BTC-Led Repair Meets Inflation Friction and the Big Tech Beta Test

Blueprint - Regime, Flows & Macro Context

- ETF demand remained positive but highly concentrated. BTC spot ETFs absorbed +$823.7M across the week, materially ahead of ETH at +$155.1M and SOL wrappers at only +$9.3M. The hierarchy is therefore still clear: BTC > ETH > SOL.

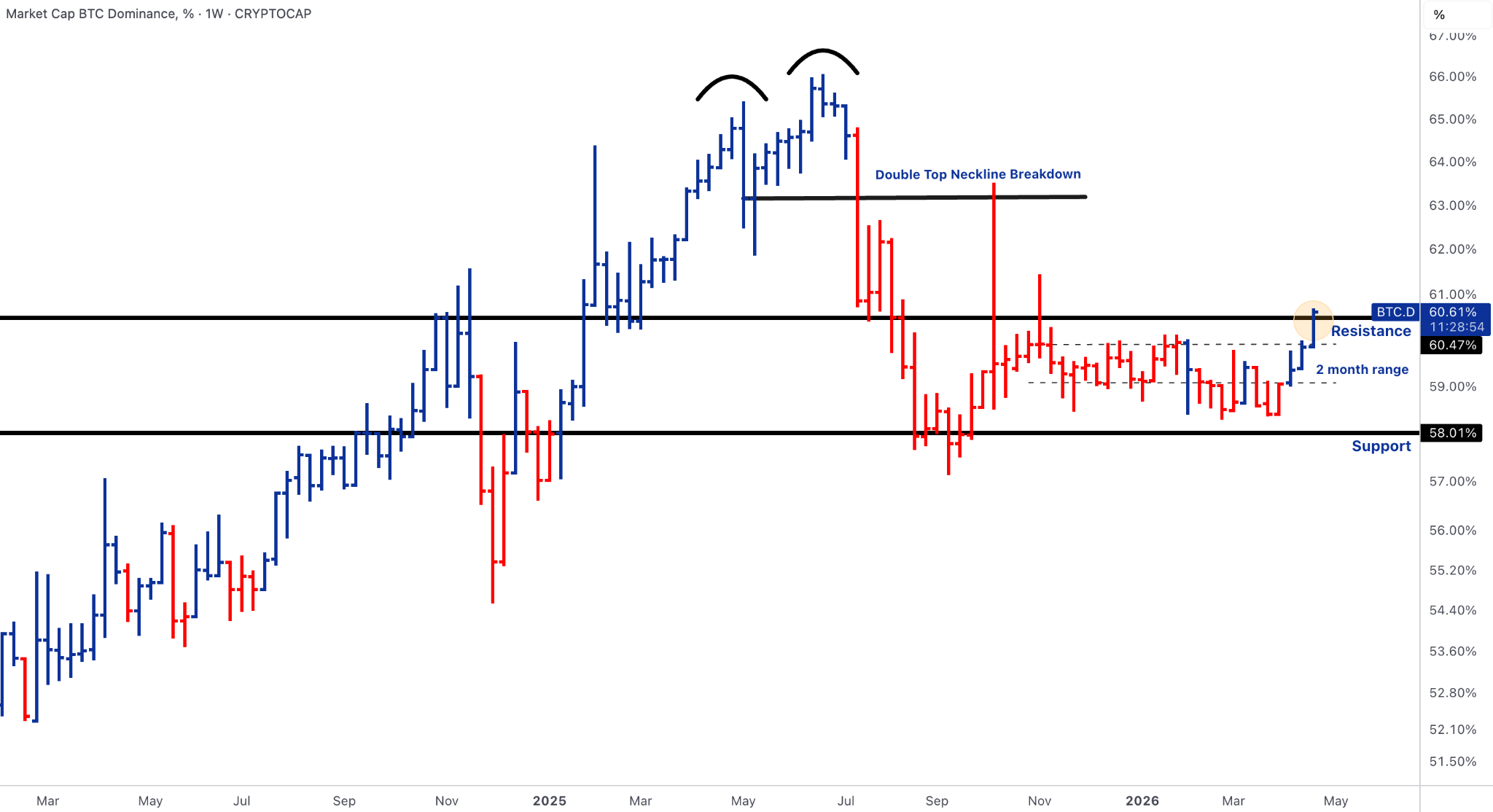

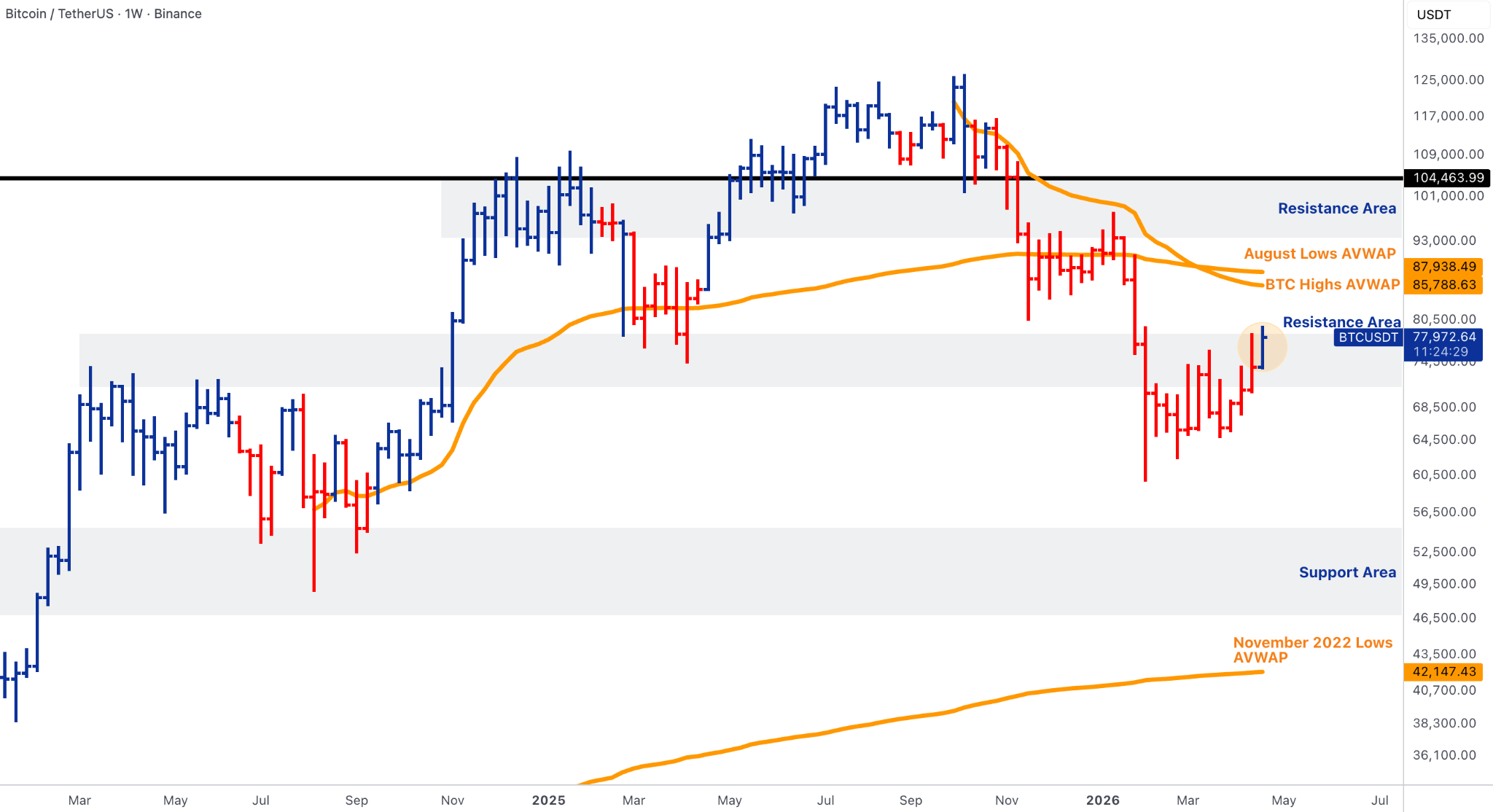

- The technical structure confirms the same message. BTC repaired fastest into the $74k-$79k supply zone, while BTC dominance pushed back above 60.47%, TOTAL3 remained below the $776B reclaim threshold, and ETH/BTC held near 0.0299, still below the first meaningful relative reclaim at 0.0354.

- Macro was not cleanly risk-on. March retail sales rose 1.7%, but the bulk of the beat came from a record 15.5% jump in gasoline-station receipts, while jobless claims stayed contained at 214k and the S&P Global U.S. composite PMI rebounded to 52.0. The inflation impulse worsened: S&P Global reported output prices rising at the fastest pace since July 2022, while University of Michigan year-ahead inflation expectations jumped to 4.7% and long-run expectations rose to 3.5%.

- The next macro-risk window is unusually dense: FOMC, GDP, PCE, ECI, ISM manufacturing and five mega-cap tech earnings land in the same week. Alphabet, Microsoft, Amazon and Meta report Wednesday, followed by Apple Thursday; together, those names represent nearly $16T of market value and roughly a quarter of the S&P 500.

Our take: The market has repaired, but it has not broadened. BTC is absorbing the institutional bid and rebuilding price structure first, while ETH is participating with weaker flow quality and the rest of the stack remains largely tactical. This is important because the macro backdrop is no longer a simple liquidity easing story: growth is holding, but inflation pressure is rising through energy, supply-chain and pricing channels. The next confirmation test is therefore not only crypto-native; it is also equity-beta transmission. If Big Tech earnings validate AI capex, cloud growth and margin durability, BTC/ES can continue repairing and ETF-led BTC demand should remain insulated. If mega-cap leadership disappoints into FOMC/PCE, crypto risks losing the equity tailwind just as BTC is testing its first major resistance band.

BTC - ETF Absorption Carries the Cleanest Repair

- BTC spot ETFs delivered +$823.7M of net inflows, with real accumulation clustered on 20, 22 and 23 April. The flow was constructive but not euphoric: 21 and 24 April were effectively flat, and IBIT remained the dominant driver, keeping the week BlackRock-led rather than broad all-issuer accumulation.

- BTC has repaired into the $74k-$79k supply zone. Acceptance above $79k-$80k would materially improve the tactical structure and open the next AVWAP cluster around $85.8k-$87.9k. Failure here would argue for consolidation after the squeeze rather than immediate continuation.

- BTC/ES has improved from support but remains incomplete. The ratio is around 10.84, still below the 12.41 short-term reclaim and the larger 13.7-14.0 resistance band. That means crypto is no longer being dominated by equities, but BTC has not yet fully re-established higher-timeframe leadership versus the S&P.

Our take: BTC is the cleanest asset in the pack because it has both flow support and chart repair. The important nuance is that the move is no longer in the easy part of the rebound. The first short-covering phase has already occurred; what matters now is whether ETF demand remains strong enough to absorb supply near $79k-$80k while macro markets digest FOMC, PCE and mega-cap earnings. A weekly acceptance above that band would shift the conversation toward $86k-$88k. A rejection, especially if BTC.D remains elevated and TOTAL3 fails below $776B, would confirm that institutional capital is still buying BTC as the safest crypto beta rather than rotating down the risk curve.

ETH - Constructive, But Still Not Leadership

- ETH ETFs posted +$155.1M of weekly net inflows, but the flow structure was less stable than BTC. The first three sessions were constructive, 23 April delivered a meaningful outflow reset, and 24 April saw only a modest recovery.

- ETH is testing the June 2022 low AVWAP near $2,365, but the chart remains below the stronger $2.5k–$2.6k reclaim band and far below the April-low AVWAP near $2,969. ETH/BTC remains the main constraint: around 0.0299, it is stabilising, but still below 0.0354 and materially below the larger 0.0398 resistance area.

- Institutional ETH demand had supportive but not decisive newsflow. The Ethereum Foundation sold 10,000 ETH OTC to BitMine at an average price of $2,387, while BitMine’s ETH staking reportedly moved above 70% of holdings after its latest staking push.

Our take: ETH is improving, but it is still an improving laggard. The BitMine/EF transaction and staking demand help absorb supply and support the institutional ETH treasury narrative, but the ETF tape and ETH/BTC structure do not justify calling ETH the leadership asset. The upgrade path is clear: ETH needs to hold the $2,365 AVWAP area, reclaim $2.5k-$2.6k, and see ETH/BTC regain 0.0354. Until then, ETH remains a repair trade with better fundamental sponsorship than relative price action.

SOL & BNB - Stabilisation Without Confirmation

- SOL wrapper flows slowed to +$9.3M, with most of the week’s net coming from a single positive session on 23 April. That is stabilising, but not enough to confirm institutional re-risking into SOL.

- SOL remains structurally damaged below the $112-$113 reclaim zone, which also aligns with the January 2023 AVWAP. Until that area is reclaimed, SOL should be treated as a lower-range stabilisation trade rather than a restored leadership asset.

- BNB recovered into the low $600s, but remains below the broken $742 structure. The chart is more orderly than SOL, but still not repaired.

Our take: SOL and BNB are not leading this move. SOL has more upside convexity if it can reclaim $112-$113, but the flow data does not yet validate that scenario. BNB remains a cleaner range-repair candidate, but the decisive level is still $742, not current price. The correct institutional framing is restraint: BTC is repairing; ETH is improving; SOL and BNB are stabilising, but neither has confirmed leadership.

Alpha Cluster - Catalyst Quality Narrows the Beta Trade

- LINK carried the strongest institutional catalyst in the weekly alpha set. AWS made the Chainlink Data Standard available through AWS Marketplace, including Data Feeds, Data Streams and Proof of Reserve, effectively placing oracle, real-time market-data and reserve-attestation infrastructure inside enterprise cloud procurement rails. The relevance is structural rather than purely token-specific: LINK is becoming a cleaner expression of tokenisation infrastructure, proof-of-reserve demand and institutional-grade data distribution.

- HYPE added high-beta productisation optionality after Grayscale amended its Hyperliquid ETF filing. The proposed trust is designed to hold HYPE directly, giving the asset a regulated-wrapper narrative at a point in the cycle where ETF access is increasingly shaping relative demand across digital assets. The catalyst remains preliminary and approval-dependent, but it is still more institutionally relevant than generic high-beta rotation because it links directly to market-structure productisation.

- CHZ was the cleanest tactical inclusion from the weekly performer screen. The move fits a specific SportFi/fan-token setup, with CHZ pushing from roughly $0.040 toward $0.047 around renewed World Cup-linked attention and stronger sports-token activity. The catalyst is narrower than LINK or HYPE, but it is liquid, legible and calendar-driven enough to qualify as a selective breadth signal.

Our take: Alpha quality remains narrow and catalyst-dependent. LINK carries the cleanest institutional read-through because the AWS integration ties directly into the week’s broader rails narrative: tokenised assets, reserve transparency and enterprise data infrastructure. HYPE sits further out on the risk curve, but the Grayscale filing gives it a credible productisation angle rather than a purely speculative beta profile. CHZ adds tactical breadth through SportFi and event-driven positioning, but does not change the broader regime signal. The key distinction is that individual catalyst trades are working, while the market has not yet confirmed broad alt expansion: BTC.D remains above 60.47%, TOTAL3 is still below $776B, and institutional flow remains concentrated in BTC.

Rails, Regulation & Institutionalisation - Adoption Advances, DeFi Risk Resurfaces

- AWS made Chainlink Data Feeds, Data Streams and Proof of Reserve available through AWS Marketplace, putting oracle, market-data and reserve-attestation tooling directly inside enterprise cloud procurement rails.

- Morgan Stanley Investment Management launched the Stablecoin Reserves Portfolio, a government money-market fund designed to align with GENIUS Act reserve requirements for payment stablecoin issuers. The fund invests only in cash, U.S. Treasury securities with remaining maturities of 93 days or less, and certain overnight Treasury/cash-collateralised repos.

- Stablecoin enforcement risk also moved to the foreground. The U.S. Treasury sanctioned Iran-linked wallets, freezing $344M in cryptocurrency, reinforcing that stablecoins are increasingly both payment rails and sanctions rails.

- DeFi delivered the week’s main institutional offset. Galaxy’s KelpDAO/LayerZero analysis described a roughly $292M exploit tied to RPC poisoning and LayerZero DVN assumptions, with Lazarus preliminarily linked and broader implications for LRT collateral, Aave risk frameworks and bridge/custody assumptions.

Our take: The institutionalisation story is bifurcating. Regulated rails are accelerating: stablecoin reserve products, tokenised liquidity infrastructure, Chainlink/AWS distribution and payment-rail policy are all moving crypto deeper into traditional finance. Permissionless DeFi, however, continues to face a credibility ceiling around bridge risk, collateral socialisation, governance response times and emergency-admin powers. The week’s strongest structural message is therefore not “DeFi is institutionally ready”; it is that regulated digital-asset rails are advancing faster than open DeFi risk systems are hardening.

Outlook - FOMC, PCE, GDP, ECI, ISM and the $16T Earnings Test

- The FOMC meets 28-29 April. The April meeting is not an SEP meeting, so the focus is statement language, inflation framing and Powell’s press conference rather than fresh dot-plot guidance.

- 30 April is the macro data cluster: BEA releases both Q1 GDP advance estimate and March Personal Income and Outlays/PCE, while BLS releases Q1 Employment Cost Index. ISM Manufacturing follows on 1 May.

- The equity transmission channel is just as important. Alphabet, Microsoft, Amazon and Meta report Wednesday, Apple follows Thursday, and the combined market value of those companies is close to $16T.

- Crypto confirmation levels remain clean: BTC needs $79k-$80k acceptance to target $85.8k-$87.9k; ETH needs to defend $2,365 and reclaim $2.5k-$2.6k; SOL needs $112-$113; TOTAL3 needs $776B; BTC.D needs to lose 60.47% for breadth to improve.

Our take: The next phase is a confirmation test across three channels: Fed inflation tolerance, AI/equity leadership, and crypto breadth. If FOMC and PCE do not reprice real yields higher, and Big Tech earnings validate AI capex and cloud growth, BTC can continue grinding toward the $86k-$88k AVWAP cluster on ETF demand. But the note should not upgrade to broad crypto expansion unless breadth confirms: TOTAL3 must reclaim $776B, ETH/BTC must regain 0.0354, and SOL/BNB must clear their first structural levels. Until then, the preferred institutional stance remains BTC-led, flow-aware and selective on alts, with rails/productisation carrying the strongest structural narrative beneath the price action.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets