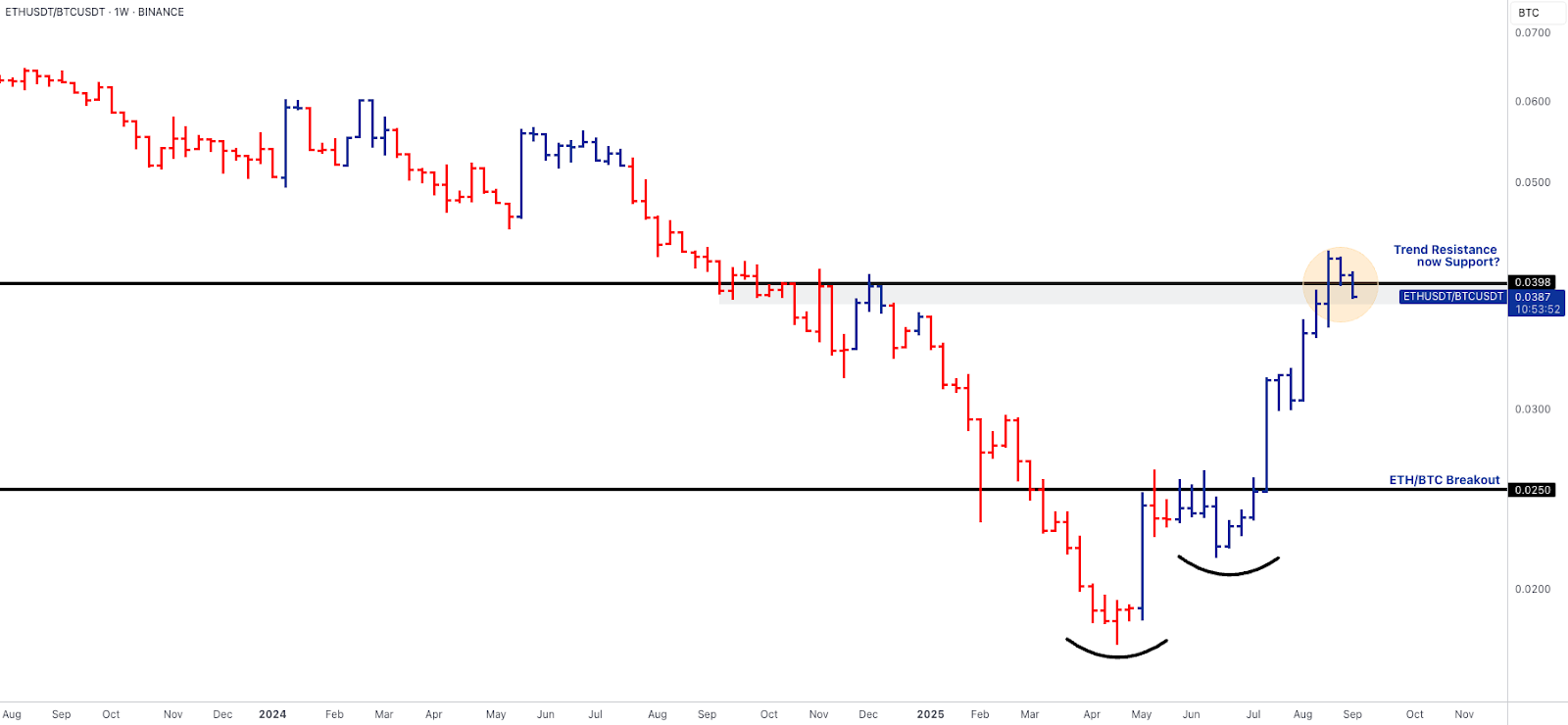

2) ETH - flows soft, supply tight; ETH/BTC retests support

- U.S. spot ETH ETFs printed a clear weekly net outflow (~$0.8B), with consecutive daily outflows throughout the trading week (Tuesday to Friday), explaining late-week relative softness.

- That was not accompanied by structural stress: funding and short-tenor basis compressed into the mid-week wobble and normalised by the weekend; exchange inventories did not show a disorderly jump.

- In parallel, a dormant ICO address moved ~150k ETH into staking, mechanically reducing liquid float.

- Price structure is consistent with digestion: ETH held ~$4.25k and never lost $4k.

- Technically, ETH is working inside the 2021 weekly-close band beneath ~4.63k; the task is absorption, meaning acceptance above that band turns prior supply into support.

- On relative terms, 0.038-0.040 for ETH/BTC remains the decision shelf: hold above ~0.040 and the rotation can extend toward 0.043-0.046; lose ~0.038 and the move likely back-fills toward ~0.034-0.035, which would be a reset, not a thesis break on ETH relative strength, provided ETH keeps absorbing supply around its current levels.

3) SOL - compression at resistance; “prove-it” breakout still in play

- SOL spent the week inside last week’s range, failing to print a higher high and once again stalling at the March-2024 high (~$203-206).

- That band has been a stubborn supply shelf: every probe is being sold, yet higher weekly lows along the rising trendline kept compressing price into a tighter wedge.

- The setup remains binary but clean: weekly acceptance above $206-210 would finally clear the overhang and unlock a measured $250-260 objective, while a close back below $188-190 would invalidate the immediate breakout and risk a back-fill toward $172-176 before buyers can reload.

- For confirmation, watch perps OI continuity without a funding blow-out, spot-lead moves (basis not doing the lifting), and stable LST spreads (e.g., JitoSOL vs native staking) as signs real demand is absorbing the shelf.

- The repeated failures to make a new high highlight the resistance, but with each test, seller inventory is likely thinning; the next decisive weekly close should resolve the coil.

4) Flow-Bearing Catalysts (Treasury, Migration, Incentives, Buybacks)

CRO (Cronos) -

- Treasury-driven demand, scheduled, not sentimental.

- JV terms formalise a ~$105M CRO purchase, creating a mechanical bid and equity cross-exposure.

- CRO needs to hold the ~$0.2035 breakout level as it trades just below the catalyst anchored-VWAP for continuation.

- On-chain treasury accumulation will need to step higher week-over-week, with net exchange outflows and steady positive taker flow. If funding stays contained, the breakout would remain flow-validated, not just headline-driven.

POL (Polygon POL) —

- Mechanics over beta are at play, as migration is largely complete and staking/gas economics are aligned, implying infrastructure accrual now maps cleanly to POL.

- The market is holding above ~$0.255 after a base breakout; that keeps $0.32-0.34 in play (stretch ~$0.37-0.38).

- The move would likely invalidate on a weekly close back below ~$0.255.

- Net staking growth, validator participation and bridge inflows > outflows would need to be monitored.

ARB (Arbitrum) -

- Usage-funded lift as DRIP Season-1 incentives are live; the trade is continuity, not first print. Price is chewing just above the reclaimed $0.45-0.4925 shelf.

- Durability requires sequencer revenue/fees and borrow demand to print while funding remains constructive. Lose the shelf, and it implies structural demand remains absent.

PUMP (Pump.fun) -

- Platform revenue feeding buybacks implies float compression.

- Price accepted above ~$0.0040, establishing a new support area.

- The thesis remains that programmatic buybacks should absorb supply as it reduces overall.

- The token remains volatile, but a clear breakout/support area has been established.

5) Dollar & credit rails added to macro glue - why flows can re-accelerate quickly

- The pipes refilled. On Sep 4, on-chain trackers flagged ~$2B USDT minted on Ethereum, expanding exchange and AMM working capital, which historically has tightened spreads and deepened order books on bounce days.

- That sits alongside steady institutionalisation (banks/payment hubs deepening USDC routes), creating a cleaner conduit for marginal dollars to land in size once risk re-engages.

- Macro-wise, Friday’s soft U.S. payrolls added a modest growth wobble even as yields softened; that combination explains ETF defensiveness into the weekend without breaking the broader risk bid.

- Fresh stablecoin inventory, a manageable macro environment accompanied by Fed cuts, could deliver a market that can re-risk quickly once we reach Q4 and bypass potential seasonal headwinds.

6) Outlook for the Week

- After the dismal US jobs data last week, US inflation data (PPI and CPI) are under the spotlight today.

- The disappointing US Non-farm payroll data last Friday, which came in ⅓ short of expectations, pretty much sealed the deal of a September Fed rate cut.

- Markets are now expecting a 100% chance of a Fed rate cut this month, with a 90% chance being a 25bps cut.

- Which makes the US inflation data important as it will give us an indication of the level of rate cut with the Fed having to balance the 2 main mandates: low inflation and high employment.

- Gold jumped to a record high while US Treasury Yields closed to a 5-month low.

- US tariffs are back haunting us again as Trump threatens trade retaliation against the EU over 'unfair' Google fine. US Treasury Secretary Bessent also warns that the Supreme Court rules against Trump’s tariffs might mean the US will need to “refund half the tariffs”, which would hit the US treasury.

Oops! Something went wrong while submitting the form.