Bitcoin Decouples From Risk Rally as ETF Drain Hits $6.35B

Blueprint - BTC decoupled from risk-on; ETF drain is the regime, not macro fear

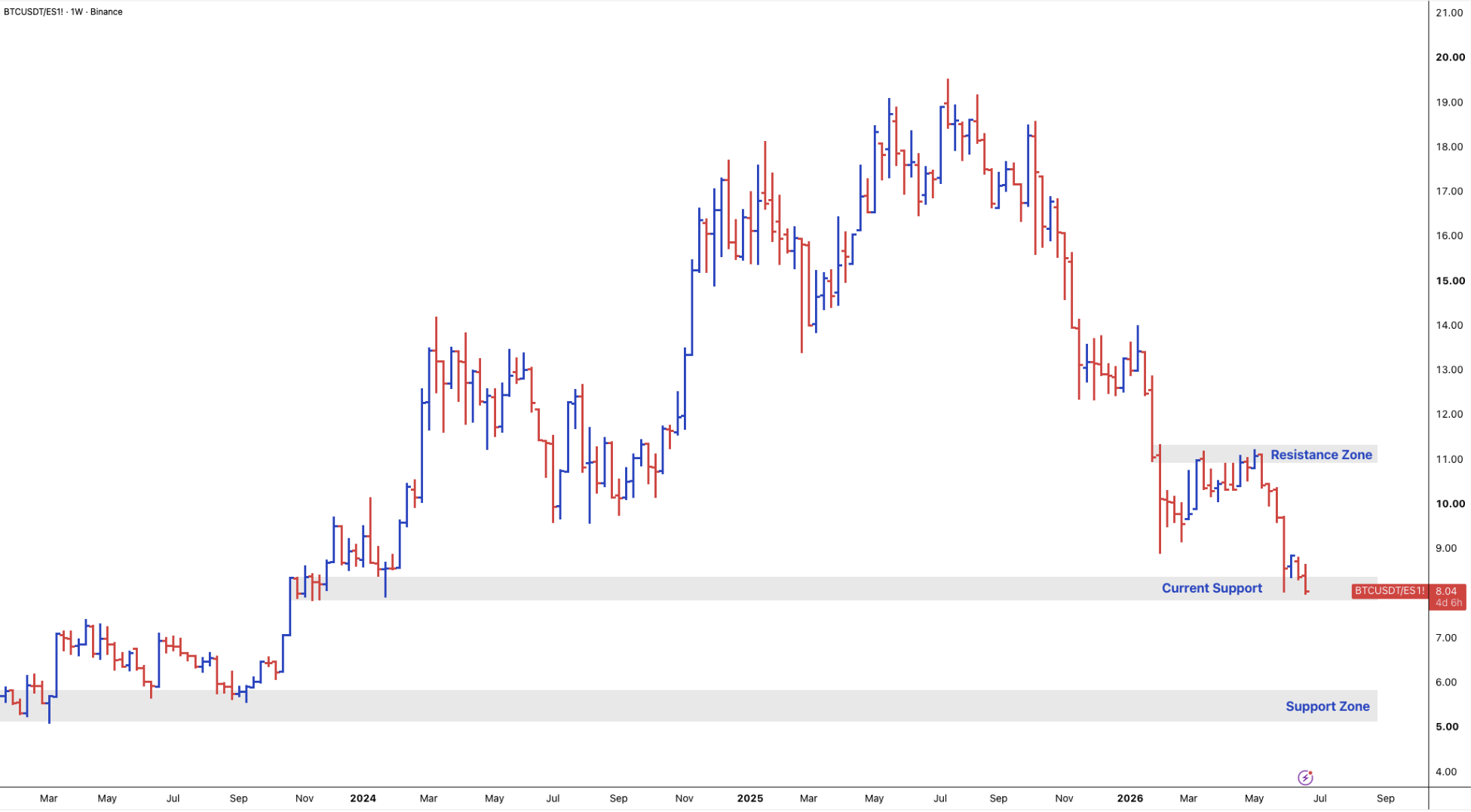

- BTC ended the week at ~$64,185, a -0.25% move while the S&P 500 gained +2.92%. The BTC/ES ratio (BTC price divided by ES1! futures at ~7,570) sits at approximately 8.48 — below the 9.0 reference floor that has historically marked the level at which BTC reprices relative to equities. The ETF overhang remains the dominant force suppressing price even in a constructive macro week.

- U.S. spot Bitcoin ETF net outflows totalled approximately $6.35B over the past 30 days. The 13-consecutive-day outflow streak from May 15–June 3 (~$4.4B total) stabilised briefly after June 5, but June 1–18 cumulative flows remained approximately -$2.27B, with June 18 alone running about -$90.7M. This is deliberate institutional repositioning, not panic — bond yields and rate hike expectations are making non-yielding BTC less attractive relative to duration assets.

- The Federal Reserve held rates at 3.5–3.75% at the June 16–17 FOMC — Kevin Warsh's first meeting as Chair. His press conference was unambiguously hawkish: the committee is "unanimous and unambiguous" on price stability, the dot plot shows a median year-end rate of 3.8% (implying one additional 25bps hike), and nine of seventeen members project at least one hike. Markets now price a 49% probability of a September hike, up from 27% the day prior.

- May CPI printed +4.2% YoY (+0.5% MoM, released June 10) and May PPI at +6.5% YoY (+1.1% MoM, released June 11) — the latter the highest annual PPI reading since late 2022. Both significantly exceed the Fed's 2% target. The constructive development this week: a confirmed Israel-Hezbollah ceasefire cut WTI approximately 8% to ~$77.50/bbl. If sustained, energy's contribution to CPI softens meaningfully going into the July 14 print.

Our take: Crypto is in a regime of ETF-driven isolation — not a market that fears macro risk (the VIX collapsed, equities rallied, gold fell -4.13% on risk-on rotation), but one where a structurally impaired bid has created its own gravitational pull. The $6.35B in 30-day BTC ETF outflows is not panic selling; it is deliberate reallocation by investors who entered at higher prices and who now find rate-sensitive instruments more attractive as the Fed pivots toward hikes. The regime started with macro (sticky inflation + strong jobs data reducing cut expectations) but is now self-reinforcing through ETF mechanics.

The key tension is the ceasefire. Energy was the primary driver of both CPI and PPI in May — a sustained oil pullback from $85+ to $77 could swing the June CPI print by 30–50bps. But Kevin Warsh is the new Chair, and his framing of inflation as supply-shock driven (not demand-led) suggests the committee will be slow to revise down its hawkish posture based on a single geopolitical data point. The market should treat the energy tailwind as conditional. What resolves this regime is one of two things: (a) a June CPI print below 3.8% on July 14 that forces the dots to flip back to neutral, or (b) ETF outflows reversing into sustained weekly inflows — which likely requires the BTC/ES ratio to re-establish above 9.0 as a signal of genuine repricing.

BTC - Flat Amid the Risk Rally; ETF Drain Still Running

- BTC ended June 22 near $64,020, down approximately 0.25% on the week — a stark contrast to the S&P 500's +2.92% move. The BTC/ES ratio sat at ~8.48 (BTC $64,020 / ES1! ~$7,541), below the 9.0 reference floor. When BTC cannot outperform equities in a strong risk-on week, it signals ETF-specific selling pressure that masks any underlying demand recovery.

- The Fear & Greed Index reading of 23 (Extreme Fear) reflects the cumulative impact of the ETF bleed. Investors who entered at cycle highs above $100K are sitting on significant unrealised losses, and the absence of new institutional inflows has removed the marginal buyer that previously set price. Bitcoin Dominance closing in on 59.02%, and market cap is approximately $1.29T with 24H trading volume of $16.07B — subdued relative to prior cycle activity.

- BlackRock launched BITA (iShares Premium Income Bitcoin ETF) on Nasdaq on June 16 — an options-overlay product targeting 15–25% annualised yield from BTC exposure via covered call strategies. This is product innovation at the institutional layer, but it is not a spot demand catalyst. Covered call structures cap upside participation and compete for capital with pure spot exposure in IBIT. Net effect on BTC spot price is ambiguous near-term.

- BTC is -16.98% over one month, -25.06% YTD, and approximately -49% below its all-time high of $126,230. The weekly -0.25% stabilisation represents seller exhaustion more than a demand-driven base.

Our take: BTC's failure to participate in the equity rally is the clearest confirmation of the current regime. In prior cycles, a VIX collapse and SPX +3% would have been fuel for a significant BTC move — instead, the ETF complex is acting as a structural counterweight. The critical level to watch on the upside is $65,800 (current consolidation ceiling) and on the downside $61,500 (prior swing low). A break above $65,800 on sustained positive ETF flows would signal the isolation thesis is breaking down; a break below $61,500 confirms drift toward the mid-$50s. AVWAP levels once continues to loom overhead as vital levels to reclaim, with August 2024 AVWAP sitting at $86,875.61, and BTC Anchored at All Time High at $82,231.18

ETH - Quiet Outperformance; ETH/BTC Lifts Off a Multi-Year Low

- ETH closed the week at approximately $1,744, up +1.53% — outperforming BTC (-0.25%) and the broader alt market (TOTAL3 -1.93%). The ETH/BTC ratio rose +2.86% on the week to approximately 0.0272. While this is a meaningful weekly recovery, the ratio remains deeply negative YTD (-20.35%) and is emerging from what analysts describe as "the final support" zone near 0.016.

- ETH found support at the $1,670–$1,690 zone intraweek and is approaching the $1,725–$1,750 resistance band. A sustained close above $1,750 would shift the technical narrative from "base formation" to "potential trend reversal." Analysts monitoring the pattern note a possible 9-month descending channel upper boundary retest is currently underway.

- On-chain activity remains steady but unremarkable: gas fees have not spiked, indicating neither a memecoin nor a DeFi demand surge is driving activity. Layer-2 volumes — particularly Base, where Aerodrome Finance drove strong activity this week — are absorbing activity that would previously have generated ETH mainnet demand.

- ETH ETF flows remain marginally negative, consistent with the broader outflow environment, though lighter selling pressure relative to BTC allowed the ETH/BTC ratio to recover.

Our take: ETH's relative outperformance is technically meaningful but contextually fragile. A single week's +2.86% ETH/BTC move does not constitute a trend reversal after a -20% YTD drawdown. The real test is a clean break above $1,750 on volume — that would shift the narrative from "bottoming" to "rotating." The Layer-2 cannibalisation dynamic continues: liquidity is finding home in application-layer ecosystems (Base/Solana) rather than ETH mainnet, reinforcing why ETH needs a distinct institutional catalyst — staking yield regulation, EIP-driven burn acceleration, or a DeFi volume supercycle — to rebuild relative value.

SOL & BNB - Solana Surges +7.4%; BNB Stalls Near Monthly Lows

- SOL/USDT rose +7.41% on the week to $74.21, significantly outperforming both majors and the broader alt market. Price broke above the $71.35–$72.20 support zone and now faces resistance near $76.00. Technical ratings show a daily buy signal but sell signals on 1-week and 1-month timeframes — characteristic of a bounce within a longer downtrend.

- SOL's outperformance reflects a confluence of positive signals: Aerodrome Finance (Base/Solana-adjacent DeFi) driving DEX activity; the Solana memecoin ecosystem maintaining relative health; and institutional narrative support for Solana as the preferred "retail activity" L1. However, the mid-July Pump.fun (PUMP) token cliff unlock is a supply event to monitor — if the memecoin ecosystem is healthy it is absorbed; if not, it weighs on SOL sentiment.

- BNB/USDT fell -3.55% to $594.11, underperforming significantly. BNB has declined -10.71% over the past month and sits near support at $563–$566. Reduced Binance exchange volume and absence of a BNB-specific product catalyst explain the divergence.

- The SOL/BNB spread this week is approximately -11% in favour of SOL. This reflects a structural theme: market preference is shifting from centralised-exchange utility tokens (BNB) toward permissionless L1s with active developer ecosystems (SOL). This theme likely extends into Q3.

Our take: SOL's +7.41% is the brightest standalone signal in an otherwise tepid alt week. But context matters: TOTAL3 fell -1.93% simultaneously — SOL's gains arrived without support from the broader alt complex. Narrative-driven moves without cross-market liquidity follow-through tend to retrace once the catalyst fades. The Pump.fun unlock in mid-July is the key near-term risk; watch cumulative Solana DEX volumes as a leading indicator of whether the ecosystem demand that drove this week's move is structural or event-driven.

Alpha Cluster - AI Infrastructure and DeFi Governance Lead the Alpha Week

- Bittensor (TAO) was the largest material-cap gainer this week, up +28.3%. The move is driven by renewed institutional interest in decentralised AI infrastructure: TAO functions as a market for AI compute staking rewards, and the AI agent narrative entering a new phase (multiple competing frameworks bidding for distributed compute) is the direct catalyst. TAO is now the primary liquid crypto proxy for the "distributed AI infrastructure" thesis.

- Uniswap (UNI) gained +18.68% on renewed optimism around the protocol's fee-switch governance proposal — which, if implemented, would distribute protocol revenues directly to UNI stakers. This converts UNI from a governance token with no direct cash flow into a yield-bearing asset with an underlying revenue model. Watch for a formal governance proposal timeline in the next 2–4 weeks; the vote outcome is the binary catalyst.

- Additional top weekly gainers: Zcash (ZEC) +21.3%, WhiteBIT Coin (WBT) +20.2%, XLM (Stellar) +14.22%, Hyperliquid (HYPE) +13.00%, AAVE +12.81%. ZEC's move likely reflects privacy-coin rotation as GENIUS Act and MiCA push institutions toward transparent stablecoins — paradoxically increasing interest in privacy-preserving alternatives for specific use cases.

- The GENIUS Act stablecoin legislation carries a 73% Polymarket probability of enactment by 2026, with a July 2026 deadline for federal/state regulators to promulgate final rules. This creates a bifurcated market: compliant USD stablecoins (USDC, regulated USDT) benefit from legitimisation; non-compliant alternatives face existential regulatory pressure.

Our take: This week's alpha landscape separates into two categories: AI-adjacent tokens capitalising on a macro narrative (TAO) and DeFi protocols with defined near-term value-accretion catalysts (UNI fee-switch, AAVE governance activity). TAO's move is interesting because it prices distributed compute networks as having real option value independent of general crypto beta — the challenge is that its tokenomics depend on continued subnet development attracting real economic activity. UNI's move is more directly investable: a governance vote with a clear timeline and a quantifiable value change. If the fee-switch passes, UNI's market cap relative to Uniswap's annualised protocol fee generation becomes the valuation anchor — something institutional investors can model.

Rails, Regulation & Institutionalisation - BlackRock's Yield-BTC Launch; MiCA Hard Deadline in 9 Days

- BlackRock launched BITA (iShares Premium Income Bitcoin ETF) on Nasdaq on June 16, 2026. The product uses an options overlay on BTC exposure to target a 15–25% annualised yield via covered call strategies. This is the first major institutional BTC income product and represents a meaningful expansion of the product landscape beyond pure spot exposure — potentially broadening the pool of yield-mandate investors who can access BTC.

- The EU MiCA transition period ends July 1, 2026 — nine days from today. After that date, entities without a CASP (Crypto Asset Service Provider) license face an effective ban on serving EU customers. This creates both a compliance urgency (entities scrambling to complete licensing) and a structural market access bifurcation (licensed entities gain a durable competitive advantage).

- Hong Kong's SFC is preparing a new public consultation on extending its regulatory regime to crypto financial advisors and asset managers. Combined with the Stablecoin Ordinance (enacted August 2025) and the first batch of stablecoin licenses expected imminently, HK is systematically constructing the most comprehensive regulated crypto hub framework in Asia.

- The GENIUS Act in the US has a July 2026 deadline for federal and state regulators to promulgate final stablecoin regulations. Requirements include licensed issuers, full reserve backing, and criteria for foreign stablecoin issuers to serve US customers. This effectively ends the era of offshore unregulated stablecoins accessing the US market.

Our take: The regulatory picture is entering its most consequential period of the current cycle. MiCA's July 1 deadline is not soft — it is a hard wall. Some of the selling pressure currently observed in the European institutional ETF complex may relate to clients reducing crypto footprint ahead of compliance deadlines as entities without CASP licensing become ineligible to hold or transact on behalf of EU clients. This is a transition-period effect that should resolve as licensing completes, but the near-term friction is real.

BlackRock's BITA launch is a longer-term positive for institutional adoption breadth. Income-oriented allocators (pension funds, insurance mandates) who cannot justify non-yielding asset allocations may access BTC through BITA where IBIT was inaccessible. But the covered call structure caps upside — BITA investors sacrifice BTC convexity for income. Near-term, BITA competes with IBIT for the same institutional wallet, and the options overlay's premium writing creates derivative selling pressure on BTC. Net directional effect is marginal but worth monitoring in ETF flow data.

Outlook - Rate Hike Odds Hit 49%; June CPI on July 14 Is the Binary

- The next FOMC meeting is July 28–29, 2026. Markets now price a 49% probability of a 25bps hike at that meeting, up from 27% before the June 17 decision. Fed Chair Kevin Warsh's language was unambiguously hawkish: "price stability" was cited 12 times in his press conference, and the dot plot shows nine of seventeen members projecting at least one hike in 2026, with a median year-end rate of 3.8%.

- The June CPI report (July 14) and June PPI (July 15) will set the July FOMC tone. A June CPI print below May's 4.2% — particularly below 3.8% — should reset September hike probabilities lower and provide a relief catalyst for risk assets including crypto. A flat or higher print likely makes a September hike near-certain, keeping DXY elevated and the crypto bid suppressed.

- The Israel-Hezbollah ceasefire announced on June 20 cut WTI approximately 8% on the week to ~$77.50/bbl. Energy was the primary driver of May's CPI and PPI shock (energy prices +3.9% MoM in May CPI). If WTI holds near $75–80 through late June, energy's contribution to June CPI should be materially lower than May's, creating a credible path to a CPI print that softens hike expectations.

- US 10-year Treasury yield sits at 4.49%, up ~5bps on the week. DXY is at 101.0 (+1.09% WoW) despite the risk-on equity move — which reflects the dollar's haven status reasserting alongside hawkish Fed signals. Gold fell -4.13% WoW to $4,190 as risk-on rotation and the ceasefire removed the geopolitical premium that had supported gold above $4,300.

- Upcoming macro calendar: June CPI July 14 | June PPI July 15 | FOMC July 28–29 | Token unlocks: PUMP (mid-July), WLD (July), XPL (July) | MiCA deadline July 1 | GENIUS Act final rules July 2026.

Our take: The macro regime is on a knife-edge. The disinflationary forces building — oil down, ceasefire holding, base effects turning more favourable in June — set up a potentially constructive CPI scenario. But Kevin Warsh's priority is price credibility above all, and a Fed willing to hike at 3.75% while CPI is at 4.2% sends a categorically different signal than a Fed waiting patiently for data. The dot plot's 3.8% median means the market has no choice but to price an elevated probability of a September hike until the data definitively contradicts it.

For crypto allocators, the playbook into July FOMC is: defensive core positioning in BTC (avoid leverage, respect $61,500 support), selective exposure in tokens with independent catalysts (UNI fee-switch vote, TAO AI infrastructure narrative), and close daily monitoring of BTC ETF flow data as the leading indicator. The tactical window is the 10 days between June CPI (July 14) and FOMC (July 28–29): if CPI prints below expectations, a sharp crypto relief rally is plausible in that window. The regime change signal is two or more consecutive weeks of net BTC ETF inflows combined with BTC/ES re-establishing above 9.0.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets