ETF Demand Breaks as Institutional Rails Keep Building

Blueprint - Regime, Flows & Macro Context, Continued...

- ETF demand deteriorated sharply. BTC spot ETFs reversed from the prior week’s +$631.6M inflow to -$995.5M of net outflows, with weakness broadening beyond GBTC into the core allocation products: IBIT -$317.1M, FBTC -$259.0M and ARKB -$324.2M. ETH ETFs also weakened materially, posting -$255.2M across five consecutive outflow days. SOL was the exception, with +$58.2M of modest but consistent wrapper demand.

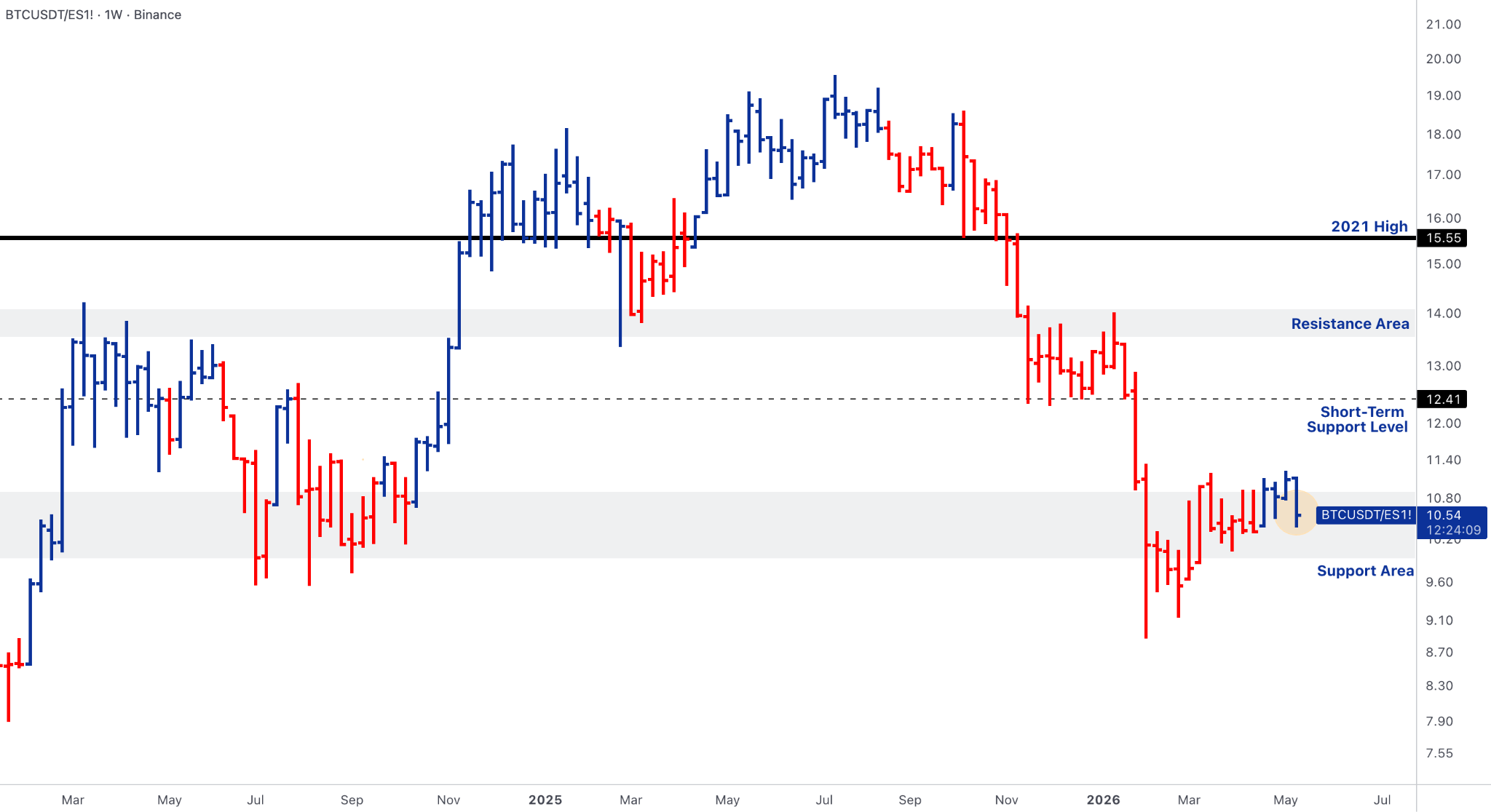

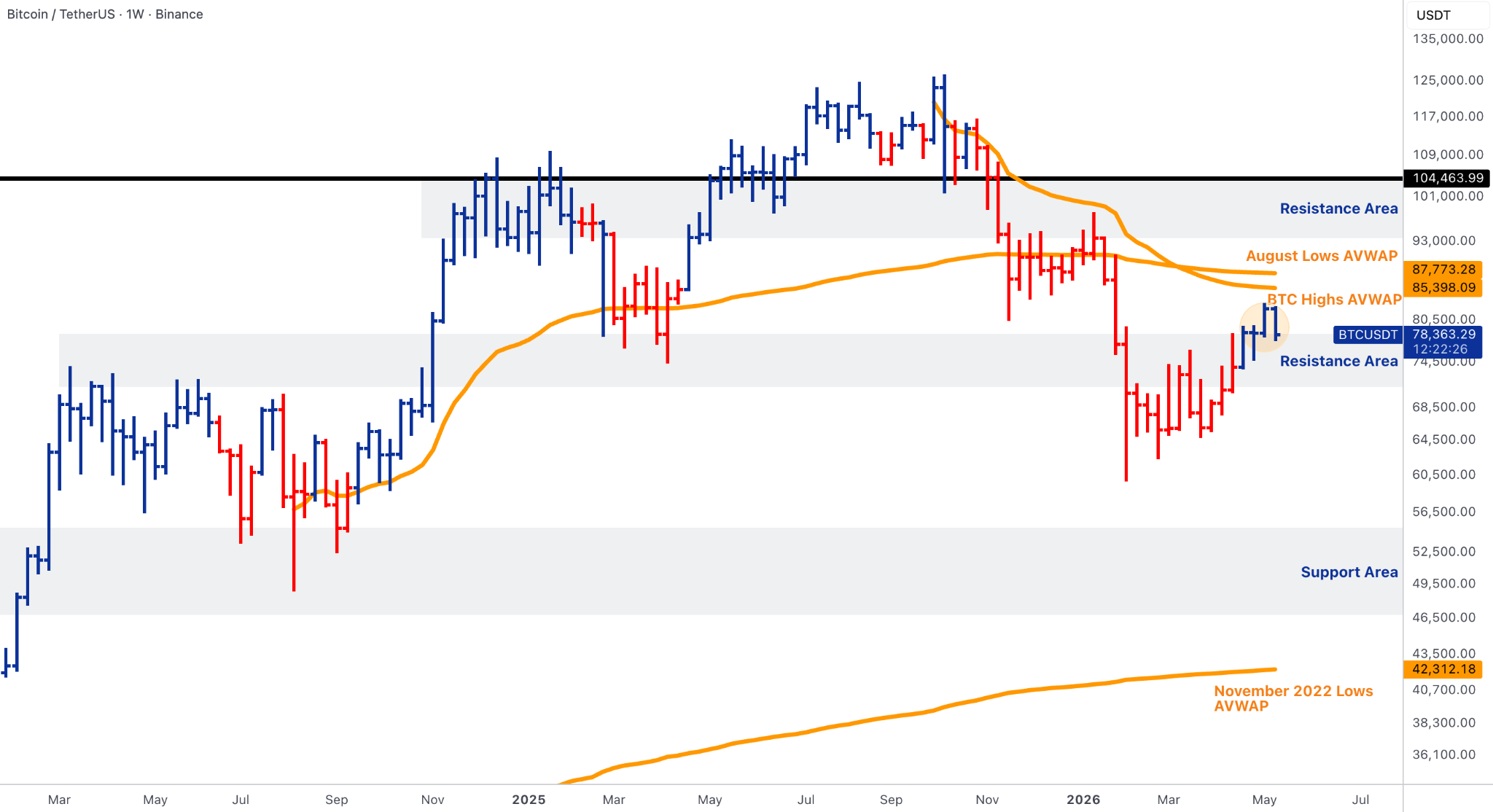

- The chart structure weakened rather than confirmed continuation. BTC failed to sustain early acceptance above $79k-$80k and slipped back toward ~$78.4k, leaving the $85.4k-$87.8k AVWAP cluster out of reach unless the trigger zone is reclaimed. TOTAL3 failed to reclaim $776B, BTC.D remained above ~60.5%, BTC/ES slipped to 10.54, and ETH/BTC deteriorated further toward 0.0280. The market is not broken, but the burden of confirmation has moved higher.

- Macro shifted from risk-supportive to rates-hostile. April CPI rose 0.6% MoM / 3.8% YoY, with energy and gasoline the primary drivers, while core CPI also firmed to 0.4% MoM / 2.8% YoY. PPI delivered the bigger shock, rising 1.4% MoM / 6.0% YoY, with gasoline up 15.6% and services also rising sharply. The combined impulse pushed the dollar and yields higher and weakened the case for near-term Fed easing.

- Equity transmission stayed fundamentally strong but macro-capped. Cisco and Applied Materials confirmed that AI infrastructure demand remains real across networking, semicap equipment and advanced packaging, while Nvidia’s surge kept AI leadership at the centre of the equity tape. But BTC/ES still fell to 10.54, confirming that strong AI equity leadership was not enough to generate crypto outperformance while ETF flows and rates moved against the asset class.

Our take: The regime has shifted from conditional continuation back to confirmation risk. BTC still has a valid repair structure if it quickly reclaims $79k-$80k, but the combination of broad ETF outflows, a failed acceptance pattern, hotter inflation, higher yields and a firmer dollar prevents a clean bullish continuation call. The important distinction is that price confirmation weakened while institutional infrastructure continued to compound. CLARITY advanced, tokenised liquidity deepened, stablecoin settlement infrastructure attracted capital, Chainlink gained share from the cross-chain security reset, and productisation expanded through Hyperliquid ETFs and CME/Nasdaq index futures. The institutional stance should therefore remain selective: cautious on broad beta, confirmation-driven on BTC, and structurally constructive on rails, tokenised cash and security infrastructure.

BTC - Failed Acceptance Raises the Bar for Continuation

- BTC spot ETFs posted -$995.5M of weekly net outflows. This was not a one-product distortion: IBIT, FBTC, ARKB, BITB and GBTC were all negative. Monday was marginally positive at +$27.2M, but the week deteriorated quickly with -$233.2M on Tuesday, -$630.4M on Wednesday and -$290.4M on Friday, only partly offset by Thursday’s +$131.3M.

- BTC failed to sustain the prior week’s early acceptance above $79k-$80k and slipped back toward ~$78.4k. That turns the prior breakout into an unresolved acceptance test rather than a confirmed continuation pattern. The next upside path remains the $85.4k-$87.8k AVWAP cluster, but that path requires a reclaim and hold of $79k-$80k first.

- Macro turned directly against the breakout attempt. CPI and PPI both confirmed broader inflation pressure, the dollar rallied, global bond yields sold off, and markets increased the probability of a future Fed hike rather than a near-term easing pivot. BTC can still benefit from a longer-term debasement narrative, but the immediate trading impulse became tighter financial conditions rather than liquidity expansion.

- Institutional ownership remains real, but the ETF tape argues that positioning is now actively managed rather than one-way accumulation. The week’s flow pattern showed de-risking across the largest products, not merely a GBTC drag or an issuer-specific anomaly.

Our take: BTC is not structurally broken, but it lost the clean continuation setup. The prior week’s case depended on price holding above $79k-$80k while ETF sponsorship rebuilt; neither condition held. Given the breadth of ETF outflows across IBIT, FBTC and ARKB, the failed $79k-$80k acceptance should be treated as institutional de-risking, not merely technical noise. The market now needs a new confirmation sequence: reclaim $79k-$80k, stabilise ETF flows, and avoid another rates/dollar shock. Without that, the $85.4k-$87.8k AVWAP cluster remains a target rather than an active magnet. BTC still deserves preference over ETH because its macro narrative and institutional access remain stronger, but the tape should not be framed as a clean BTC-led breakout while the largest ETF products are seeing broad outflows.

ETH - ETF Outflows and ETH/BTC Weakness Keep Leadership Off the Table

- ETH ETFs posted -$255.2M of net outflows across five consecutive negative sessions. The weakness was concentrated in the main institutional products, with ETHA -$184.6M and FETH -$59.9M, removing the prior stabilisation argument that ETHA could carry the complex.

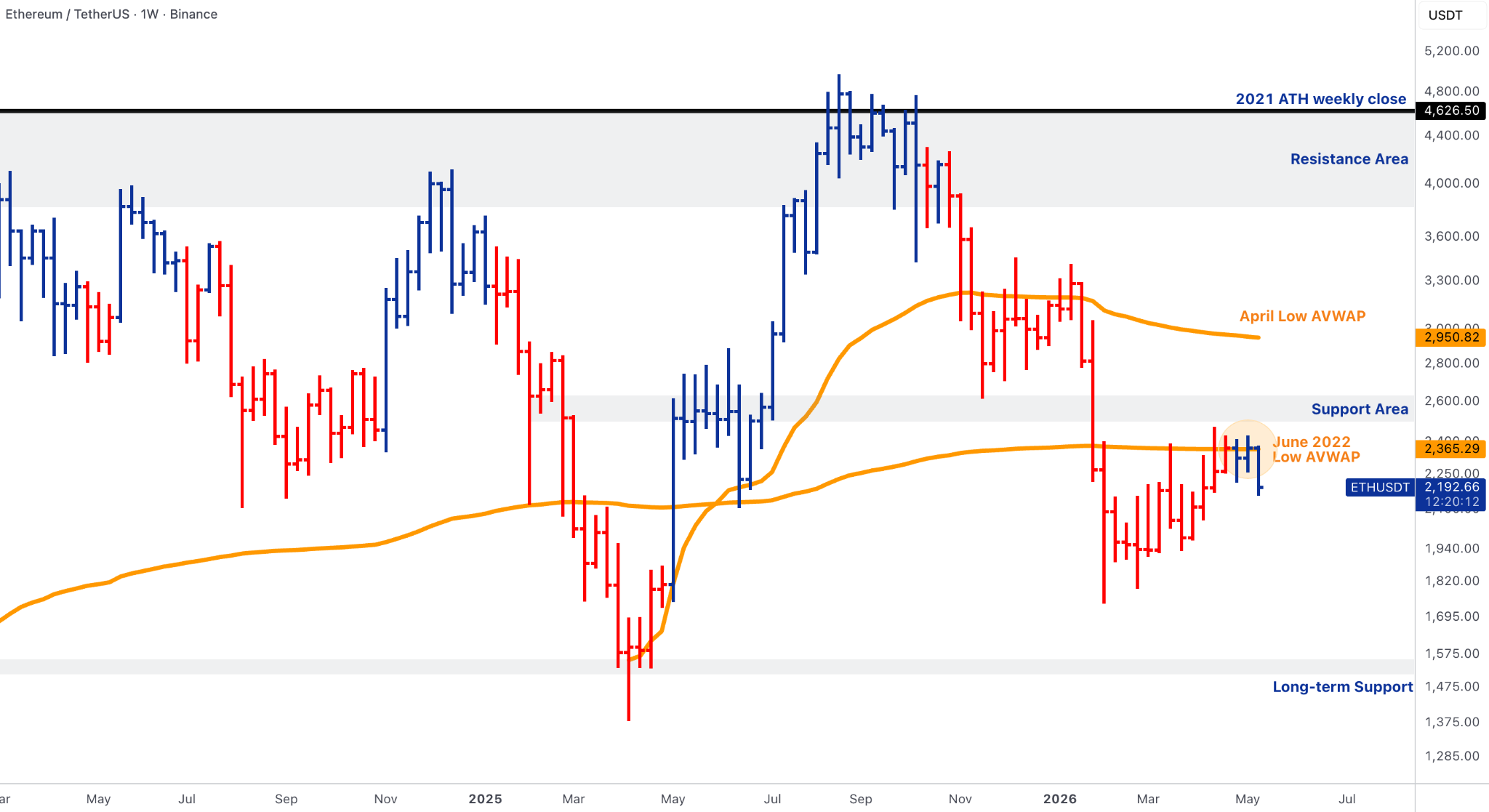

- ETH fell further below the June 2022 low AVWAP near $2,365-$2,366, trading around $2,193. The immediate reclaim remains $2,365-$2,400, followed by the stronger $2.5k-$2.6k repair band. The April low AVWAP near ~$2.95k remains well above current levels.

- ETH/BTC weakened again toward 0.0280, below the prior 0.029-0.030 support-area grind and still far below 0.0354 short-term resistance. The risk is that continued relative weakness pulls the ratio closer to the 0.0250 lower structural pivot.

- ETH’s institutional infrastructure story remains alive through tokenisation, treasury and money-market fund developments, including J.P. Morgan’s second tokenised money-market fund on Ethereum. But that is not yet translating into ETH price leadership or ETF sponsorship.

Our take: ETH remains the weakest major from a flow-adjusted and relative-strength perspective. The tokenisation story is structurally positive for Ethereum rails, but the asset itself is not yet being rewarded by ETF flows, relative price action or technical reclaim. ETH needs to regain $2,365-$2,400, then $2.5k-$2.6k, while ETH/BTC must stabilise above 0.028 and ultimately reclaim 0.0354 before any leadership language is justified. Until then, ETH should be framed as infrastructure-relevant but price-lagging.

SOL & BNB - SOL Flows Improve, Price Still Refuses to Confirm

- SOL wrappers were the only major ETF/wrapper complex with positive demand, posting +$58.2M of net inflows. The profile was clean: four positive days, no negative daily print, and demand led by BSOL +$41.4M, with additional support from FSOL +$10.4M and GSOL +$6.4M.

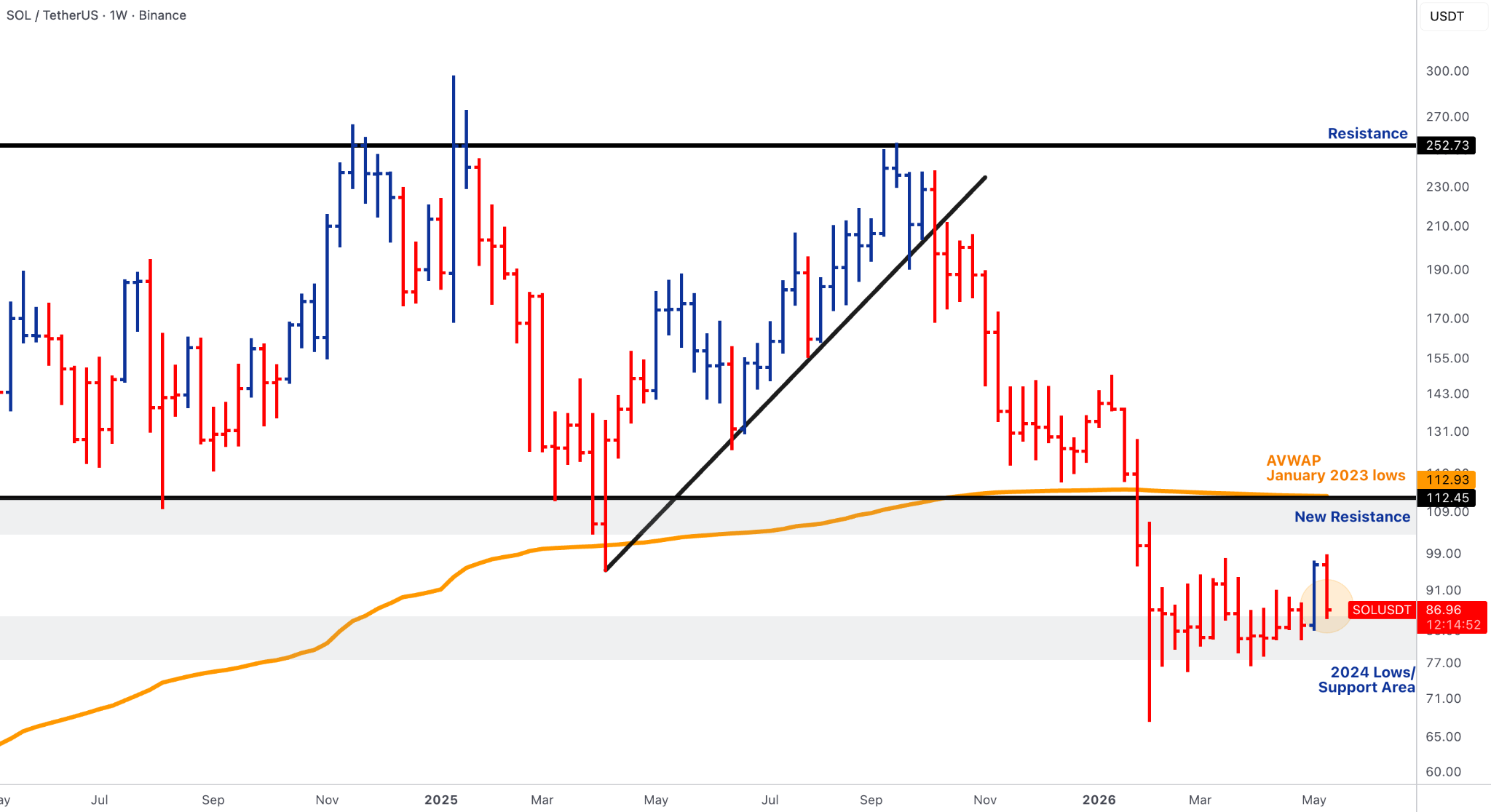

- SOL’s price action did not confirm the flow improvement. The token traded around $87, down from the prior week’s $93-$94 area, and remained trapped in the lower range below the decisive $112-$113 reclaim zone, which also aligns with the January 2023 lows AVWAP.

- BNB was more orderly, trading around $655, but still below the decisive $742 reclaim. Fresh BNB ETF amendments from VanEck and Grayscale improved the productisation narrative, but price remains below the level needed to restore a cleaner higher-timeframe structure.

- Broader major-alt breadth remained incomplete. TOTAL3 failed to reclaim $776B, BTC.D held above ~60.5%, and ETH/BTC weakened further, all arguing against broad alt beta despite pockets of wrapper demand and productisation news.

Our take: SOL had the best relative flow signal of the major-alt complex, but price did not validate it. That matters. Wrapper demand from a low base is constructive, but SOL is not a leadership asset while it remains below $112-$113. BNB has a clearer productisation catalyst through ETF filings, and its chart is more orderly than ETH or SOL, but it still needs $742. The right framing is that major-alt stabilisation remains selective and unconfirmed: flows, filings and infrastructure are improving in places, but the charts have not delivered the reclaim levels required for a broader rotation call.

Alpha Cluster - LINK, HYPE, INJ and FLR Lead Selective Infrastructure Beta

- LINK carried the strongest institutional catalyst. Chainlink CCIP gained more than $2.5B of TVL from protocols migrating away from LayerZero, with Kraken Bitcoin among the latest additions. The post-Kelp reset is turning cross-chain security, verifier architecture and institutional trust assumptions into measurable market-share drivers.

- HYPE was the clearest productisation trade. 21Shares launched U.S. Hyperliquid products, including spot HYPE exposure and a 2x long HYPE product, while Bitwise’s Hyperliquid ETF began trading on NYSE. Coinbase also became Hyperliquid’s official USDC deployer. This is not generic DeFi beta; it is the wrapping of an onchain perps venue into regulated public-market access.

- INJ’s move was supported by stablecoin-routing, Cosmos/dYdX distribution, Binance.US access and renewed buyback/burn mechanics. That gives INJ a cleaner infrastructure and exchange/settlement read-through than most mid-cap rallies.

- FLR acted as the XRPFi and interoperability sleeve. The FAssets v1.3 upgrade went live on Flare mainnet on 14 May, simplifying the process of moving native XRP into Flare and giving the rally a clearer catalyst than pure momentum.

Our take: The alpha tape is constructive only where catalysts are specific. LINK is the strongest institutional infrastructure call because the post-Kelp migration wave turns security architecture into a share-gain story. HYPE extends the productisation theme by bringing onchain derivatives exposure into regulated wrapper form. INJ is the best performer-screen inclusion, with stablecoin routing, exchange access and tokenomics all converging in the same week. FLR is a higher-beta but valid interoperability trade tied to FAssets and XRP collateral mobility. The broader message remains restrained: catalyst beta is working in pockets, but broad alt expansion is still not confirmed while BTC.D holds above ~60.5%, TOTAL3 remains below $776B, ETH/BTC continues to weaken, and SOL/BNB have not reclaimed their structural repair levels.

Rails, Regulation & Institutionalisation - Policy Advances, Tokenised Liquidity Deepens, DeFi Security Becomes Market Share

- U.S. market-structure legislation moved from aspiration to legislative process. The Senate Banking Committee advanced the CLARITY Act by a 15-9 vote, giving the digital-asset market-structure bill a major procedural win and reinforcing the shift toward defined jurisdiction across securities, commodities and crypto trading venues. The institutional caveat is implementation: the bill would push more authority toward the CFTC, so agency staffing, commissioner appointments and rulemaking capacity now matter as much as the headline vote.

- Tokenised liquidity moved deeper into bank-grade reserve infrastructure. J.P. Morgan Asset Management launched its second tokenised money-market fund on Ethereum, the JPMorgan OnChain Liquidity-Token Money Market Fund, ticker JLTXX, following its earlier MONY fund. The structure extends the tokenised cash/MMF stack toward stablecoin-reserve, treasury-management and institutional collateral use cases on a public-chain settlement layer.

- Circle’s Arc presale confirmed that stablecoin infrastructure remains a funding category even as spot ETF demand weakened. Circle raised $222M through an ARC token presale at a $3B network valuation, with participation from major institutional and crypto-native investors. Circle also reported Q1 revenue of $694M and strong USDC transaction-volume growth, reinforcing the scale of stablecoin settlement demand.

- Chainlink was the clearest beneficiary of the post-Kelp cross-chain security reset. CCIP’s migration inflows show that verifier design, cross-chain risk management and security architecture are becoming competitive market-share drivers, not just technical preferences.

- Productisation broadened beyond BTC and ETH. Hyperliquid ETFs moved onchain perps into public-market wrappers, fresh BNB ETF amendments accelerated the next-altcoin ETF race, and CME set 8 June for Nasdaq-backed crypto-index futures. The CME product is expected to be the exchange’s first market-cap weighted crypto futures contract, available in micro and larger-sized formats.

- Stablecoin regulation also remained globally unresolved. The Bank of England is reconsidering parts of its proposed stablecoin framework after industry pushback around reserve requirements and holding caps, which is a useful counterweight to the U.S. rails narrative: adoption is accelerating, but reserve design, run risk and jurisdictional divergence remain core policy constraints.

Our take: The week delivered a clear divergence between price confirmation and infrastructure progression. ETF demand deteriorated and BTC failed to hold $79k-$80k, but the institutional rails stack continued to compound: CLARITY advanced, J.P. Morgan expanded tokenised money-market infrastructure on Ethereum, Circle funded Arc as a dedicated stablecoin-settlement network, Chainlink gained share from the post-Kelp security reset, and regulated product access broadened through Hyperliquid ETFs, BNB filings and CME/Nasdaq crypto-index futures. The market is no longer just building directional BTC wrappers; it is building a fuller institutional stack across policy, tokenised cash, stablecoin settlement, cross-chain security, derivatives and index exposure.

The constraint remains risk architecture. Stablecoins still face reserve and run-risk scrutiny, DeFi still has to prove that bridge design and verifier governance are robust enough for balance-sheet-scale capital, and market-structure legislation still requires agency capacity to translate into functioning rules. The institutional framing is therefore constructive but bifurcated: infrastructure adoption is accelerating, price confirmation weakened, and permissionless risk systems remain the weakest link.

Outlook - FOMC Minutes, Nvidia and the BTC Reclaim Test

- The April FOMC minutes are the main policy event, scheduled for 20 May. They matter more than usual because the market needs to understand how divided the Fed already was before the Warsh transition and whether policymakers viewed the energy shock as temporary or as a broader inflation-risk regime.

- Nvidia is the equity-beta event of the week. Consensus expects another major AI infrastructure print, with investors focused on whether hyperscaler capex, data-centre demand and gross-margin quality can continue to support the AI equity trade while bond yields rise.

- Housing, claims and flash PMIs will test whether higher yields are starting to damage growth. Jobless claims, housing starts, building permits, the Philadelphia Fed Manufacturing Index and S&P Global flash PMIs all matter because the market needs softer rates without a growth scare. That remains a narrow landing zone for crypto.

- CLARITY shifts from milestone to negotiation risk. The committee vote is behind the market; the next question is whether the bill can survive floor negotiations, CFTC staffing constraints and renewed disputes over AML, ethics, stablecoin rewards or SEC/CFTC jurisdiction.

- Productisation remains a forward support, not immediate spot-demand confirmation. CME Bitcoin Volatility futures are planned for 1 June, while Nasdaq CME Crypto Index futures are planned for 8 June, pending regulatory review. These reinforce the medium-term institutional stack but do not replace the need for near-term ETF flow stabilisation.

- The crypto confirmation levels remain unchanged. BTC must reclaim and hold $79k–$80k to reopen the $85.4k-$87.8k AVWAP path. TOTAL3 needs $776B. BTC.D needs to lose ~60.5%. ETH needs $2,365-$2,400. ETH/BTC needs to stabilise above 0.0280 and eventually reclaim 0.0354. SOL needs $112-$113. BNB needs $742.

Our take: The next phase is a policy, equity-beta and reclaim test. A patient FOMC-minutes read would give BTC room to recover $79k-$80k, especially if Nvidia keeps the equity-risk floor intact. A hawkish minutes read, weak Nvidia reaction or continued yield/dollar pressure would keep BTC trapped below the trigger and make the failed acceptance pattern more important. The key risk is that a hawkish FOMC-minutes read and a weaker Nvidia reaction would remove both supports at once: policy patience and equity-beta cushioning. The setup is not bearish enough to abandon the repair framework, but it is not strong enough to chase broad beta. Until ETF flows stabilise, BTC reclaims $79k-$80k, and breadth confirms through TOTAL3 and BTC.D, the preferred stance remains cautious on broad risk, selective on infrastructure-led alpha, and structurally constructive on tokenised rails.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets