Access expands, breadth still lags

Blueprint - Repair without breadth

- BTC dominance is pushing the top of its two-month range and probing the 60.0-60.5% resistance band on the weekly chart, while TOTAL3 is still holding above the April 2025 lows but remains below the main $776B repair shelf.

- BTC/ES has bounced from major relative support, but it is still below the 12.41 pivot, so crypto’s rebound versus equities is improving rather than fully confirmed.

- Macro stress has eased from the worst of the war panic, but it has not disappeared: commercial traffic through the Strait of Hormuz effectively halted again over the weekend, while U.S.-Iran talks via Pakistan remain uncertain.

Our take: The market is in a better place than it was two weeks ago, but this is still a selective repair regime, not a clean broad-alt breakout. BTC is benefitting from improving access, better ETF demand, and a macro setup that is no longer relentlessly worsening; by contrast, alt breadth still lacks confirmation while BTC.D sits near the upper end of its range and TOTAL3 remains below its principal recovery threshold. The correct framework remains BTC-led stabilization with catalyst-backed pockets of alpha, not generalized beta chasing.

BTC - Flows are finally matching the access story

- U.S. spot BTC ETFs printed +$996.5M for the week, with Friday alone at +$663.9M.

- Charles Schwab said it will launch spot crypto trading in the coming weeks, widening direct BTC/ETH access for traditional brokerage clients.

- Goldman Sachs also filed for its first bitcoin ETF product, underscoring that the wrapper stack around BTC continues to deepen even in a volatile macro backdrop.

- On the chart, BTC has reclaimed the lower resistance shelf in the mid-70s, but the heavier AVWAP cluster still sits materially higher in the mid-to-high 80s.

Our take: BTC’s rebound is more credible because it is now being carried by both price repair and genuine distribution progress. ETF demand improved materially through the week, while the Schwab and Goldman developments confirm that traditional access channels are still broadening rather than pausing. That said, this remains a recovery trade until BTC can convert the reclaimed mid-70s area into support and start forcing acceptance into the 86-88k AVWAP cluster; without that, the move is still vulnerable to macro reversal rather than yet being a clean trend resumption.

ETH - Treasury absorption is constructive, but leadership still needs proof

- U.S. spot ETH ETFs printed +$275.9M on the week, with Friday at +$127.4M.

- Bitmine said its ETH treasury reached 4.87M ETH, or about 4% of supply, with total crypto and cash holdings of $11.8B.

- The Ethereum Foundation launched a $1M audit subsidy program to help builders access more than 20 audit firms.

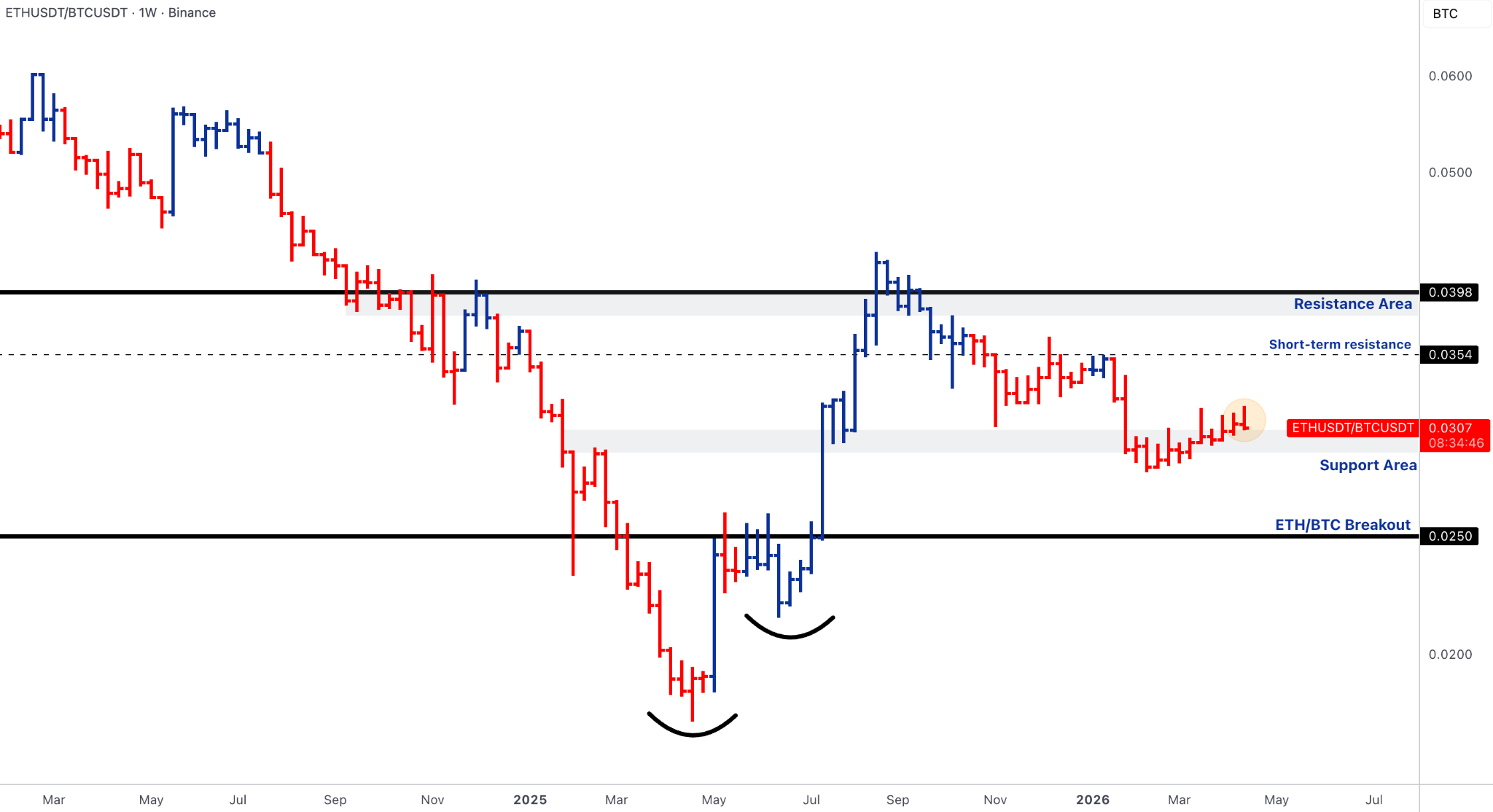

- On the chart, ETH is testing the June 2022 low AVWAP area around $2.36k, while ETH/BTC is rebounding from support but remains below the key 0.0354 decision band.

Our take: ETH is improving through a better quality mix of demand than a generic reflex bounce. Treasury accumulation on this scale matters because it creates a meaningful balance-sheet bid under a still-fragile market, while the audit subsidy initiative reinforces that the ecosystem is spending on security and deployment quality rather than just marketing a rebound. But ETH still needs technical confirmation: until spot convincingly reclaims the $2.36k AVWAP zone and ETH/BTC pushes through 0.0354, ETH is participating in recovery, not yet dictating leadership.

SOL & BNB - Constructive undercurrents, incomplete repair

- Spot SOL wrappers printed +$35.1M on the week.

- Wrapped XRP launched on Solana, opening a new route for XRP holders into Solana-native DeFi.

- On the chart, SOL remains below the $106-113 repair band and the January 2023 AVWAP area, while BNB is still trapped below the prior $742 breakout shelf despite holding above broader support.

Our take: SOL continues to show better structural undercurrents than the raw chart alone suggests: flows are positive, and the chain is still broadening its asset-capture and composability story. Even so, the market has not repaired enough to justify declaring renewed leadership while price remains below the $106-113 reclaim zone. BNB looks even more obviously like repair rather than leadership; until it starts closing back above $742, it reads as exchange-beta stabilization inside a damaged higher-timeframe structure, not the spearhead of the next leg.

Alpha Cluster - Catalyst-backed leadership, not generic beta

- HYPE: 21Shares filed a second amended S-1 for a Hyperliquid ETF expected to list on Nasdaq under THYP.

- AVAX: Bitwise launched the BAVA spot Avalanche ETP/ETF and said it intends to stake roughly 70% of the AVAX held, with a 30% liquidity reserve.

- WLD: World rolled out a major World ID upgrade tied to Tinder, Zoom, and ticketing / anti-bot functionality, shifting the story back toward product adoption rather than pure token mechanics.

- ONDO: Ondo is seeking SEC no-action relief / clearance for an Ethereum-based tokenized-equities model.

Our take: This remains a market where catalyst quality matters more than leaderboard position. HYPE, AVAX, WLD, and ONDO all map onto the strongest live themes in crypto right now - wrapper expansion, tokenized capital markets, proof-of-human infrastructure, and institutional onchain distribution. With TOTAL3 still below full repair, the right posture is to own idiosyncratic catalysts linked to infrastructure and distribution, not assume the market is ready to reward indiscriminate alt exposure.

Rails & productisation - The structural bid is still in access, settlement, and data

- Hong Kong granted its first stablecoin licences to HSBC and Anchorpoint Financial, a significant step in institutionalizing regulated fiat-backed issuance in Asia.

- Circle is continuing to push native multichain USDC infrastructure, with its cross-chain stack centered on burn-and-mint transfers and unified USDC balances across supported networks.

- SIX Swiss Exchange and BME are now pushing equities market data onchain through Chainlink, extending securities data for assets worth about €2 trillion into blockchain infrastructure.

- Schwab’s direct trading rollout and Goldman’s BTC fund filing reinforce the same direction of travel: traditional finance is still widening the access layer, not retreating from it.

Our take: The durable structural bid remains in wrappers, regulated access, settlement rails, and market data, not in speculative token demand alone. What matters is that more of the stack is becoming legible to traditional allocators: stablecoin issuance is moving into supervised banking channels, equities data is being made onchain by incumbent market-infrastructure operators, and large brokerage platforms are opening direct crypto access rather than forcing investors through proxies only. That combination continues to argue that the most durable part of the cycle is being built in the financial plumbing layer first, with token performance following where adoption is easiest to scale.

Outlook - The next leg depends on consumer data, earnings guidance, and whether geopolitics relapses

- Macro: Tuesday, April 21: U.S. March retail sales is due on April 21st, and Reuters flags Kevin Warsh’s Senate panel hearing the same day as a key policy event. The market will receive the next global flash PMI round lands on April 23rd, including U.S. jobless claims that day.Finally, the April University of Michigan consumer sentiment release is due on April 24th.

- Earnings: nearly 20% of the S&P 500 is set to report, with Tesla, Boeing, Intel, and Procter & Gamble among the names most likely to move macro risk appetite and guidance-sensitive sectors.

- Geopolitics: commercial shipping through Hormuz has again deteriorated sharply, while the U.S. says it will send negotiators to Pakistan and Iran has not yet decided whether to participate.

Our take: Next week is not about a single blockbuster data point; it is about whether improving crypto-specific flows can survive a denser macro cross-current. Retail sales and the PMI complex will tell the market whether the energy shock is feeding further into demand and pricing, while Michigan sentiment will show whether inflation psychology is stabilizing or continuing to deteriorate. At the same time, earnings guidance matters because crypto is still trading in a regime where equity-risk appetite and rates volatility can overwhelm even good crypto news at the margin. If retail, PMIs, and earnings all come in “good enough” while Pakistan talks keep the Hormuz situation from worsening, BTC has room to challenge the upper-70s and extend the squeeze; if the ceasefire narrative fails and shipping stress worsens again, the market is likely to rotate back toward BTC defensiveness over broad alt participation.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets