Spot Beta Breaks as Market Structure Moves Onshore

Blueprint - Spot Beta Fractures, Institutional Rails Hold

- Large-cap ETF sponsorship deteriorated again. BTC spot ETFs lost roughly $1.416B across the shortened trading week, led by almost $1B of IBIT redemptions, while ETH ETFs lost another $241.6M and extended the persistent outflow sequence. SOL wrappers stayed barely positive at +$2.4M, while HYPE-listed products remained the clear outlier with +$55.1M of inflows.

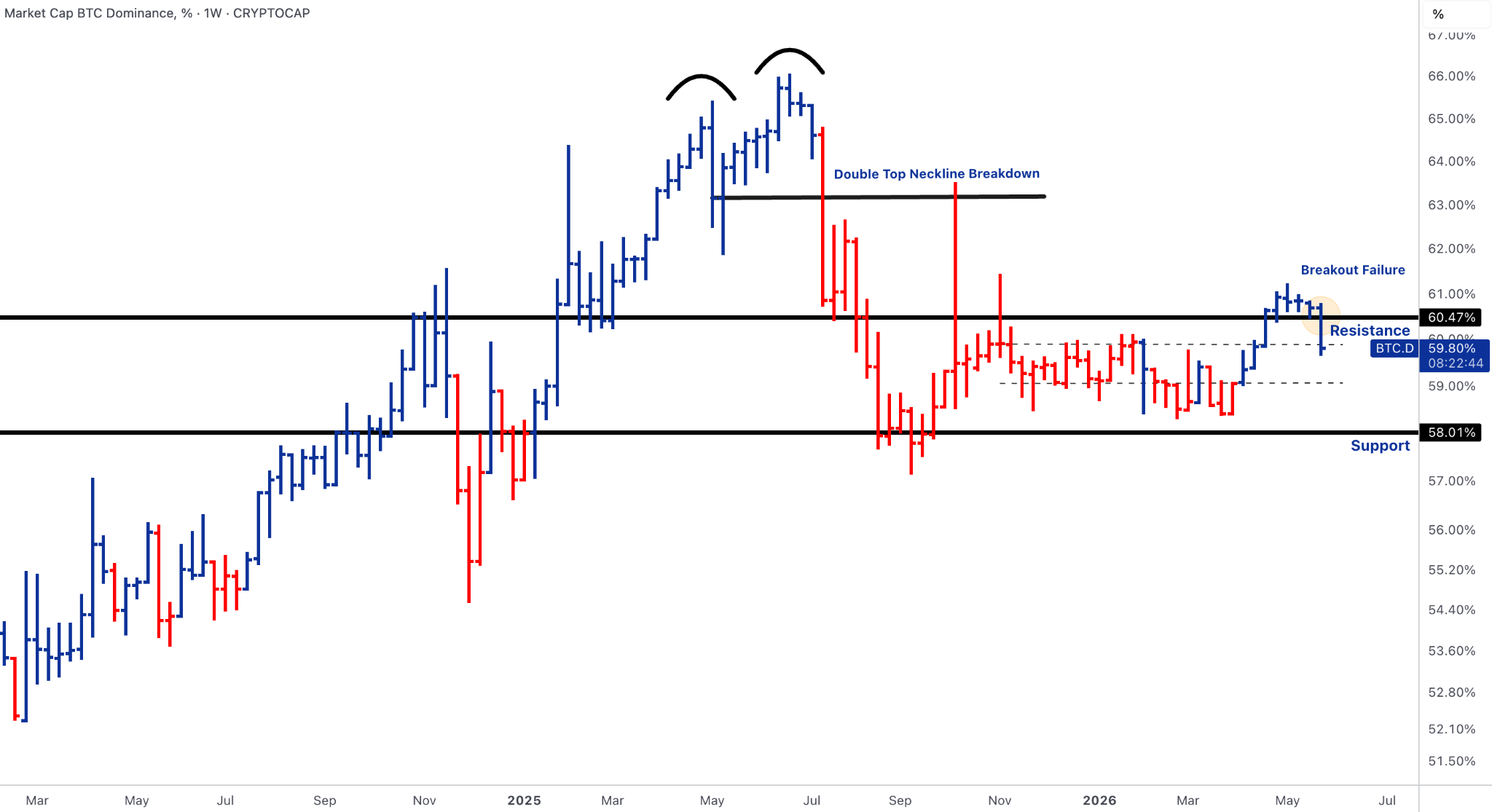

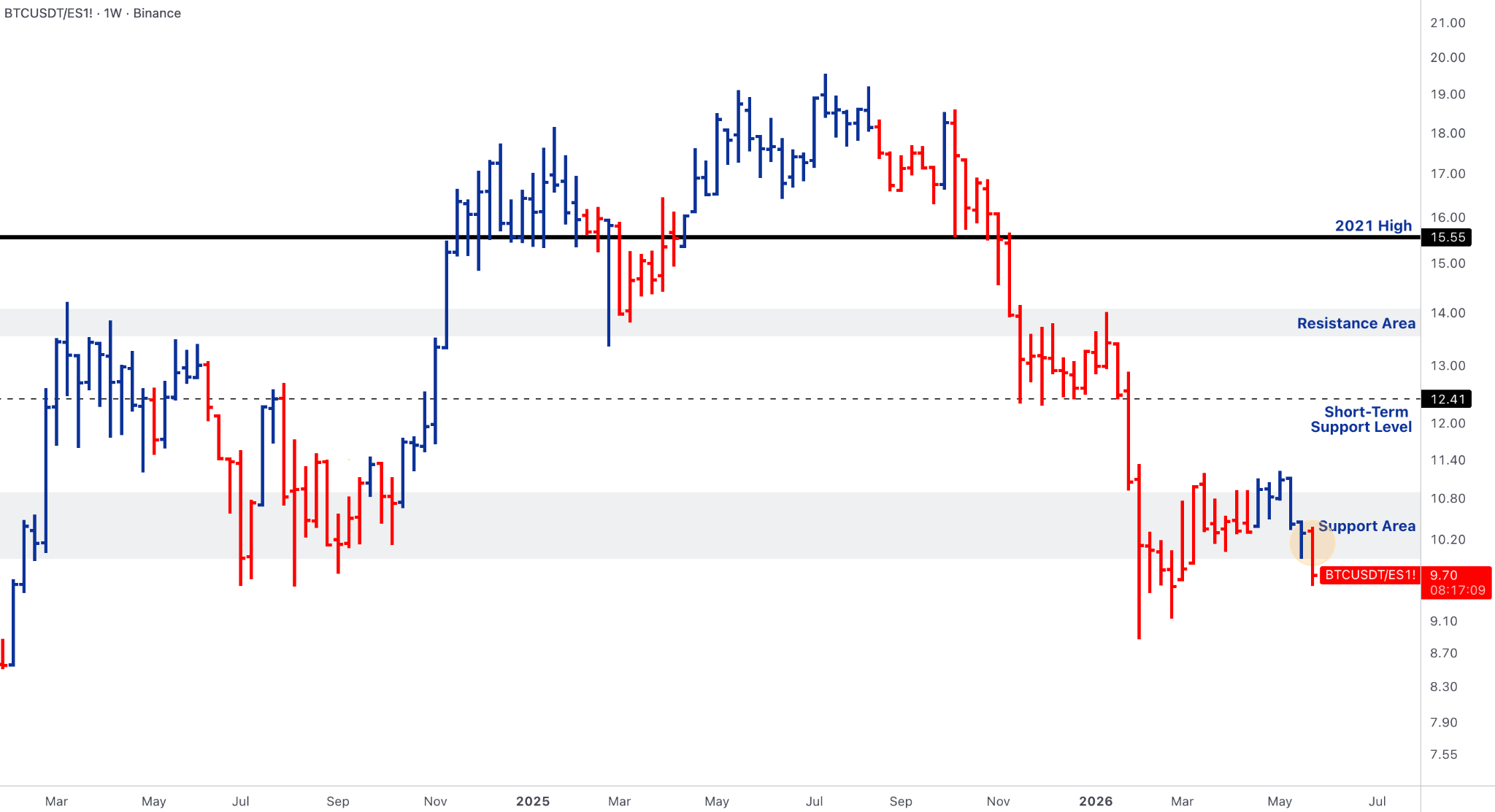

- The technical repair failed. BTC rejected the $79k-$80k band and rolled back toward $73k-$74k, ETH lost the $2,350-$2,400 recovery zone, BTC/ES broke toward 9.7, and TOTAL3 remained below the key $776B breadth-repair threshold. BTC dominance slipped back below 60.5%, but that alone is not enough to call alt rotation while TOTAL3, ETH/BTC and major-alt reclaim levels remain unconfirmed.

- Macro delivered relief at the margin, but not enough to reverse the crypto flow problem. April PCE rose 0.4% MoM / 3.8% YoY, core PCE rose 0.2% MoM / 3.3% YoY, personal income was essentially flat, disposable personal income fell 0.1%, and Q1 real GDP was revised down to 1.6%. That is not an immediate macro shock, but it is also not a clean rate-cut signal.

- Equities remained more resilient than crypto. FactSet’s latest Earnings Insight showed Q1 S&P 500 blended earnings growth at 28.6% YoY, while Goldman raised its S&P 500 year-end target to 8,000 on strong earnings and AI infrastructure momentum. The problem for crypto is that BTC/ES still deteriorated, confirming crypto-specific underperformance rather than a broad risk-off liquidation.

Our take: This was not a generic risk-off week; it was a crypto-specific beta failure inside a still-resilient equity tape. The market entered the week with a narrow window for repair, but that window closed as BTC lost acceptance above $79k-$80k, ETH rejected the June 2022 AVWAP region, ETF flows remained under active distribution, and BTC/ES confirmed that AI-led equity strength was not transmitting into crypto. The more constructive institutional story was not in spot beta, but in regulated market structure: U.S. perpetual futures, BNB’s first U.S. spot ETP, HYPE wrapper demand, DTCC/Stellar tokenised securities, BIS wholesale-tokenisation work, and stablecoin payment rails all advanced. The regime remains bifurcated: weak large-cap sponsorship, poor crypto/equity transmission, but continued institutionalisation through wrappers, rails and derivatives plumbing.

BTC - Failed Repair, ETF Distribution, Weaker Cross-Asset Transmission

- BTC failed to sustain acceptance above the $79k-$80k repair band and rolled back toward $73k-$74k, leaving the market below the first recovery zone and well below the $85.0k-$87.6k AVWAP cluster.

- BTC spot ETFs posted roughly -$1.416B of weekly outflows, with every reported session negative and the largest drawdown concentrated on 27 May at approximately -$733M. The weakness remained broad but was led by IBIT, which accounted for almost $1B of redemptions.

- BTC/ES fell toward 9.7, confirming that BTC is underperforming equities rather than simply tracking a broader risk-off move. This is one of the most important regime signals: equities are holding up, but crypto is not receiving the marginal risk dollar.

- Macro did not offset the flow problem. PCE cooled sequentially at the core level, but headline and core inflation remained too far above target to reopen an easy-policy narrative, while lower real income and slower GDP growth kept the backdrop closer to stagflationary pressure than clean disinflation.

Our take: BTC’s issue is no longer just price rejection; it is the combination of failed technical repair, persistent ETF distribution and poor cross-asset confirmation. The AI-led equity tape and easing Hormuz headlines created enough macro relief to keep equities supported, but not enough to restore BTC sponsorship. Until BTC reclaims $79k-$80k and ETF outflows slow materially, rallies should be treated as repair attempts rather than trend resumption. The higher-quality confirmation remains a move through the $85k-$87.6k AVWAP cluster, but the immediate burden of proof is now lower: BTC first needs to stabilise the failed reclaim and stop underperforming equities.

ETH - Infrastructure-Relevant, Asset Still Lagging

- ETH ETFs lost approximately $241.6M, with ETHA again the main pressure point. ETH flow sponsorship remains weaker than BTC on a persistence basis, and there is still no ETF-based case for ETH leadership.

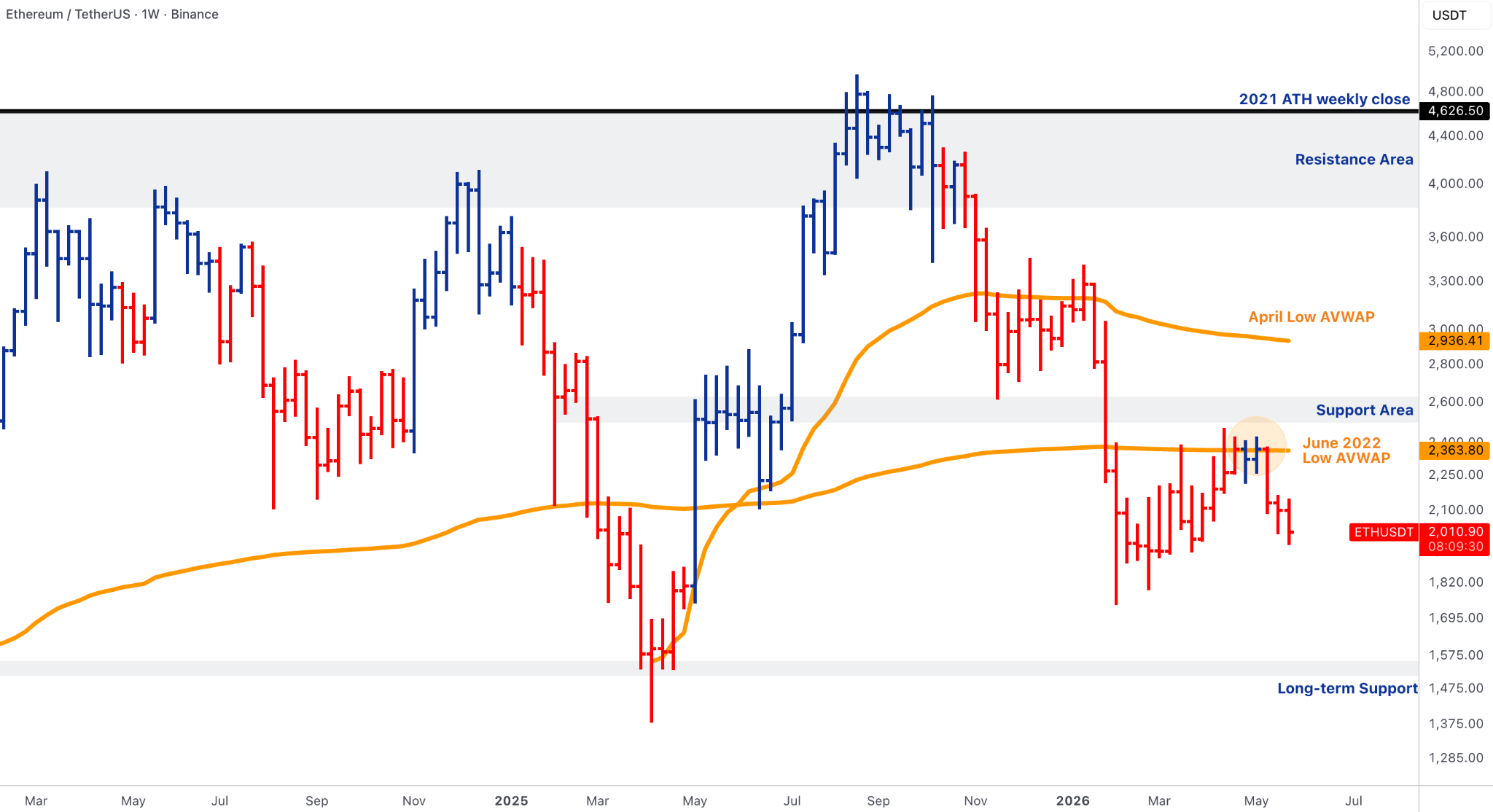

- ETH rejected the $2,350-$2,400 repair area and traded back near $2,010, keeping the chart below the June 2022 AVWAP and far below the larger $2,936 April-low AVWAP reference.

- ETH/BTC slipped toward 0.0273, above the major 0.025 structural pivot but below the short-term support band and far below 0.0354-0.0398 resistance. The pair is not broken on a long-term basis yet, but it is still leaking lower.

- Ethereum-adjacent infrastructure improved: Base’s Azul upgrade went live, Aave Labs secured UK approvals for regulated crypto/payments activity, and the Ethereum Foundation’s lower-sale optics helped sentiment at the margin. None of that has yet translated into ETH ETF demand or relative-price leadership.

Our take: Ethereum remains institutionally relevant at the infrastructure layer but price-lagging at the asset layer. The positive story is clear: Coinbase’s L2 stack is hardening, Aave is moving further into regulated payments infrastructure, and Ethereum remains central to tokenised collateral and settlement conversations. The problem is that none of this has reversed ETF outflows, ETH/BTC weakness, or spot-price rejection at the relevant repair zone. ETH needs to reclaim $2,350-$2,400 and defend 0.025 on ETH/BTC before the tone can shift from “infrastructure-relevant, price-lagging” to a genuine leadership frame.

SOL & BNB - SOL Stays Trapped, BNB Becomes the Cleaner Productisation Candidate

- SOL wrappers stayed marginally positive at roughly +$2.4M, but demand faded meaningfully from prior weeks and remains too small to support a leadership claim.

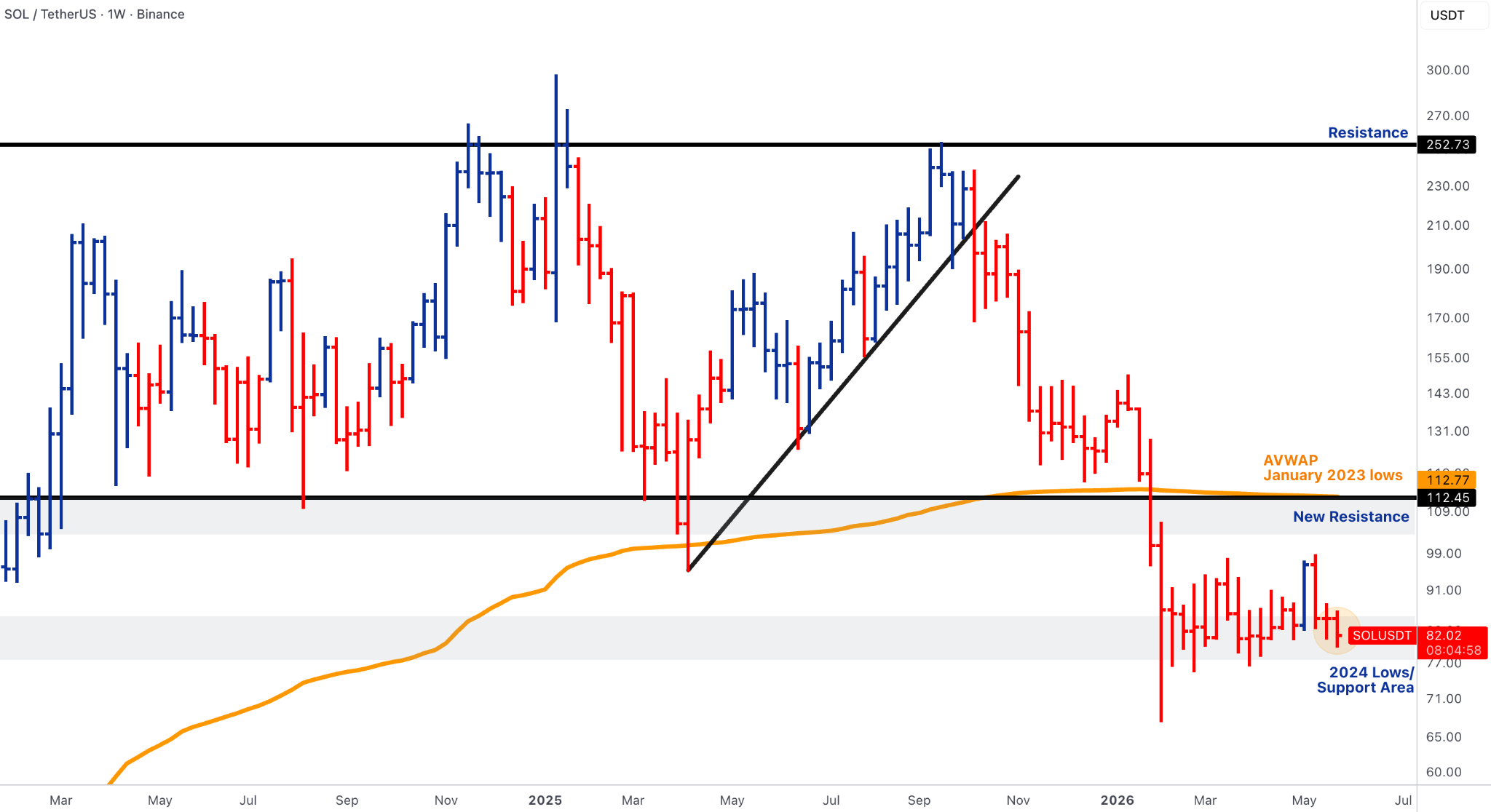

- SOL traded near $82, still well below the $112-$113 AVWAP / prior-breakout reclaim zone. The chart remains in stabilisation rather than expansion.

- VanEck launched VBNB, the first U.S. exchange-traded product designed to provide spot exposure to BNB, with shares physically backed by BNB held in cold storage with a qualified custodian.

- BNB traded around $721, pressing toward the $742 prior resistance / breakout level, making it the cleanest major-alt technical candidate if acceptance above that level confirms.

Our take: SOL has relative flow resilience versus BTC and ETH, but it lacks the scale and chart confirmation required for leadership language. Its marginally positive wrapper flow is useful, yet the asset remains trapped below the level that matters. BNB is the more interesting major-alt setup because productisation and structure are aligned: the VBNB launch gives the market a real wrapper catalyst just as price approaches $742. The distinction matters: SOL is still a stabilisation chart; BNB is a confirmation candidate, but only above $742.

Alpha Cluster - HYPE and XLM Lead Institutional Utility Repricing

- HYPE remained the cleanest selective-demand signal, with listed products attracting roughly +$55.1M across the shortened trading window while BTC and ETH ETFs remained under distribution. The catalyst stack stayed unusually clean: wrapper demand persisted, onchain perps remained in focus, and U.S. regulatory movement around perpetual futures validated the category even as it raised the competitive bar.

- The CFTC opened the door for regulated U.S. crypto perpetual futures, with Coinbase and Kalshi moving forward under CFTC oversight. That matters for HYPE because it validates perpetuals as a market-structure category, but also changes the competitive frame from offshore/onchain growth to regulated domestic derivatives access.

- XLM was the strongest top-performer inclusion, rising ~68% after DTCC and the Stellar Development Foundation announced plans to connect DTC’s tokenisation service to Stellar. DTCC said DTC-tokenised assets are expected to become available on Stellar in 1H27, giving the move a direct link to post-trade tokenised securities infrastructure.

Our take: The week’s alpha was narrow and institutional rather than broad and speculative. HYPE remains the cleanest expression of selective demand because it sits at the intersection of listed-product inflows, onchain perps and the institutionalisation of crypto derivatives; the CFTC’s move validates the category, even as it raises the competitive bar by pulling perps into regulated U.S. venues. XLM’s move was different but equally relevant: DTCC/Stellar turns the tokenisation narrative into post-trade infrastructure connectivity, giving the rally a stronger institutional catalyst than generic alt momentum. The Alpha Cluster should therefore stay deliberately narrow: HYPE for productised onchain trading infrastructure and XLM for tokenised securities infrastructure. INJ remains a watchlist continuation name, but not a core driver without a fresher catalyst.

Rails, Regulation & Institutionalisation - Plumbing Advances While Spot Beta Bleeds

- The U.S. opening for regulated crypto perpetual futures is a major market-structure development because it expands domestic regulated risk-transfer capacity and challenges the offshore/onchain derivatives complex.

- DTCC/Stellar and BIS Project Agorá reinforced the tokenised-market-infrastructure direction. DTCC is moving DTC-custodied asset tokenisation toward public-chain connectivity, while BIS Project Agorá is testing tokenised central-bank reserves and commercial-bank deposits for wholesale cross-border payments.

- Stablecoin rails kept expanding. Coinbase and Standard Chartered added institutional multi-currency funding access across AUD, SGD, CAD and CHF, with GSIB-backed settlement for EUR and GBP; Circle and Nium connected USDC settlement to last-mile payouts across more than 190 countries.

- CME’s Bitcoin Volatility futures are scheduled for 1 June, pending regulatory review, and settle to the CME CF Bitcoin Volatility Index, a 30-day forward-looking implied-volatility measure derived from CME Bitcoin options order books.

- Tokenised equities and synthetic/private-market exposures remain a risk area. The Ventuals / pre-IPO SpaceX perps episode and delays around tokenised-stock exemptions highlight legal-claim, reference-pricing, disclosure and investor-protection gaps.

Our take: Institutionalisation is still compounding, but the transmission channel has shifted away from simple spot beta. The market is building regulated derivatives, tokenised collateral, stablecoin payouts, fiat access, public-chain post-trade links and volatility products even as BTC and ETH ETFs are under redemption pressure. That is a healthier long-term infrastructure story than the price tape suggests, but it is not an immediate all-clear for risk assets. The key institutional distinction is that plumbing adoption can advance while token prices remain flow-constrained; the next phase requires productisation demand to reconnect with spot sponsorship, especially in BTC and ETH.

Outlook - Labour Data, Broadcom and Flow Stabilisation Decide Whether Repair Resumes

- The week ahead brings ISM manufacturing, JOLTS, ADP, ISM services and Friday’s May payrolls report. The market will be focused less on the payroll headline alone and more on whether wages and employment data are soft enough to ease yields without triggering a growth scare.

- The best macro outcome for crypto is soft-but-not-recessionary: enough labour cooling to reduce rate pressure, but not enough weakness to break equity risk appetite.

- Broadcom’s earnings are the main equity-transmission test. AI infrastructure remains the equity cushion, but BTC/ES must stabilise before equity strength can be treated as crypto confirmation.

- BTC needs to reclaim $79k-$80k; ETH needs $2,350-$2,400; ETH/BTC must defend 0.025; TOTAL3 needs ~$776B; SOL needs $112-$113; and BNB needs acceptance above $742.

- Flow thresholds remain decisive: BTC ETF outflows need to slow, ETH’s outflow streak needs to break, SOL wrappers need more than marginal inflows, and HYPE needs continued listed-product demand to retain alpha leadership.

Our take: Next week is a macro-transmission and flow-stabilisation test. A benign labour report would give BTC room to retest $79k-$80k, but that reclaim will not be credible without ETF outflows slowing, especially from IBIT. A hot wages print would keep the Fed inflation-constrained ahead of the 16-17 June FOMC, while a labour-break print would risk turning crypto-specific weakness into broader risk reduction. The regime remains selective until proven otherwise: HYPE and XLM represent institutional utility repricing, BNB is the major-alt productisation trigger, and BTC/ETH remain tactical repair trades until flows and relative strength confirm.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets