BTC Bounces in Isolation. Stagflation Hardens, ETF Bleed Finds Its Floor

Blueprint - BTC bounces in isolation, breadth absent

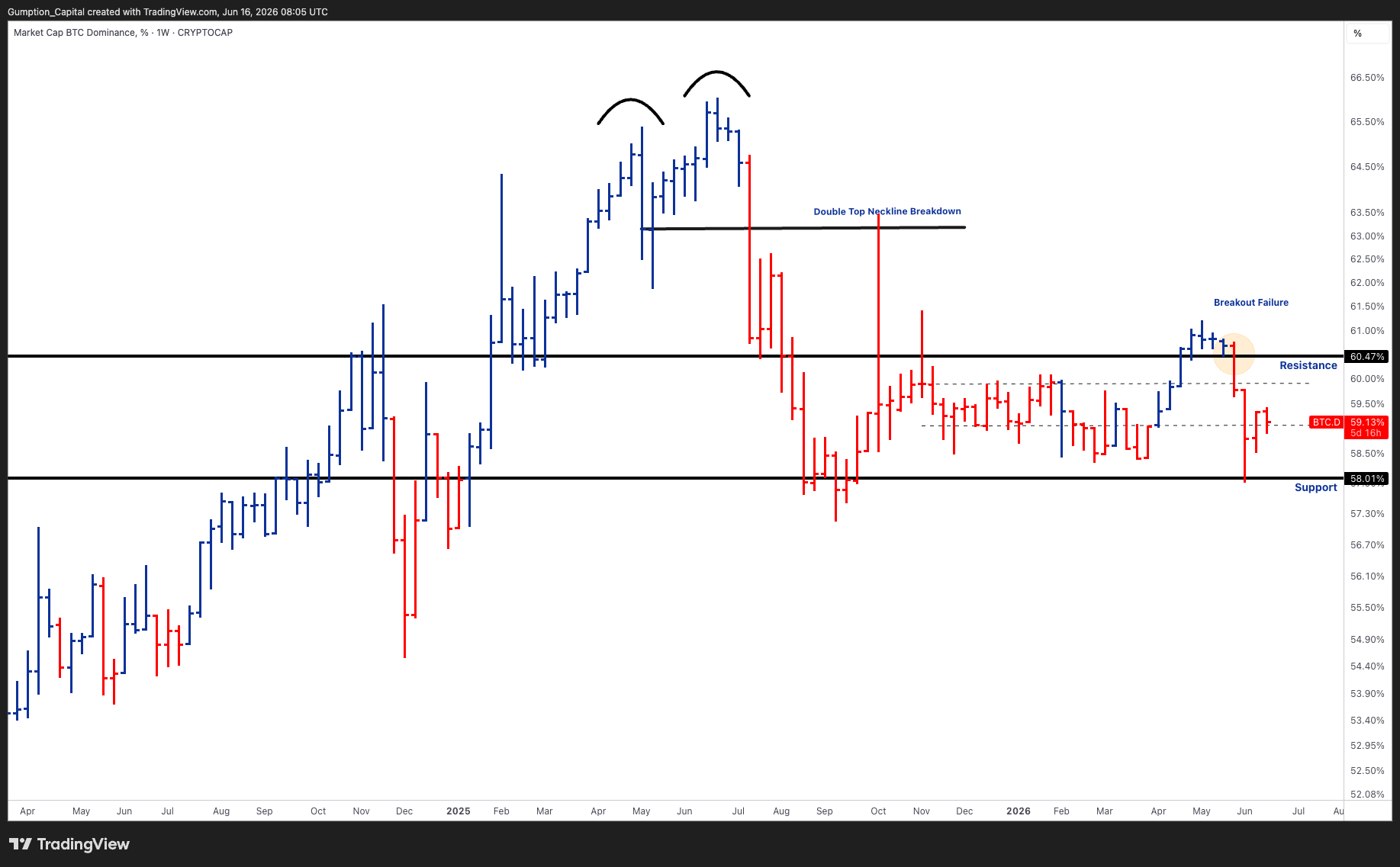

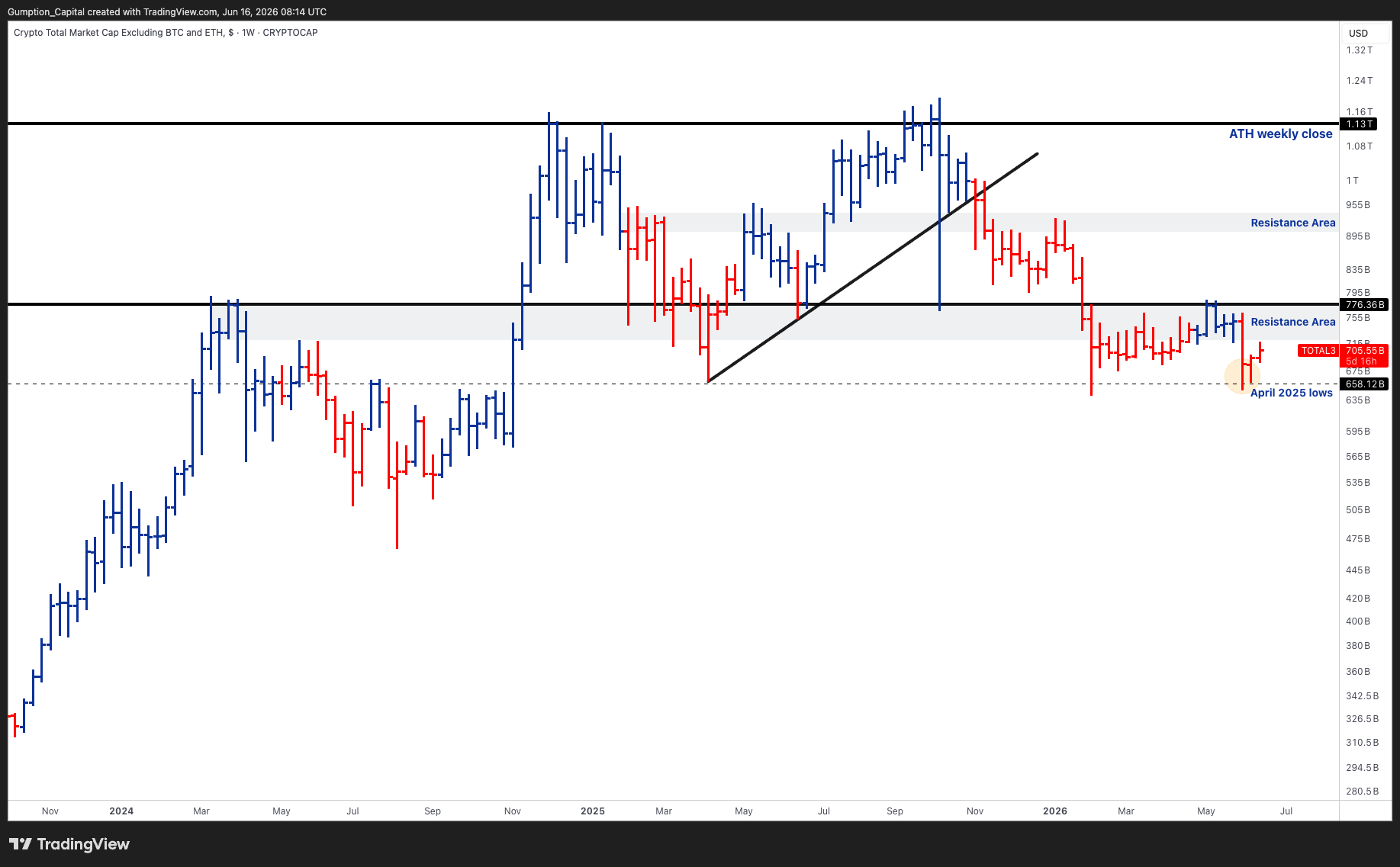

- The market is not yet trading like a broad institutional recovery. BTC is near $66k, sitting in the zone between the lower AVWAP band support at $63,641 and the March 29 anchored AVWAP at $71,306. That intermediate level is the first technical gate: BTC must clear the March 29 AVWAP before the $79k-$80k structural repair band becomes relevant, and the larger $85k-$87.6k AVWAP cluster remains the full regime confirmation level. TOTAL3 fell further to $696.34B — well below the $776B breadth-repair threshold — even as BTC bounced. The recovery is BTC-specific, not regime-wide.

- Flows reinforce that read. Spot BTC ETFs ran 13 consecutive outflow sessions totalling more than $4.4B before June 12 produced the first clean positive print (+$85.9M, zero funds negative). ETH ETFs continued to bleed with no stabilisation signal. When capital rotated out of BTC and ETH products on June 9, it did not return to ETH on relative value; it moved into SOL and XRP listed wrappers, which absorbed approximately $226M in combined inflows. The broader implication is that the ETF product complex is now deep enough across asset classes to function as an active capital-rotation vehicle, not just a BTC and ETH access tool.

- Macro did not provide the relief valve crypto needed. May CPI printed at +4.2% YoY — the highest reading since April 2023, up from 3.8% in April — driven by a 3.9% monthly surge in energy prices and a 7% jump in gasoline. Core CPI offered partial relief at +0.2% MoM, slower than April's 0.4%, but May PPI compounded the pressure: +1.1% MoM, +6.5% YoY, the highest annual rate since November 2022, with final demand goods surging 2.8% MoM. The one constructive macro development was oil, which sold off 4.2% to $80.72 — the first real-time input with the potential to cool the June CPI print. Gold surging 2.5% to $4,326 alongside the oil decline is the market hedging stagflation risk while beginning to price in the possibility of energy reversal.

- Cross-asset transmission remained broken. BTC/ES fell to 8.66, breaking below the approximately 9.0 reference level that had provided a floor in early June. The S&P 500 gained 0.5% with VIX compressing to 16.75, confirming that BTC is losing ground to equities even on sessions when equity sentiment improves — the constraint is crypto-specific, not macro-broad.

Our take: This was not a broad crypto recovery; it was BTC bouncing from seller exhaustion while the rest of the complex continued to deteriorate. TOTAL3 fell to $696B even as BTC moved 5% higher, ETH/BTC leaked lower and BTC/ES broke through a key reference. The constructive signals were narrow and deliberate: the 13-session ETF bleed produced its first zero-fund-negative session, SOL and XRP wrapper rotation confirmed that the listed-product layer is functioning as a capital reallocation mechanism, and oil's decline opened the first credible macro path to CPI softening. The regime remains rates-hostile and BTC-isolated. Until the June 12 ETF green day sustains across multiple sessions, TOTAL3 reclaims $776B and the FOMC avoids introducing explicit hike bias on June 16-17, the correct frame is stabilisation, not recovery.

BTC - One green ETF day, AVWAP still overhead

- BTC is near $66k, sitting between the lower AVWAP band support at $63,641 and the March 29 anchored AVWAP resistance at $71,306. That intermediate structure is what matters now. The $79k-$80k repair band and the $85k-$87.6k AVWAP cluster remain the larger targets, but neither becomes relevant until $71,306 is reclaimed. That level represents the average cost of all participants who entered since late March; below it, they are underwater and represent a defined layer of overhead supply. A weekly close above $71,306 would be the first meaningful technical confirmation since the breakdown.

- ETF flows remain the central constraint. Spot BTC ETF sessions from Monday through Friday of the prior week were approximately -$483.8M, -$519.1M, -$396.6M, +$3.2M and -$325.7M before June 12 produced a clean +$85.9M print with zero funds reporting an outflow. The cumulative 13-session bleed exceeded $4.4B. The zero-fund-negative character of the June 12 session is the important detail: it is a higher-quality stabilisation signal than a positive aggregate with mixed fund behaviour underneath, because it suggests distribution is approaching exhaustion rather than simply pausing.

- BTC/ES fell to 8.66, breaking below the approximately 9.0 reference level. With the S&P 500 up 0.5% and VIX at 16.75, the equity environment is calm. BTC underperforming equities on a session when both equities gained and volatility compressed confirms the drag is internal to crypto, not a macro transmission problem.

- Performance context reinforces the repair framing: BTC is -16.98% over one month, -25.06% YTD, and -37.76% over one year. The 3.72% weekly recovery is real but does not yet reverse the dominant trend.

Our take: BTC's issue this week is not that it failed to make a new high — it is that it remains below the level where the March-onward buyer base breaks even. The $71,306 AVWAP is the first credible near-term target not because clearing it resolves the larger repair case, but because it removes a defined layer of overhead supply and gives the market a technical reference to trade against. The June 12 ETF green day is necessary but not sufficient: the flow data needs to confirm across two to three additional sessions before it can be treated as a genuine turning point rather than a one-day positioning reset. The FOMC binary on June 16-17 frames the near-term range clearly — a patient hold opens the path toward $71,306; a hawkish hold with an upward dot-plot shift returns focus to $63,641 as the support level that must not break. Until BTC reclaims $79k-$80k with ETF outflows slowing materially, rallies should continue to be treated as relief attempts rather than trend resumption.

ETH - Price-lagging, bypassed in the rotation

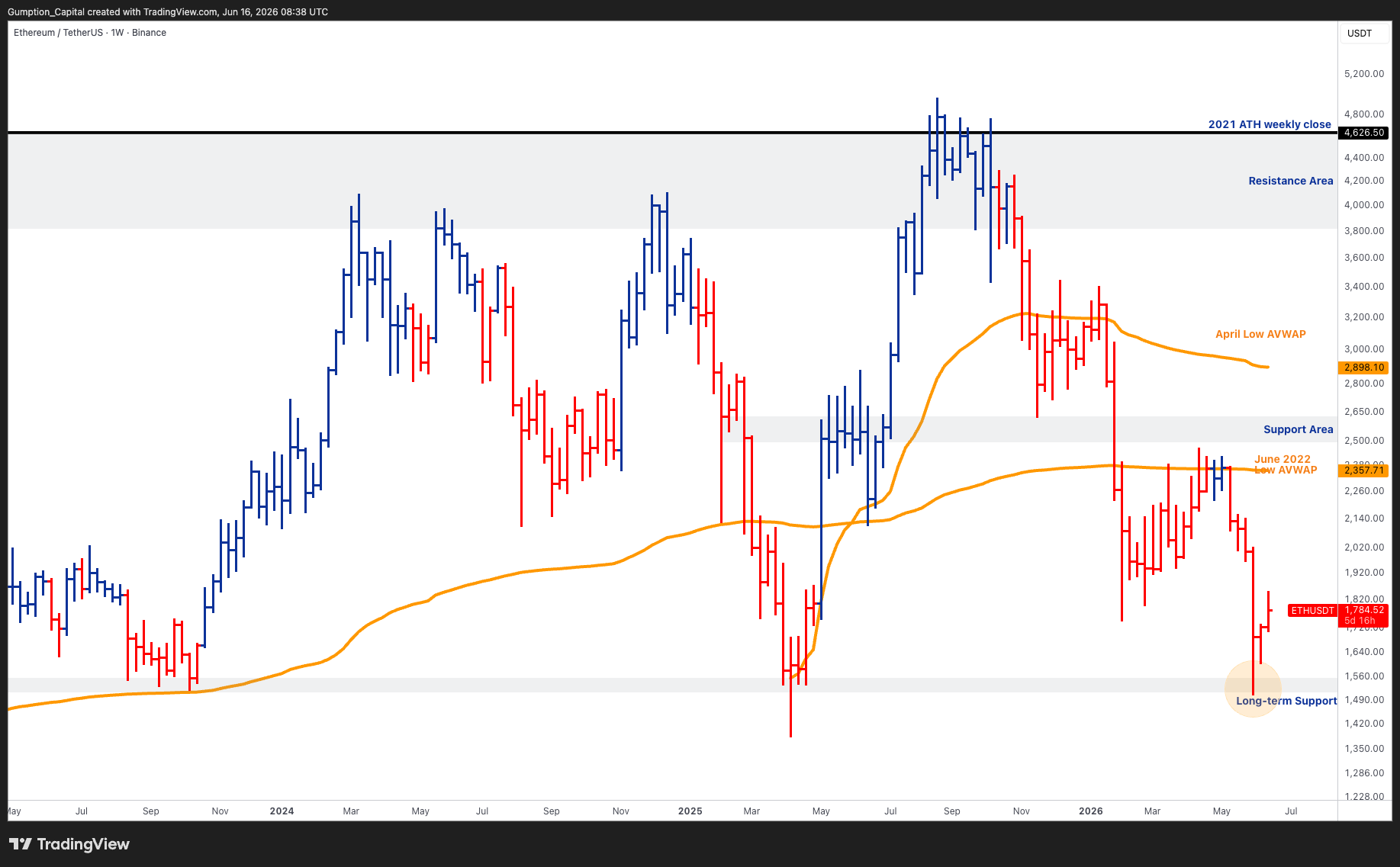

- ETH traded near $1,800, recovering marginally from the prior week but still approximately 27% below the $2,350-$2,400 validation zone. The June 2022 AVWAP region remains out of reach, and the April-low AVWAP reference is well above current levels. ETH dominance fell to 8.94%, compressing ETH/BTC to approximately 0.026 — above the major 0.025 structural pivot but continuing its multi-week decline toward that level.

- Spot ETH ETFs saw continued outflows through the week with no stabilisation signal. The rotation that emerged on June 9 bypassed ETH entirely: capital leaving BTC and ETH products moved into SOL and XRP wrappers rather than rotating back into ETH on relative value grounds. ETH is not the institutional rotation destination when large-cap crypto flows are negative.

- Ethereum-adjacent infrastructure continued to develop. Base's scaling activity, Aave's expanding regulated footprint and the broader stablecoin settlement narrative remain structurally intact. None of that has reversed ETF outflows, arrested ETH/BTC weakness, or changed the spot-price rejection at the $2,350-$2,400 repair zone.

Our take: Ethereum remains institutionally relevant at the infrastructure layer but price-lagging at the asset layer — the same frame as prior weeks, and it has not yet earned an upgrade. The medium-term thesis around tokenised collateral, stablecoin settlement, staking demand, DeFi credit and L2 scaling is structurally valid, but the market is not paying for that optionality while ETF flows are negative and ETH/BTC is leaking toward 0.025. The distinction for institutional readers is that ETH's infrastructure value and ETH's price leadership are currently decoupled, and the market is showing no sign of closing that gap through flow demand. The conditions for reconnection remain unchanged: spot ETF outflows must slow, ETH/BTC must hold and build above 0.025, and price must reclaim $2,350-$2,400. Until all three arrive simultaneously, ETH strength should be treated as tactical relief rather than the start of a leadership rotation.

SOL & BNB - Rotation beneficiary, not yet a leader

- SOL traded at ~$74k, up approximately 10% from the prior week's $64.7k — the strongest price recovery among major alts — but still approximately 37% below the $112-$113 reclaim zone. SOL was a direct beneficiary of the XRP/SOL ETF rotation on June 9, with combined inflows of approximately $226M as capital exited BTC and ETH products. That wrapper demand is constructive, but it remains too modest in scale and too distant from the price trigger to support a leadership call.

- BNB traded at ~$615, up approximately 3.5% on the week, still roughly 17% below the $742 acceptance level. VanEck's VBNB continues to provide listed ecosystem access, but that productisation has not yet translated into price acceptance above the confirmation zone.

- XRP ETFs recorded their sixth consecutive week of net inflows, reaching $1.44B cumulative since the November 2025 launch. That consistency through a broadly negative ETF environment establishes XRP as one of the cleaner institutional rotation expressions in the current cycle, even if it sits outside the primary analytical framework given its distinct regulatory and network profile.

Our take: The SOL and BNB setups are cleaner in structure than in price. SOL's 10% bounce and direct ETF rotation inflows are more constructive than anything in ETH's current flow picture, but being a rotation beneficiary is not the same as being a confirmed leader. SOL needs $112-$113 with sustained wrapper demand to earn that description; below it, the asset remains liquid beta that amplifies moves in both directions without yet confirming a regime shift. BNB is the more interesting productisation story — VBNB gives the market a listed access channel precisely as BNB presses toward a technically relevant level — but the same discipline applies: the language does not upgrade until price acceptance above $742 confirms. The note should not get ahead of the price.

Alpha Cluster - WLD builds; HYPE tests the wrapper thesis

- WLD remained the clearest directional expression of the AI identity theme, trading near $0.49 and up approximately 70% over the prior month. The catalyst stack continued to compound: Arthur Hayes publicly endorsed the token after rotating out of HYPE, citing Elon Musk optionality and proximity to the AI company IPO cycle; the July 24 supply unlock will reduce daily issuance by approximately 43%, from roughly 5.1M to 2.9M WLD/day; and the asset is outperforming inside a damaged large-cap tape, which is the defining characteristic of durable selective alpha rather than speculative rotation noise.

- HYPE fell approximately 14.7% over the week to approximately $50-53, extending the post-ATH correction that followed the June 6 $700M token unlock. Listed-product wrapper demand remained marginally resilient through the price decline. The question the correction poses is direct: if wrapper inflows hold while price corrects, the ATH was a consolidation high and the institutional derivatives utility thesis remains intact; if wrapper flows follow price lower, the ATH was a distribution event.

- The House Ways and Means Committee held its digital asset taxation hearing on June 9, circulating seven draft bills covering de minimis relief ($10 per fee, capped at 5,000 transactions per year), staking and mining tax deferral and wash sale rule clarification. Written submissions are due June 23. This is a discussion hearing, not a markup — no legislation passes today — but advancing to a full committee hearing is the prerequisite step before any of those drafts can move.

Our take: The alpha message is the same as the prior week: narrow, AI-anchored, and not a signal that broad alt rotation has returned. WLD is the cleanest expression because the catalyst stack is unusually precise — an identifiable institutional backer, a hard-dated supply event and a direct read-through from the AI equity cycle rather than reliance on generic risk appetite. The risk is front-running: with the July 24 unlock six weeks away, the three weeks ahead of that date will establish whether positioning has already absorbed the event or whether structural demand sustains the move into the supply reduction. HYPE's correction is the alpha cluster's key test this week — wrapper flows sustaining through a 14.7% drawdown would be a stronger confirmation of the institutional derivatives thesis than any single positive price session. The Ways and Means hearing is not a near-term price catalyst, but the legislative direction toward de minimis relief, staking deferral and wash sale clarity represents a structural tailwind for U.S. participation breadth that complements the institutional product-layer build without yet reaching the price.

Rails, Regulation & Institutionalisation - Tax reform and bank tokenisation advance

- The House Ways and Means Committee's seven crypto tax discussion drafts are the most substantive U.S. digital asset tax reform package since the 2021 infrastructure bill. De minimis relief at $10 per fee capped at 5,000 transactions per year, staking and mining tax deferral until disposal, and wash sale rule clarification together address the three primary frictions that have kept U.S. retail participation structurally below institutional adoption. Written submissions close June 23 ahead of potential markup.

- JPMorgan, Citigroup, Wells Fargo and Bank of America are advancing a tokenised deposit network through The Clearing House, targeting a 1H27 launch. This is the commercial-bank complement to the DTCC/Stellar public-chain tokenisation rail: while DTCC moves custodied securities onto Stellar, the bank consortium is building 24/7 bank-controlled tokenised settlement infrastructure — two parallel tracks converging on the same post-trade tokenisation outcome from different institutional starting points.

- The global stablecoin market cap reached a new all-time high of $320B, its fourth consecutive monthly expansion, even as broader digital asset prices continued lower. Stablecoin supply growing while crypto prices decline is a structural signal: dollar-denominated on-chain liquidity is compounding independently of market cycles.

- Oil's 4.2% weekly decline to $80.72 is the first meaningful macro tailwind in several weeks. Energy was the primary driver of May's CPI overshoot at +3.9% MoM. A sustained oil reversal would reduce the energy component in June CPI and materially shift the rate narrative ahead of the July FOMC.

Our take: Institutional plumbing continued to advance on every dimension regardless of where spot prices traded — the same bifurcation as prior weeks, but the macro picture is beginning to offer a potential reconnection path. Tax clarity, bank-led tokenised settlement, stablecoin supply growth and public-chain post-trade connectivity are all compounding on parallel tracks. Oil's decline is the most underappreciated development of the week. It does not change the June FOMC outcome, which is locked as a hold, but it is the first real-time input that could soften the July CPI print and reopen the rate-cut optionality that crypto needs to reconnect with equity risk appetite. The next phase requires productisation demand to reconnect with spot sponsorship — specifically BTC and ETH ETF flow stabilisation. Until that reconnection arrives, institutional infrastructure progress remains a medium-term structural support rather than a near-term price signal.

Outlook - FOMC to set the next gate

- The week ahead is an FOMC transmission test. The June 16-17 hold is near-certain at 3.5-3.75%, but the market will be focused on Powell's language and the dot-plot update. The best macro outcome for crypto is a patient hold with no explicit hike bias and an acknowledgement that core CPI softened to +0.2% MoM — enough to keep the rate-cut path open for later in the year without delivering an immediate easing signal.

- BTC's technical sequence is now explicitly layered. The first gate is the March 29 AVWAP at $71,306 — clearing that removes the overhead supply from the March buyer base and opens a path toward the $79k-$80k structural repair band. The second gate is $79k-$80k itself, the level required before allocators can treat the drawdown as a repair rather than a repricing. The third gate is the $85k-$87.6k AVWAP cluster, which represents full regime confirmation. Each gate requires ETF flow and cross-asset confirmation to hold.

- ETF flow follow-through is the most important near-term signal. The June 12 green day needs to extend to two to three additional positive or flat sessions to confirm the 13-session distribution sequence has ended. A renewed outflow print immediately after resets the stabilisation case and suggests the bleed was structural rather than positioning-driven.

- The broader technical map is unchanged. ETH needs $2,350-$2,400. ETH/BTC must hold and build above 0.025. TOTAL3 must reclaim $776B for breadth repair. SOL needs $112-$113. BNB needs $742 acceptance. Until those levels are reclaimed, the market remains in post-breakdown stabilisation, not regime repair.

- WLD's July 24 supply unlock is six weeks away. Oil at $80.72 and declining is the macro wildcard — a second week of energy softening would allow June CPI to track closer to core's 0.2% MoM trajectory and give the Fed room to shift language at the July meeting without requiring a full policy pivot.

Our take: The burden of proof remains on the bulls, but the evidence base is beginning to shift. One clean ETF green day, a 5% BTC bounce, an oil decline that could cool the next CPI print and six weeks of runway to WLD's supply catalyst are not a recovery — but they are a materially better starting position than the prior two weeks provided. The FOMC is the immediate binary: a patient hold validates the June 12 ETF signal and gives BTC a path toward the $71,306 AVWAP; a hawkish hold with a dot-plot upside shift returns the focus to $63,641 lower-band support and confirms that the macro regime is not yet ready to release pressure on duration-sensitive assets including crypto. The regime remains selective until proven otherwise: WLD for AI identity repricing, XRP and SOL for ETF rotation mechanics, BNB for productisation validation above $742. BTC and ETH remain tactical relief trades until ETF flows confirm across multiple sessions, TOTAL3 reclaims $776B and the layered AVWAP gates are cleared in sequence.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets