BTC Clears First Supply as Agentic Payments Move Into Production

Blueprint - Regime, Flows & Macro Context, Continued...

- ETF demand improved versus the prior week, but the recovery was still uneven. BTC spot ETFs posted +$631.6M of weekly net inflows, materially above the prior week’s +$162.8M, but the structure was front-loaded: Monday and Tuesday contributed +$999.6M, Wednesday slowed to +$46.2M, and Thursday/Friday gave back -$414.2M. ETH ETFs flipped back to a modest +$70.3M, while SOL wrappers improved to +$39.2M from an almost absent base.

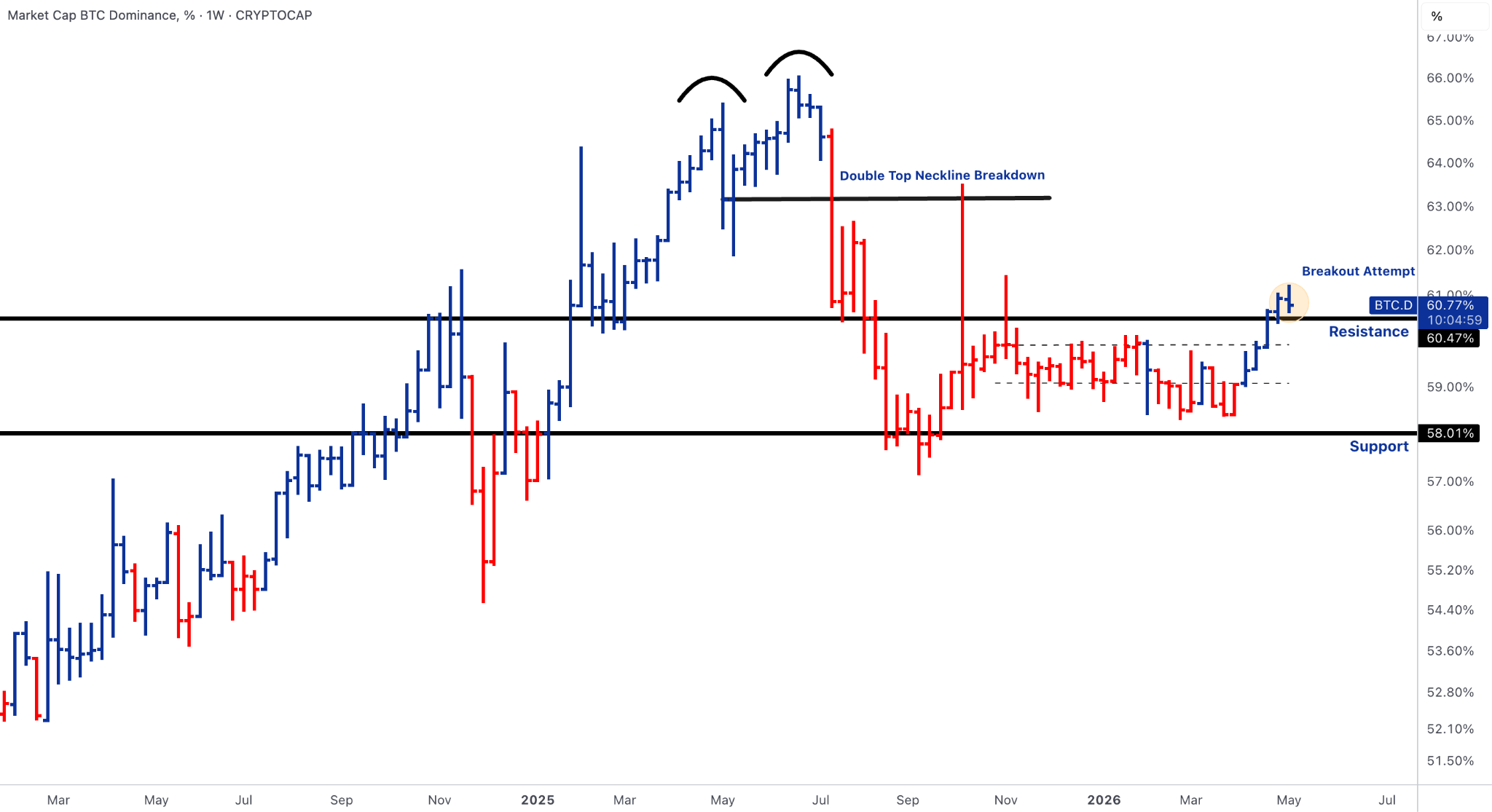

- Price structure improved, but leadership remains narrow. BTC delivered the cleanest upgrade by pushing above the $79k-$80k trigger zone and now sits near $81k, shifting focus toward the $85.5k-$87.8k AVWAP cluster. TOTAL3 improved to roughly $765B, close to the $776B breadth reclaim, while SOL and BNB stabilised better from low ranges. The constraint is that BTC.D still holds above ~60.5%, ETH/BTC weakened toward 0.0288, and ETH remains below the June 2022 AVWAP.

- Macro was risk-supportive but not liquidity-easy. April payrolls rose 115k, unemployment held at 4.3%, participation was little changed at 61.8%, and average hourly earnings rose 0.2% MoM / 3.6% YoY. The labour report was firm enough to avoid a growth scare, but the rise in part-time-for-economic-reasons employment to 4.9M kept the labour-quality read mixed.

- The inflation constraint did not clear. ISM Services stayed expansionary at 53.6, but the Prices Index held at 70.7, matching the highest reading since October 2022, while Michigan sentiment fell to a record-low 48.2 as gasoline pressure continued to weigh on households.

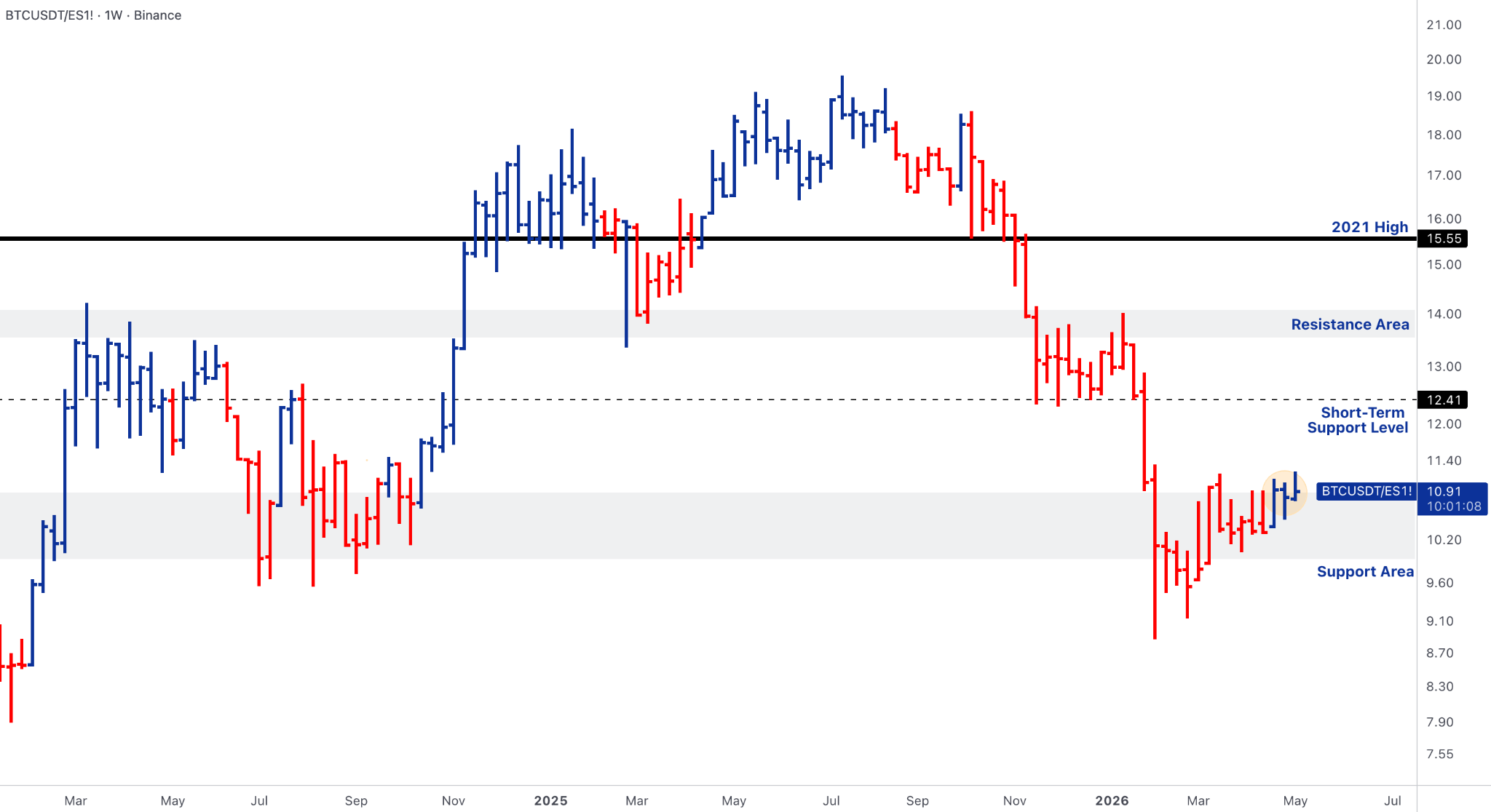

- Equity transmission remained supportive but selective. AMD’s Data Center revenue rose 57% YoY to $5.8B, Palantir reported a $1.63B quarter, and Arista posted $2.709B of revenue, up 35.1% YoY, confirming that AI infrastructure and software demand remain fundable where revenue conversion is visible. BTC/ES improved only marginally to around 10.91, still below the 12.41 reclaim, so equities provided a risk floor without confirming crypto outperformance.

Our take: The market has upgraded from defensive repair to conditional continuation. BTC now has the cleanest combination of flow recovery, technical improvement and macro relevance: ETF demand rebounded, price cleared the first major supply zone, and the fiscal/inflation hedge argument remains live while labour data avoids a growth scare. The improvement is not broad enough to call a potential alt regime. TOTAL3 is close to reclaim, but BTC dominance has not broken down, ETH/BTC remains heavy, and SOL/BNB are still below their structural repair levels. The right institutional stance is constructive on BTC above $79k-$80k, selective on catalyst-led alts, and still confirmation-driven before upgrading the broader crypto beta complex.

BTC - Initial Breakout Holds, AVWAP Cluster Becomes the Next Test

- BTC spot ETFs recovered to +$631.6M of weekly net inflows. The week began strongly, with +$532.3M on Monday and +$467.3M on Tuesday, before flows slowed on Wednesday and turned negative on Thursday and Friday. IBIT contributed +$596.3M, meaning the weekly net remained heavily BlackRock-led rather than a broad all-issuer chase.

- BTC moved above the $79k-$80k trigger zone and is trading around $81k. This is a meaningful improvement from the prior week’s resistance test. The next major technical magnet is the AVWAP cluster: BTC highs AVWAP around $85.5k and August lows AVWAP around $87.8k. The larger structural ceiling remains near $104.5k.

- The newsflow supports BTC’s improved positioning but also argues against complacency. ETF momentum was strong early in the week, but profit-taking warnings increased as BTC approached the $85k-$88k resistance area. Macro framing also remained BTC-friendly on a relative basis: oil-driven inflation, fiscal supply and delayed Fed easing all strengthen BTC’s hedge/debasement narrative more directly than they support ETH or SOL.

- Treasury supply did not create an immediate rates accident, but the medium-term borrowing path keeps the fiscal-supply theme alive. Treasury expects to borrow $189B in privately held net marketable debt in Q2, $79B above the February estimate, and $671B in Q3.

Our take: BTC has moved from “testing supply” to “early acceptance above first resistance.” That is the most important regime upgrade of the week. The caveat is flow quality: a front-loaded ETF week followed by late outflows is not the same as persistent institutional chase, and IBIT concentration still means the bid is not fully diversified. The late-week ETF outflows prevent the move from being treated as a clean chase; the breakout needs renewed flow confirmation as price approaches the AVWAP cluster. As long as BTC holds $79k-$80k, the path toward $85.5k-$87.8k is open. A loss of that zone would turn the breakout into a failed acceptance pattern and put the market back into range-repair mode.

ETH - Flow Stabilises, Relative Structure Deteriorates

- ETH ETFs improved from the prior week’s negative print to +$70.3M, but the quality remained fragile. Monday and Tuesday were constructive, Wednesday was marginally positive, Thursday saw a -$103.6M outflow, and Friday was only slightly positive. ETHA carried the weekly result, while FETH remained a drag.

- ETH is still below the June 2022 low AVWAP near $2,365-$2,366, trading around $2,329. The immediate reclaim remains $2,365-$2,400, followed by the stronger $2.5k-$2.6k repair band. The April low AVWAP near $2,957 remains a larger structural hurdle.

- ETH/BTC weakened further toward 0.0288, below the prior support-area grind and far below 0.0354 short-term resistance. This is the clearest argument against ETH leadership. ETH is not simply lagging less; it is still losing relative ground despite the broader BTC-led recovery.

- ETH-related treasury and protocol narratives remain supportive at the margin, but they are not driving relative performance. The market continues to reward BTC’s flow/macro setup more clearly than ETH’s staking, treasury and infrastructure story.

Our take: ETH can be upgraded from negative to tentatively stabilising, but not to leadership. The ETF flow improvement matters, yet the chart has not confirmed: ETH remains below the June 2022 AVWAP and ETH/BTC is weakening. The asset needs a clean reclaim of $2,365-$2,400, then $2.5k-$2.6k, with ETH/BTC recovering toward 0.0354 before it can be treated as more than a secondary repair trade. Until then, ETH remains structurally behind BTC in both flows and relative price action.

SOL & BNB - Better Stabilisation, Still Below Repair Levels

- SOL wrapper demand reappeared after the prior week’s near-absence, with +$39.2M of net inflows. The absolute figure is small versus BTC and ETH, but the profile was cleaner: every day finished positive, with BSOL driving most of the allocation.

- SOL’s price action improved to around $93.7, but it remains below the decisive $112-$113 reclaim zone, which also aligns with the January 2023 lows AVWAP. The current range has improved from the low-$80s, but the chart is not structurally repaired until that reclaim is cleared.

- BNB also improved, trading around $651, and continues to show a more orderly range recovery than SOL. The decisive reclaim remains $742, the broken prior resistance / breakout level. Until that area is recovered, BNB is still in a stabilisation phase rather than restored leadership.

- Solana-adjacent rails news remained active, including stablecoin, payments and application-layer developments. However, token-level confirmation still rests on price reclaim and sustained wrapper demand, not on application headlines alone

Our take: SOL and BNB moved in the right direction, but neither has earned a leadership upgrade. SOL flows improved from a low base and the chart is bouncing, yet $112-$113 remains the level that determines whether the move is structural or tactical. BNB is cleaner in range terms but still needs $742. The section should therefore remain constructive but restrained: major-alt stabilisation is improving, but BTC remains the centre of gravity until SOL, BNB, TOTAL3 and BTC.D all confirm broader rotation.

Alpha Cluster - TON, ZEC and VVV Lead Selective Catalyst Beta

- TON was the cleanest large-cap alpha leader, gaining more than 80% on the weekly performance screen after Telegram moved back into a direct leadership role around The Open Network. Pavel Durov said Telegram would replace the TON Foundation as the main driving force behind TON and become its largest validator, tightening the link between the network and Telegram’s consumer-distribution layer.

- ZEC remained one of the strongest privacy/productisation trades. Grayscale Zcash Trust average daily volume rose to roughly $1.7M in April, more than double the prior month, while the Orchard shielded pool grew from 1.92M ZEC to 4.55M ZEC over the past year, leaving close to 30% of circulating supply in shielded balances.

- VVV added the AI-application and tokenomics sleeve. Venice Token’s setup fits the same selective AI-beta framework seen in equities: investors continued to fund AI infrastructure and software exposure where usage and monetisation were visible. The tokenomics narrative is also cleaner than most AI microcaps, with annual emissions reduced to 6M VVV in February and a buy-and-burn programme tied to platform revenue.

Our take: The alpha tape is healthier than it was, but it remains selective. TON is the strongest large-cap expression because Telegram’s validator and roadmap shift gives it a real distribution channel and consumer-payments angle. ZEC is the cleaner institutional narrative trade, supported by privacy usage, Grayscale trust activity and shielded-supply growth. VVV is the higher-beta AI application sleeve, helped by a stronger tokenomics story and continued demand for AI-linked crypto exposure. The broader message remains disciplined: individual catalysts are working, but broad alt expansion still requires BTC.D to lose ~60.5%, TOTAL3 to reclaim $776B, and ETH/BTC to stabilise.

Rails, Regulation & Institutionalisation - Agentic Payments, Tokenised Settlement and Federal Infrastructure

- Stablecoin rails moved deeper into AI and cloud infrastructure. AWS launched Amazon Bedrock AgentCore Payments in preview, built with Coinbase and Stripe, enabling AI agents to autonomously access and pay for APIs, MCP servers, web content and other agents, while handling wallet authentication, transaction execution, spending governance and observability. The stack also connects Coinbase CDP wallets or Stripe Privy wallets into the payment flow, with support for x402-style autonomous settlement.

- Tokenised settlement advanced in Europe and the U.S. The Bank of Italy said the EU should consider tokenised SEPA payments as payments infrastructure evolves toward speed, programmability and new forms of settlement. DTCC also advanced its tokenisation service, with limited production trades of tokenised real-world assets planned for July and a broader service launch targeted for October, supported by an industry working group that includes BlackRock, Circle and more than 50 firms.

- Regulated custody and market-structure infrastructure continued to move toward federal channels. Kraken parent Payward filed for an OCC national trust company charter, which would establish a federally regulated custody offering under OCC oversight for institutional clients requiring a qualified custodian. The Senate Banking Committee also set a 14 May executive session to consider the CLARITY Act, which would clarify how digital assets are treated across securities, commodities and other regulatory categories.

- Productisation deepened across derivatives. CME’s new AVAX and SUI futures are now trading, with first block trades executed between FalconX and G-20 Group. CME also plans to launch Bitcoin Volatility futures on 1 June, pending regulatory review, giving institutions a listed instrument to express or hedge BTC volatility directly rather than only spot direction.

- DeFi risk remains the institutional constraint. KelpDAO’s move from LayerZero to Chainlink after the rsETH exploit turns the incident into a case study in verifier architecture, cross-chain assumptions, recovery governance and legal-claim hierarchy. The investment implication is not simply that DeFi remains risky; it is that institutional DeFi underwriting is becoming more granular around oracle selection, bridge design and emergency-response mechanics.

Our take: The institutionalisation story is now less about “crypto adoption” in the abstract and more about production rails. AWS, Coinbase and Stripe embedding stablecoin payments into agentic workflows links USDC to cloud, AI and machine-to-machine commerce. Tokenised SEPA, DTCC’s tokenised-asset rollout, CLARITY Act progression, Payward’s OCC trust-charter application and CME’s expanding derivatives suite show that payments, settlement, custody, regulation and risk-transfer infrastructure are maturing in parallel. The offset remains permissionless DeFi: Kelp/LayerZero shows that bridge design, verifier configuration, governance response and legal-claim hierarchy are still central diligence items before open DeFi can absorb institutional balance-sheet capital.

Outlook - CPI, CLARITY Markup and the AVWAP Test

- The next macro test is labour. The April Employment Situation is scheduled for Friday, 8 May, with JOLTS, ADP and weekly claims setting up the labour-market read beforehand.

- Rates volatility remains central after the divided FOMC. Treasury’s financing estimates are scheduled for 4 May, followed by refunding/auction-schedule documents on 6 May. This matters because crypto is entering the week with BTC still below $79k-$80k acceptance and ETF demand already decelerated versus the prior week.

- AI/data-centre earnings remain the equity-beta channel. After mega-cap earnings defended the AI trade, the market will now look to Palantir, AMD, Arista and Super Micro for confirmation that AI infrastructure demand remains strong beyond the largest platforms.

- Oil and Hormuz remain the inflation-tail overlay. OPEC+ agreed a symbolic 188k bpd June quota increase, but the increase remains largely theoretical while Strait of Hormuz disruptions continue to limit Gulf exports and keep energy inflation risk elevated.

- Crypto-native productisation continues with CME’s planned AVAX and SUI futures launch on 4 May, though derivatives access should be treated as structural market development rather than immediate spot-demand confirmation.

- The key crypto levels remain unchanged. BTC needs acceptance above $79k-$80k to target $85.6k-$87.9k. ETH needs to reclaim $2,365-$2,400, then $2.5k-$2.6k. TOTAL3 needs $776B. BTC.D needs to lose 60.47%. SOL needs $112-$113. BNB needs $742.

Our take: The next phase is a macro and breadth confirmation test. If CPI is primarily energy-led and core services do not re-accelerate, BTC should have room to test the $85.5k–$87.8k AVWAP cluster while holding the $79k-$80k breakout zone. A hot core print would raise real-yield risk and make BTC acceptance more fragile, especially after ETF flows turned negative late in the week. The CLARITY Act markup adds a crypto-native catalyst that can support the rails and productisation theme, but broader market confirmation still depends on breadth: TOTAL3 needs $776B, BTC.D needs to break back below ~60.5%, and ETH/BTC must stop leaking lower. Until that happens, the preferred stance remains BTC-led, catalyst-selective and structurally constructive on rails.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets