Below the Reclaim: Rails Build as Beta Breaks Further

Blueprint - Spot Beta Breaks Deeper, Institutional Rails Advance

- The market is not yet trading like a broad institutional reaccumulation phase. BTC is near $61.9k, still materially below the $79k-$80k repair band and far from reopening the $85k-$87.6k AVWAP cluster. ETH is near $1.63k, well below the $2,350-$2,400 validation zone. SOL is near $64.7, far beneath the $112-$113 reclaim area, while BNB is near $594, still below the $742 acceptance level required to confirm productisation-led leadership. The chart message is therefore not “capitulation complete”; it is “post-breakdown stabilisation without regime repair.”

- Flows reinforce that read. Spot BTC ETFs saw approximately $1.72B of net outflows from 1–5 June, with four negative sessions and only one marginal positive print. ETH ETFs also remained under pressure, with approximately $174M of net outflows over the same period. SOL wrappers were marginally negative, while HYPE was the only clear listed-product outlier, attracting approximately $17M of net inflows. That makes HYPE a selective productisation winner, not proof of broad alt-beta repair.

- Macro did not provide the relief valve crypto needed. ISM manufacturing rose to 54.0, ISM services rose to 54.5, payrolls surprised to the upside at 172k, and unemployment held at 4.3%. The issue was the mix: resilient activity arrived alongside elevated price pressure, higher Treasury yields and renewed rate-hike concern into the 16–17 June FOMC. In that environment, crypto’s duration-like characteristics were exposed precisely as ETF demand was weakening.

- Equity beta also failed to cushion the tape. Broadcom reported AI semiconductor revenue of $10.8B, up 143% YoY, and guided Q3 AI semiconductor revenue to $16.0B, but the stock still sold off because expectations had already priced in perfection. Friday’s payroll-driven de-risking then pushed the Nasdaq down 4.18% and the S&P 500 down 2.64%. The important cross-asset point is that crypto weakened before the broader equity break and did not regain leadership when equities sold off.

Our take: This is a price-first market. The institutional rails story remains real, but the charts are not validating a new allocation cycle. BTC is not hovering just below resistance; it is trading far below the reclaim zone that would turn a bounce into a repair attempt. ETH’s infrastructure narrative remains intact, but price is still disconnected from the tokenisation and staking thesis. SOL is too far below its leadership trigger to be described as rotation leadership, and BNB’s VBNB launch is structurally important but not yet confirmed by acceptance above $742.

That makes the current regime defensive but conditional, not irreparably bearish. The market has become oversold enough for sharp relief rallies, especially if inflation data softens and ETF outflows slow. But the difference between a relief rally and a regime shift is acceptance. BTC needs $79k-$80k, ETH needs $2,350-$2,400, ETH/BTC needs to rebuild above 0.0250, TOTAL3 needs to regain $776B, SOL needs $112-$113, and BNB needs $742. Until those levels are reclaimed, institutional infrastructure progress remains a medium-term support story rather than a near-term price signal.

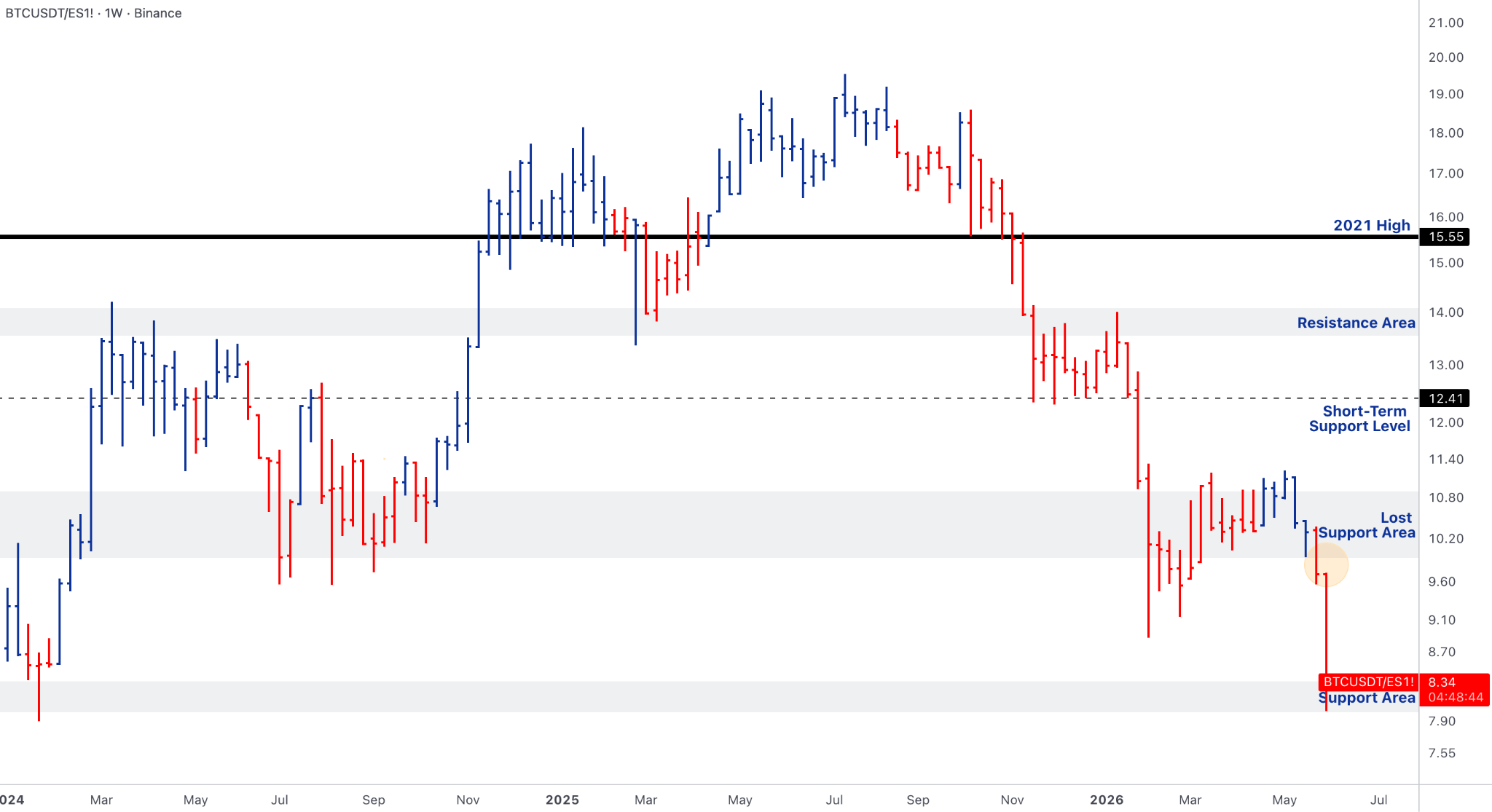

BTC - Distribution Until $80k Reclaim

- BTC is trading near $61.9k, leaving it roughly 22% below the lower end of the $79k-$80k repair band. That distance is the central technical point. The $79k-$80k zone is not just upside resistance; it is the failed-support region that needs to be recovered before allocators can treat the drawdown as a repair rather than a repricing. The market is not yet retesting the breakdown zone; it is still trading in the post-breakdown field where rallies can be violent but unconfirmed. Only a reclaim of $79k-$80k would reopen the prior AVWAP cluster around $85k-$87.6k and force a reassessment of seller control.

- ETF flows remain the major constraint. Daily spot BTC ETF flows were approximately -$483.8M, -$519.1M, -$396.6M, +$3.2M and -$325.7M from Monday to Friday, producing a weekly net outflow of roughly -$1.72B. Thursday’s marginal inflow was not enough to mark stabilisation because it was immediately followed by renewed Friday selling. The flow structure still says distribution, not accumulation.

- The BTC/ES signal also deteriorated. Crypto weakened while AI equities were still absorbing risk appetite earlier in the week, then equities themselves broke lower after payrolls and Broadcom. That sequence makes BTC’s underperformance more important: it was not a harmless crypto-only flush, but an early sign that liquidity was becoming less forgiving across risk assets.

Our take: BTC remains below the level where institutional buyers need to prove themselves. At current levels, the market is still closer to stress management than trend repair. The first bullish confirmation is not a new high; it is a reclaim of $79k-$80k with ETF outflows slowing at the same time. Without both, rallies should be treated as short-covering and volatility compression rather than renewed institutional accumulation.

The next risk is that BTC continues to behave as the weakest expression of risk appetite even while rails improve beneath the surface. That is the key tension. The long-term institutional access channel is deeper than in prior cycles, but the current ETF tape is a source of supply, not demand. Until flows stabilise and BTC/ES stops deteriorating, the market should remain cautious on any bounce that fails below the repair band.

ETH - Infrastructure Thesis, No Flow Confirmation

- ETH is trading near $1.63k, leaving it roughly 30% below the $2,350-$2,400 validation zone. That makes the chart structure materially weaker than the narrative backdrop. ETH is not yet attempting leadership; it is still trying to stabilise below the level that would put the June 2022 AVWAP region and broader structural repair back in play.

- Spot ETH ETFs saw approximately $174M of net outflows from 1–5 June. Thursday’s +$19.3M inflow briefly interrupted the redemption sequence, but Friday reverted to a negative print. ETH/BTC also needs to defend and rebuild above 0.0250 before ETH can be described as a relative-strength leader rather than a high-beta extension of large-cap weakness.

Our take: ETH remains a latent infrastructure asset without current market confirmation. The medium-term thesis around tokenised collateral, stablecoin settlement, staking, DeFi credit and institutional on-chain rails remains valid, but price is not yet paying for that thesis. This week’s message was demand withdrawal, not demand return.

The distinction matters for institutional readers. ETH still has one of the clearest medium-term institutional use cases in crypto, but the market is not rewarding that optionality while ETF flows are negative and ETH/BTC remains fragile. A constructive turn requires three signals together: spot ETF outflows must slow, ETH/BTC must hold and improve from the 0.025 area, and ETH must reclaim $2,350-$2,400. Until then, ETH strength should be treated as tactical relief rather than leadership.

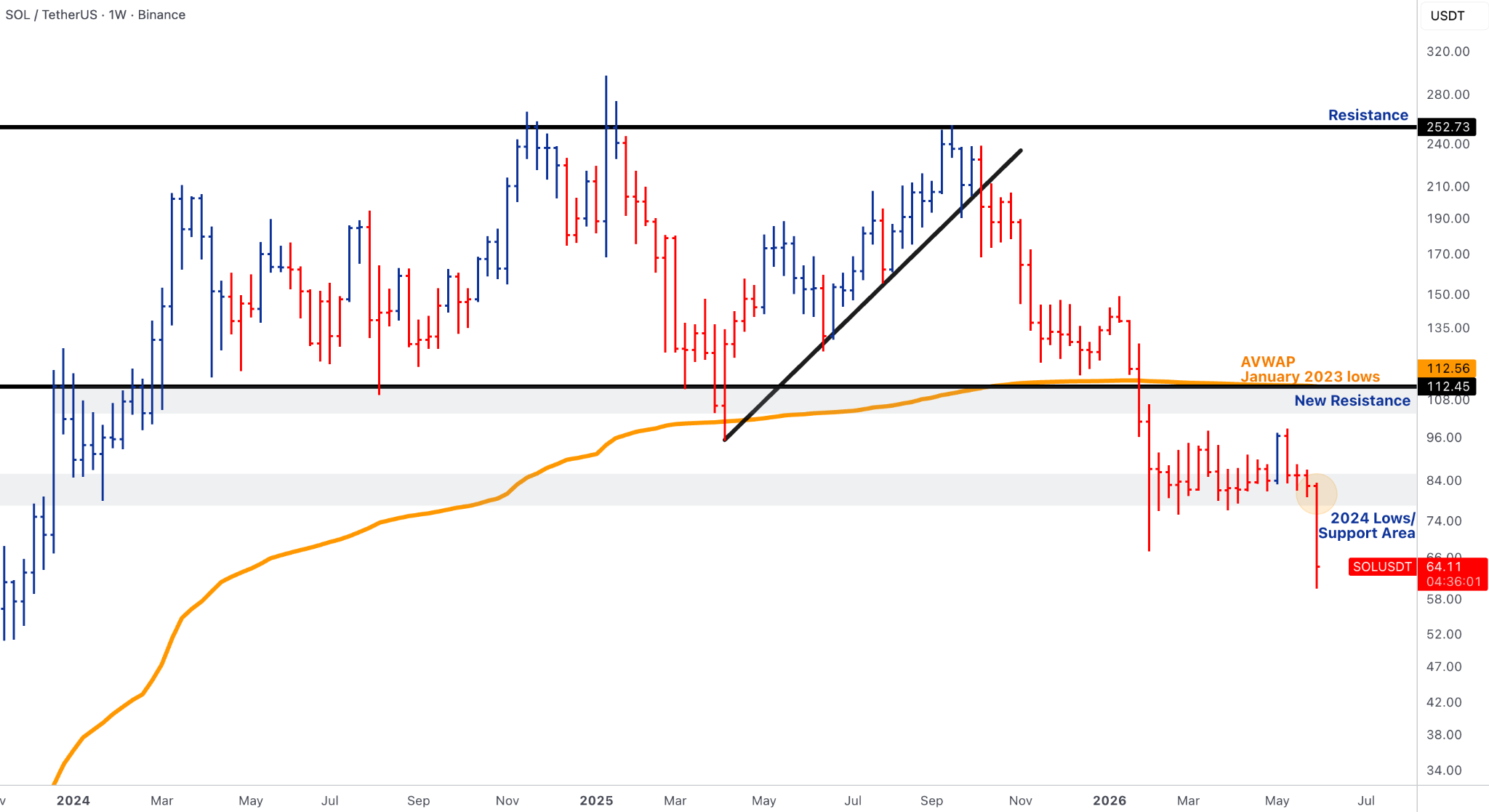

SOL & BNB -Productisation Without Leadership

- SOL is trading near $65, roughly 42% below the $112-$113 reclaim zone. That is too large a gap to describe SOL as leadership. Wrapper flows were flat on Monday, +$6.5M on Tuesday, -$12.8M on Wednesday, and flat again on Thursday and Friday, leaving the week marginally negative. The price structure and flow data are aligned: SOL remains liquid beta, not confirmed rotation leadership.

- BNB is trading near $594, roughly 20% below the $742 validation level. VanEck’s VBNB launch is structurally relevant because it gives investors listed exposure to BNB and reframes the asset as an ecosystem thesis linked to BNB Chain activity, stablecoin usage and exchange-linked network demand. But productisation has not yet translated into confirmed price acceptance.

Our take: SOL is not leadership while it trades this far below $112-$113. It remains one of the most liquid high-beta L1s and will respond quickly if risk appetite returns, but liquidity is not the same as leadership. The current chart says SOL remains in the damage zone, with liquidity amplifying downside rather than confirming leadership. A reclaim of $112-$113 would change the setup; below that, the signal remains weak.

BNB is the more interesting productisation story, but the same discipline applies. VBNB creates a legitimate listed-access channel and gives allocators a cleaner way to express the BNB Chain thesis. Still, price is below $742, so the note should not upgrade BNB prematurely. Sustained wrapper demand plus acceptance above $742 would move BNB from productisation to leadership. Until then, it remains a structurally improving asset without full technical confirmation.

Alpha Cluster - Identity Outperforms, Breadth Does Not

- The top-performer screen was highly speculative, but one theme emerged: proof-of-humanity and AI identity. WLD is the strongest expressions because the theme connects directly to AI-era identity, bot mitigation, sybil resistance and digital trust. WLD is trading near $0.47, showing high-beta sensitivity to the identity narrative rather than broad market strength.

- The catalyst stack is now cleaner: Arthur Hayes publicly backed the token after rotating out of HYPE, citing Elon Musk optionality and proximity to the upcoming IPO cycle for major AI companies. That combination — credible institutional backer, AI equity narrative adjacency, and an identifiable supply event — makes WLD the cleaner single-asset alpha expression.

- WLD also has a clearer supply catalyst. Its daily unlock rate is scheduled to fall by roughly 43% on 24 July, from approximately 5.1M WLD/day to 2.9M WLD/day.

Our take: The alpha message remains narrow and AI-anchored rather than broad. WLD is the clearest expression: institutional backing, a hard supply catalyst and direct AI identity narrative — outperforming while large-cap beta is breaking. The risk is front-running ahead of July 24; the three weeks before the unlock will be the real signal.

The Ways and Means hearing is not a near-term price trigger, but the legislative direction matters structurally. De minimis relief, staking deferral and wash sale clarity together address the three main frictions holding back domestic retail participation. That complements the institutional infrastructure build happening at the product layer and reinforces the medium-term structural thesis even as spot beta remains under pressure.

Rails, Regulation & Institutionalisation - Plumbing Advances Beneath Broken Beta

- Institutional crypto plumbing continued to advance beneath weak spot beta. The most important market-structure development was the opening of U.S. regulated perpetual futures, with Coinbase and Kalshi bringing a historically offshore product category into the domestic regulatory perimeter. That shift immediately pressured traditional exchange operators and triggered public pushback from CME CEO Terry Duffy, who warned about leverage, liquidation mechanics and systemic-risk concerns.

- CME also expanded the regulated crypto risk stack with Bitcoin Volatility futures, while Nasdaq CME Crypto Index futures are scheduled to launch on 8 June, offering market-cap-weighted exposure to a basket including BTC, ETH, SOL, XRP, ADA, LINK and XLM. Productisation broadened through VBNB for BNB exposure and continued HYPE wrapper demand, where listed access is tied to one of the few on-chain venues with visible derivatives usage.

- Tokenisation also accelerated. DTCC’s planned Stellar integration targets DTC-tokenised assets in the first half of 2027, while major U.S. banks are working through The Clearing House on a tokenised deposit network aimed at 24/7 bank-controlled settlement. Aave Labs’ Push subsidiaries secured U.K. FCA cryptoasset registration, supporting regulated fiat-to-stablecoin on/off-ramping. Kraken and Bybit also pushed tokenised IPO access into focus through SpaceX-related xStocks access, though these products provide price exposure rather than direct shareholder ownership or voting rights.

Our take: Rails are improving, but rails are not spot demand. That is the central discipline this week. Regulated perps, CME volatility futures, crypto index futures, BNB/HYPE wrappers, tokenised IPO access, DTCC/Stellar and bank-led tokenised deposits all point to a market structure becoming more institutional, more regulated and more productised. But the same developments also introduce unresolved issues around leverage, reference pricing, custody, legal ownership, investor rights and jurisdictional consistency.

The price action is what keeps the note cautious. If rails were translating into broad spot demand, BTC would not be trading near $61.9k with the $79k-$80k repair band still distant, ETH would not be stuck below $2,350-$2,400, and SOL/BNB would not remain below their validation levels. HYPE remains the cleanest listed-product story because wrapper demand is tied to a live protocol with real derivatives utility. BNB productisation is structurally relevant but still needs sustained flow and price confirmation. The right conclusion is balanced: institutional rails strengthened materially, but they did not repair ETF outflows, weak breadth or broken large-cap technicals.

Outlook - CPI, Flows and the Reclaim Test

- The coming week is an inflation-to-Fed transmission test. May CPI is scheduled for 10 June, May PPI follows on 11 June, and the June FOMC is scheduled for 16-17 June. With the Fed in blackout, markets will need to price the CPI/PPI sequence directly through Treasury yields, the dollar and rate expectations rather than through speaker guidance.

- Crypto-specific catalysts are also dense. Nasdaq CME Crypto Index futures are scheduled to launch on 8 June, the House Ways and Means Committee holds its digital asset taxation hearing on 9 June, and the market will get a fuller read on regulated U.S. perps, CME Bitcoin Volatility futures and newly launched alt-linked wrappers. Flow confirmation remains the main signal: BTC and ETH ETF outflows need to slow, HYPE listed-product demand needs to remain resilient, and SOL/BNB wrappers need evidence of genuine allocator follow-through.

- The technical map is explicit. BTC needs $79k-$80k to repair. ETH needs $2,350-$2,400. ETH/BTC needs to hold and build above 0.0250. TOTAL3 needs $776B to signal breadth repair. BTC dominance needs to remain below ~60.5% and translate into actual alt breadth, not just passive BTC underperformance. SOL needs $112-$113. BNB needs acceptance above $742. Until those levels are reclaimed, the market remains below confirmation. If CPI softens and crypto still fails to reclaim, that would be a negative signal, because it would suggest the constraint is no longer macro alone but internal demand weakness.

Our take: The burden of proof remains on the bulls because current price is still far below the levels that matter. A softer CPI/PPI sequence can generate tactical relief, especially after the intensity of the latest de-risking, but the market cannot be upgraded on macro relief alone. The repair must be visible in ETF flows, breadth and price acceptance. Without those confirmations, rallies should be treated as positioning resets rather than durable allocation turns.

A hot inflation sequence would validate the rates-hostile regime, keep real-yield pressure on BTC and ETH, and reduce the probability that productisation alone can offset spot demand weakness. The constructive path is conditional: inflation softens, Treasury yields stabilise, AI equities stop de-risking, BTC/ETH ETF outflows slow, and the market reclaims the key technical levels. Until then, the conclusion is deliberately simple: below the reclaim, there is no regime shift.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets