Regulatory Infrastructure Week & Crypto Consolidation

Blueprint - ETF Inflows End $2.73B Bleeding Streak. Macro Overhang Persists Into July FOMC

- The week's dominant theme was regulatory infrastructure, not price. Circle received final OCC approval for First National Digital Currency Bank, N.A. ("Circle National Trust") on July 10 — the first stablecoin issuer under direct federal bank supervision. SWIFT launched its live blockchain ledger with 17 banks from six continents on July 9, built on Hyperledger Besu, enabling 24/7 tokenized deposit settlements. The SEC released its "Regulation Crypto" rulemaking agenda. A new merged CLARITY Act draft (Senate Banking + Agriculture) is expected the week of July 20. These are structural milestones, not price catalysts — their institutional impact will compound over quarters.

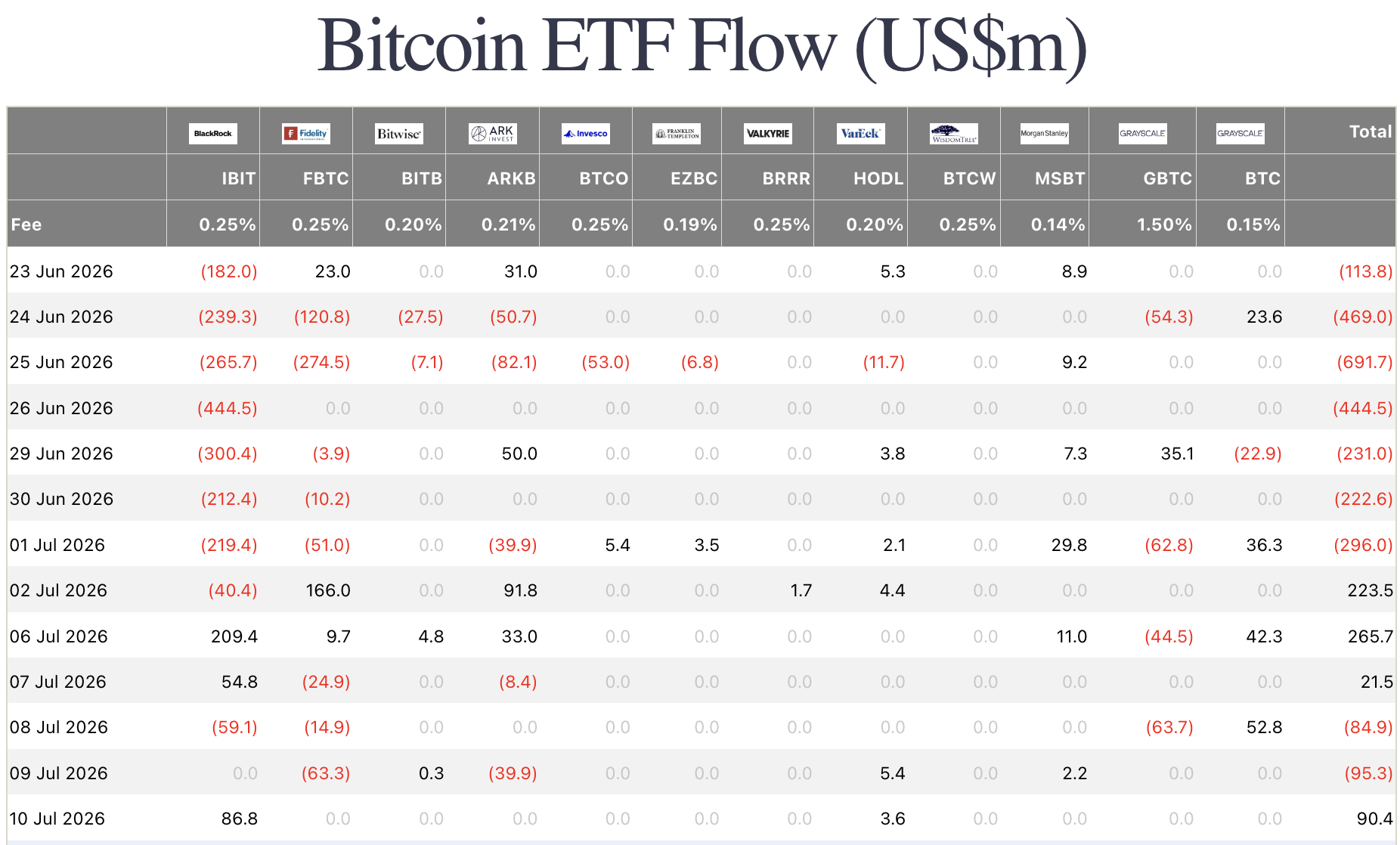

- BTC and ETH spot ETFs combined drew $282M in net inflows for the week, definitively ending eight consecutive weeks of combined outflows that had totaled $9.46B. BTC alone accumulated roughly $200M in weekly net inflows. The week's key data point: IBIT led recoveries (BlackRock +$253.71M on July 7 alone). When BlackRock leads, the institutional bid is genuine. Only one negative day: July 9 (-$52M).

- June CPI releases Tuesday July 14. The Cleveland Fed nowcast projects 3.96% YoY, a 24bp deceleration from May's 4.2%. A print below 3.8% likely triggers a crypto rally toward $70K; a print at or above 4.0% risks re-engaging the Fed hike narrative and renewing outflow pressure. Oil's 3.5-5% weekly gain on renewed US-Iran Strait of Hormuz disruptions is the main upside inflation risk heading into the print.

- The June FOMC minutes (released July 8) revealed "a few" officials saw a case for hiking at the June meeting but held back. This confirms the meeting was closer to a live hike than markets appreciated and that July 28-29 is genuinely live if June CPI disappoints.

- Altcoin Season Index rose to 52/100 — the highest in three months and the first reading above 50 since March 2026. Early-stage rotation signal, not confirmed alt season. Capital appears to be distributing beyond BTC and ETH into ADA (+25%), BCH (+22%), Lighter (+50%+), and MemeCore (+89%).

Our take: The market is in a structural pause, not a reversal. Last week's recovery set the floor; this week's consolidation is the breath before the next move. The direction of that move will almost entirely be determined by the June CPI print on July 14; the single most important near-term macro event.

The regulatory infrastructure events are structurally more important than this week's price action. Circle's national bank charter changes the counterparty risk profile for institutional USDC. Federal oversight means parity with bank trust departments managing pension and endowment assets. SWIFT going live with 17 banks on tokenized deposits means the global correspondent banking network is an active participant in on-chain settlement, not a spectator. The CLARITY Act's imminent new draft means US digital asset legislation is weeks from the Senate floor. None of these are narrative events, they are infrastructure events whose impact on institutional crypto allocation will be felt over quarters.

BTC - Consolidating At $64k With Etf Streak Finally Broken

- BTC held $63,909 this week (+2.76% WoW), consolidating above $62K support established after last week's recovery from $58K. Price action was orderly within a tightening range — consistent with accumulation behavior, not distribution.

- The 8-week ETF outflow streak ($9.46B cumulative) was definitively broken with ~$200M in weekly net BTC inflows. July 7: +$253.71M (BlackRock IBIT led with +$3,285 BTC on the day). Only negative day: July 9 (-$52M). When IBIT leads recoveries, the institutional bid is real.

- BTC dominance rose from 55.5% to 56.3% — +0.8pp week-over-week — even as the Altcoin Season Index climbed to 52/100. This atypical combination (dominance rising alongside alt season signal) suggests broad capital inflow rather than BTC-to-alt rotation. New money entering, not old money rotating.

- BTC/ES ratio: 63,909 / 7,620 = 8.39 — below the 9.0 reference floor for the second consecutive week. Institutional rotation from equities into BTC has not yet reengaged at scale. This ratio reclaiming 9.0 remains the trigger to watch.

Our take: BTC is well-positioned heading into the CPI print: above support, with a broken ETF outflow streak and whale accumulation from two weeks ago still intact. A constructive CPI (below 4.0%) could push BTC to test $68K-$70K within five trading days. A hot print risks a $60K retest. The structural setup provides the floor; macro provides the catalyst. Position sizing matters more than directional conviction this week.

AVWAP note: Manual verification required before publishing. Open BTCUSD on TradingView, anchor AVWAP to June 28-29 swing low (~$58K). Insert AVWAP level, upper band, and lower band into this section.

ETH - Digesting Last Week's Gains, Rails Narrative Building

- ETH closed essentially flat at $1,802.89 (+0.46% WoW), digesting last week's +13% surge on Ethereum Institutional's launch. Consolidation after a single large catalyst week is structurally healthy — it tests buyer commitment at elevated prices. So far, buyers are holding.

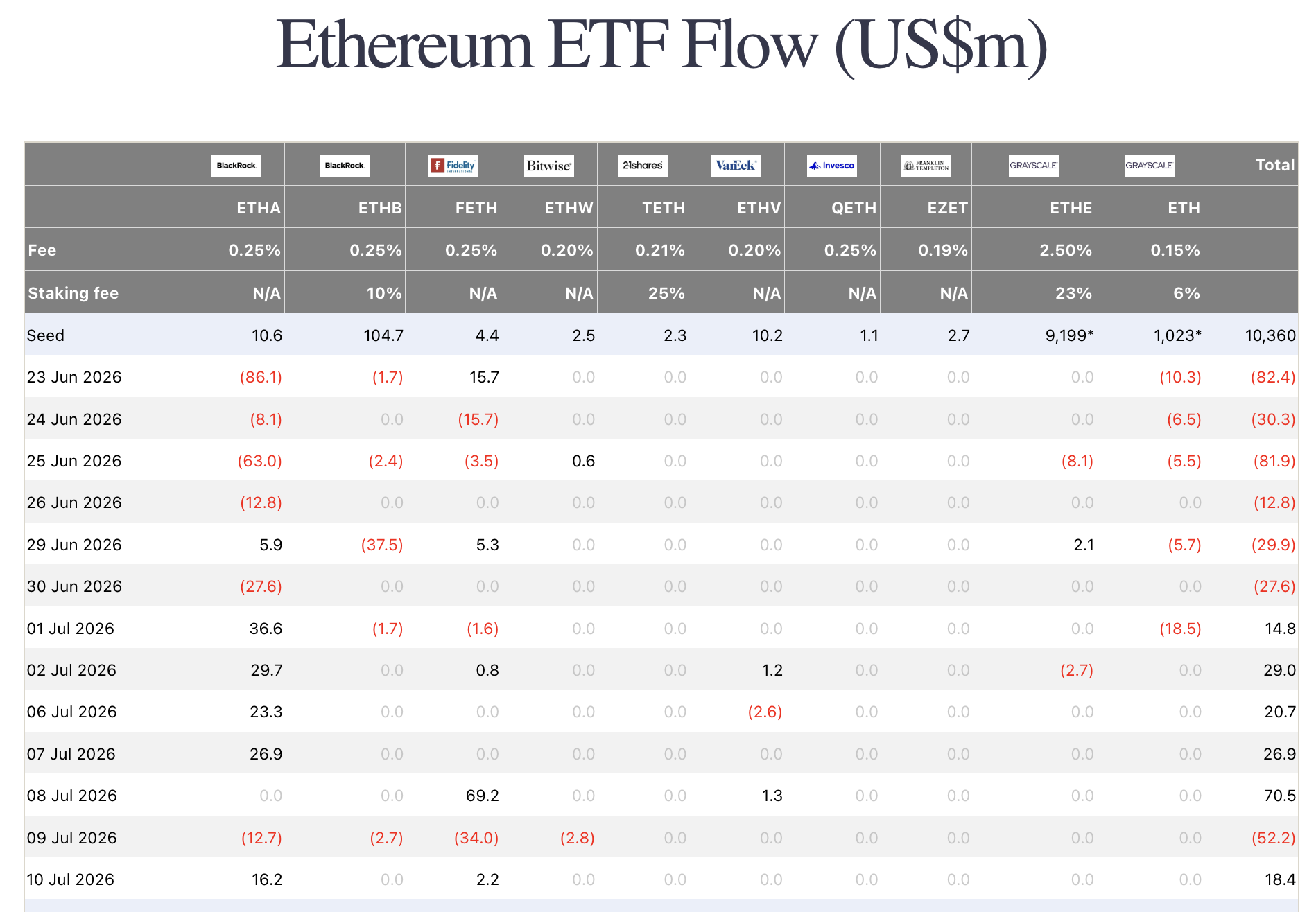

- ETH ETF inflows extended to four consecutive positive days through July 7, with that day alone recording +$26.9M (all from BlackRock ETHA). Weekly net: approximately +$36.37M (~20,570 ETH). Modest, but the directional shift from weeks of outflows is meaningful.

- ETH/BTC ratio: -0.50% WoW to approximately 0.0282 — essentially unchanged after last week's +6.60% move.

Our take: ETH is behaving correctly after a +13% catalyst week. The next significant move likely comes from one of three sources: (1) a constructive CPI on July 14, (2) first concrete Ethereum Institutional partnership announcement, or (3) CLARITY Act passage enabling US staking ETF products. Watch for the ETH/BTC ratio to break above 0.030 as the institutional rotation confirmation signal.

SOL & BNB - Pump Unlock Hits Sol; Alt Rotation Beginning

- SOL fell 5.15% to $76.49 — confirming that the PUMP unlock ($123.65M, 21.35% of supply) created the selling pressure flagged in last week's draft. The decline is supply-driven, not ecosystem-driven. Solana network activity remains among the highest in crypto; the price impact is mechanical.

- BNB gained 1.37% to $572.98, continuing its BTC-beta behavior. No independent catalyst. BNB will accelerate with crypto risk-on, not lead it.

- Altcoin Season Index at 52/100 is the most important alt market signal this week. Above 50 for the first time since March, the index suggests capital is beginning to rotate. Historical analogues: once the index crosses 60, broad alt momentum typically sustains for 4-8 weeks. At 52, we are at the inflection point — CPI on July 14 determines whether it accelerates or reverses.

- TOTAL3 declined 1.85% to $672.4B, driven primarily by SOL. Ex-Solana, the broader alt market was roughly flat — consistent with early rotation rather than broad selling pressure.

Our take: SOL's PUMP unlock pullback is an event-driven dip, not a structural break. The unlock selling should absorb over the next 2-3 weeks. JTO and GRASS unlocks (also July) may add secondary pressure but at far lower magnitudes. If CPI cooperates on July 14, SOL has room to reclaim $80+ quickly. The Altcoin Season Index at 52/100 is the most actionable signal for positioning in the alt space — be positioned before the index crosses 60, not after.

Alpha Cluster - Alt Season Clock Ticking, Lighter And Defi Lead

- Lighter (LIT) surged over 50% this week — the standout institutional alpha name. A decentralized derivatives exchange with $40B in 30-day trading volume, Lighter represents the on-chain perp narrative gaining traction as CEX-to-DEX migration accelerates. The 13.5% 24-hour move at week's end suggests momentum building, not exhausting.

- MemeCore +89%, ADA +25%, BCH +22%, DEXE +23% — the week's broad alpha breadth confirms early-stage rotation rather than concentrated narrative. When top performers span speculative (MemeCore), established L1s (ADA), and legacy forks (BCH), capital is spreading, not concentrating.

- The SEC's "Regulation Crypto" agenda — startup registration exemptions for up to four years and a $75M annual fundraising exemption without full agency registration — directly reduces compliance barriers for altcoin projects seeking US market access. Projects discounted for securities classification risk get a structural re-rating when this framework finalizes.

- XRP spot ETF approaches $1B in net assets. Ripple's full MiCA CASP authorization (all 30 EEA countries) gives XRP the cleanest regulatory footprint of any non-BTC/ETH asset. CLARITY Act week of July 20 could add US clarity on top of the EU license — a compounding catalyst for XRP if it lands.

Our take: The alpha story this week is breadth. Broad gainers across speculative, DeFi, L1, and legacy-fork categories signal early alt season, not a mature one. Early-stage positioning — before the Altcoin Season Index crosses 60 — has historically offered the best risk/reward. The SEC exemption framework and the CLARITY Act together represent a regulatory unlock for altcoins that have been systematically discounted for US classification risk. That discount unwinds when clarity lands.

Rails, Regulation & Institutionalisation - Circle Gets Its Bank, Swift Goes Live, Clarity Coming

- Circle received final OCC approval for First National Digital Currency Bank, N.A. (to operate as "Circle National Trust") on July 10, 2026. This makes Circle the first stablecoin issuer under direct federal bank supervision, placing USDC custody under regulatory parity with bank trust departments — the custodians of pension, endowment, and institutional capital. Application filed June 30, 2025; conditional approval December 2025; final approval July 10, 2026.

- SWIFT launched its live blockchain ledger on July 9 with 17 banks from six continents piloting tokenized deposit payments (DBS, UOB, OCBC, Standard Chartered, BNP Paribas, MUFG, HSBC, UBS, BNY, Citi, Wells Fargo, and others). Built on Hyperledger Besu. The ledger orchestrates 24/7 cross-border settlement above existing payment rails — not replacing them. First live transaction use case for tokenized interbank settlement at global scale.

- CLARITY Act: A merged Senate Banking + Agriculture committee draft is expected the week of July 20. The bill needs 60 votes; three unresolved issues remain — an ethics provision restricting senior officials with crypto ties, DeFi protections (BRCA Section 604), and Democratic threshold support. Senate floor action targeted for late July, but chamber has only weeks before summer recess.

- Ripple received full MiCA CASP authorization from Luxembourg's CSSF on July 6, covering all 30 EEA countries. One of approximately 210 firms (of 1,200+ that previously operated in EU) to survive the July 1 MiCA enforcement deadline. XRP payments are now fully licensed across the EU.

Our take: This was the most consequential regulatory and infrastructure week in crypto since the US spot Bitcoin ETF launch in January 2024. Circle's national bank charter, SWIFT's live ledger, and Ripple's full MiCA license represent the formalization of on-chain finance within regulated banking infrastructure; not pilots, not announcements, but live regulated operations.

For Hex Trust, the strategic implications are direct. Circle National Trust becoming a federally regulated custodian creates new framing for institutional custody comparisons. SWIFT's live tokenized deposit ledger with major global banks means correspondent banking clients are now active on-chain settlement participants. They need compliant custodians, reporting infrastructure, and risk management on the other side. The CLARITY Act's imminent landing will accelerate US institutional entry. These are tailwinds for regulated institutional custodians, compounding over the next 12-18 months.

Outlook - Pre-Cpi Silence Before July 14 Thunder

- June CPI releases July 14 at 8:30am ET. Cleveland Fed nowcast: 3.96% YoY (down from May's 4.2%). Consensus tightly clustered 3.9-4.0%. Market interpretation: above 4.0% = hike narrative re-engages; below 3.8% = October cut odds surge and crypto rallies; 3.8-4.0% = status quo holding pattern.

- June FOMC minutes (July 8) revealed "a few" officials saw a case for hiking at June's meeting. Confirms July 28-29 is a genuinely live meeting if June CPI disappoints. Nine of 18 officials still project at least one 2026 hike. Fed funds rate held at 3.5-3.75%.

- US 10-year yield rose to 4.54-4.56% — up 8bp from last week's 4.46% close. The driver: WTI crude oil gained 3.5-5% to ~$71.41 on renewed US-Iran tensions disrupting Strait of Hormuz shipping. Higher oil = higher energy CPI contribution = higher nominal inflation expectations = higher yields. This feedback loop is the primary upside risk to the July 14 print.

- VIX fell to 15.02 (-11.91% WoW) as equities continued higher (+1.07% SPX Closing at $7,575.39). Market is positioned for CPI cooperation — calm volatility and rising equities both assume a benign print. This creates asymmetry: limited upside from a good CPI (priced), significant downside from a hot one.

- June PPI releases July 15. July FOMC: July 28-29. No Fed speakers this week (quiet period / post-holiday blackout).

Our take: The market is dangerously calm heading into the most important macro data point of the past six weeks. VIX at 15 with equities near highs means positioning is long and complacent — the setup where a surprise CPI print causes maximum damage. The oil-driven yield move (+8bp this week) is the warning signal: if crude holds above $72, energy CPI won't cooperate with the disinflation narrative, and 3.96% may prove optimistic.

For crypto, asymmetry is clear: CPI at or below 3.8% likely pushes BTC toward $70K within five trading days; CPI at or above 4.0% risks retesting $60K. The structural setup (whale accumulation, broken ETF streak, Circle/SWIFT infrastructure) provides the floor. But macro overrides structure in the near term. The right posture heading into Monday: positioned for the upside scenario, sized for the downside scenario.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets