Late-Week ETF Rescue Masks a Narrower Crypto Regime

Blueprint - Regime, Flows & Macro Context, Continued...

- ETF demand remained positive at the headline level, but the quality of the flow deteriorated materially versus the prior week. BTC spot ETFs finished with +$162.8M of weekly net inflows, down from +$823.7M the previous week, and only turned positive because of a +$629.8M Friday reversal after three consecutive outflow sessions. ETH ETFs posted -$82.5M despite a Friday recovery, while SOL wrapper demand was effectively absent at -$1.2M.

- The chart structure remains BTC-led but unconfirmed. BTC is consolidating inside the $74k-$79k resistance band, BTC dominance is holding above 60.47%, TOTAL3 remains below the $776B reclaim threshold, and ETH/BTC remains weak near 0.0296, below the first meaningful relative reclaim at 0.0354. This supports selective repair, not broad crypto expansion.

- Macro remained growth-resilient but inflation-constrained. The Fed held the target range at 3.50%-3.75%, but the statement carried a divided signal: Stephen Miran dissented in favour of a 25bp cut, while Beth Hammack, Neel Kashkari and Lorie Logan supported holding rates but objected to retaining an easing bias. Q1 real GDP recovered to 2.0% annualised, while the Q1 PCE price index rose 4.5% annualised and core PCE rose 4.3%, reinforcing the inflation-friction theme.

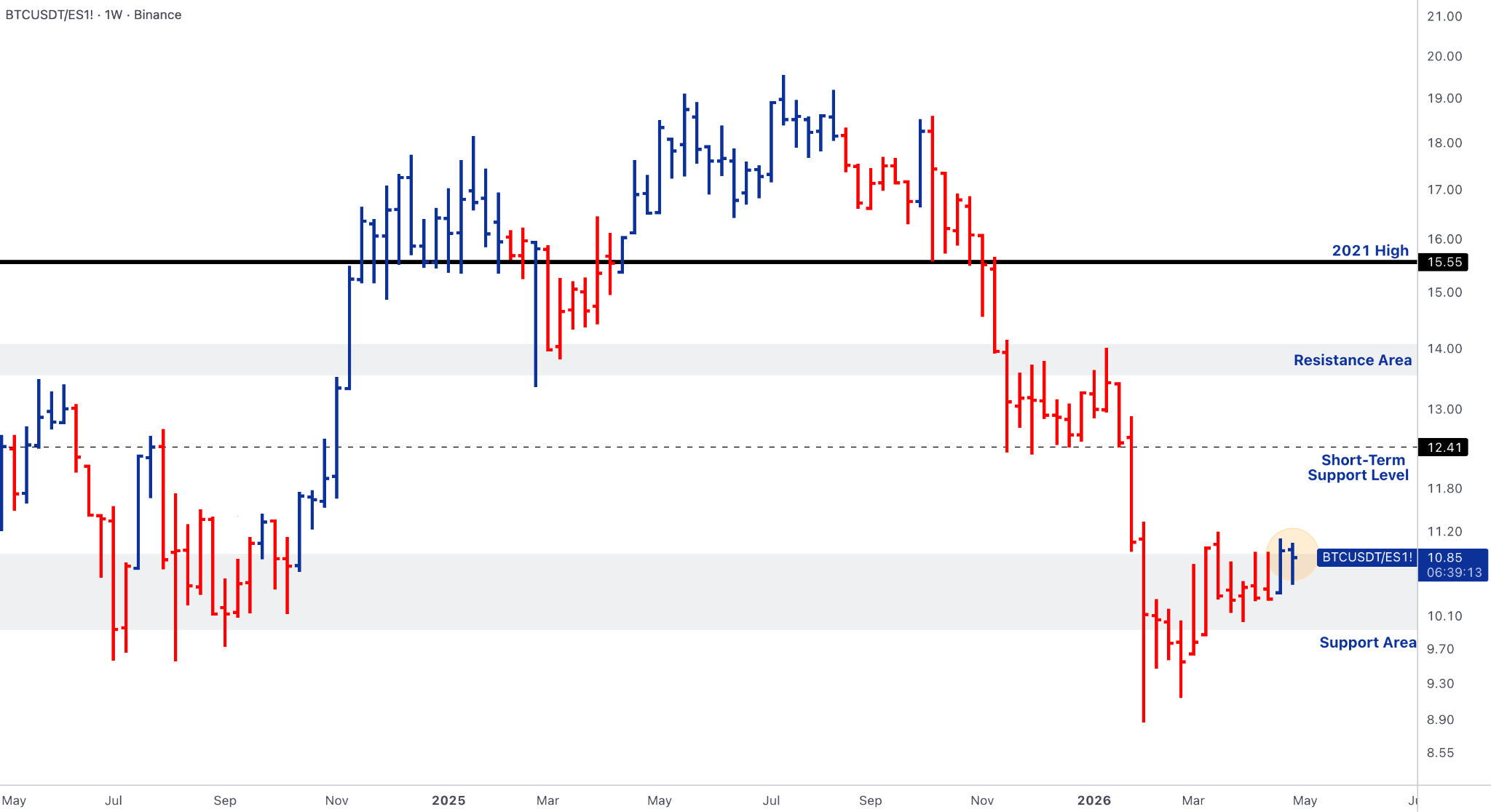

- The equity-risk channel held, but the AI trade became more selective. Google Cloud emerged as the clear standout among mega-cap reports, while the broader market began separating AI/cloud monetisation from capex-heavy narratives. BTC/ES stabilised near 10.85, but remains below the 12.41 reclaim, meaning equities provided a risk floor without confirming crypto outperformance.

Our take: The regime remains narrow. BTC continues to act as the cleanest institutional expression because it has the strongest ETF support, the best chart repair, and the clearest macro narrative in an inflation-heavy environment. But the quality of the move has weakened: ETF demand was rescued late rather than accumulated steadily, BTC has not accepted above $79k-$80k, and breadth remains constrained by elevated dominance and an unrepaired TOTAL3 structure. The market is therefore best described as BTC-led resilience under inflation friction, not a broad re-risking cycle.

BTC - Friday ETF Rescue Keeps the Repair Alive

- BTC spot ETFs finished with +$162.8M of net inflows, but the week was defined by reversal rather than steady accumulation. The first three sessions saw cumulative outflows of roughly -$490.5M, 30 April was only marginally positive, and the week was rescued by the +$629.8M inflow on 1 May. IBIT, FBTC and ARKB were the main positive offsets, while GBTC remained a drag.

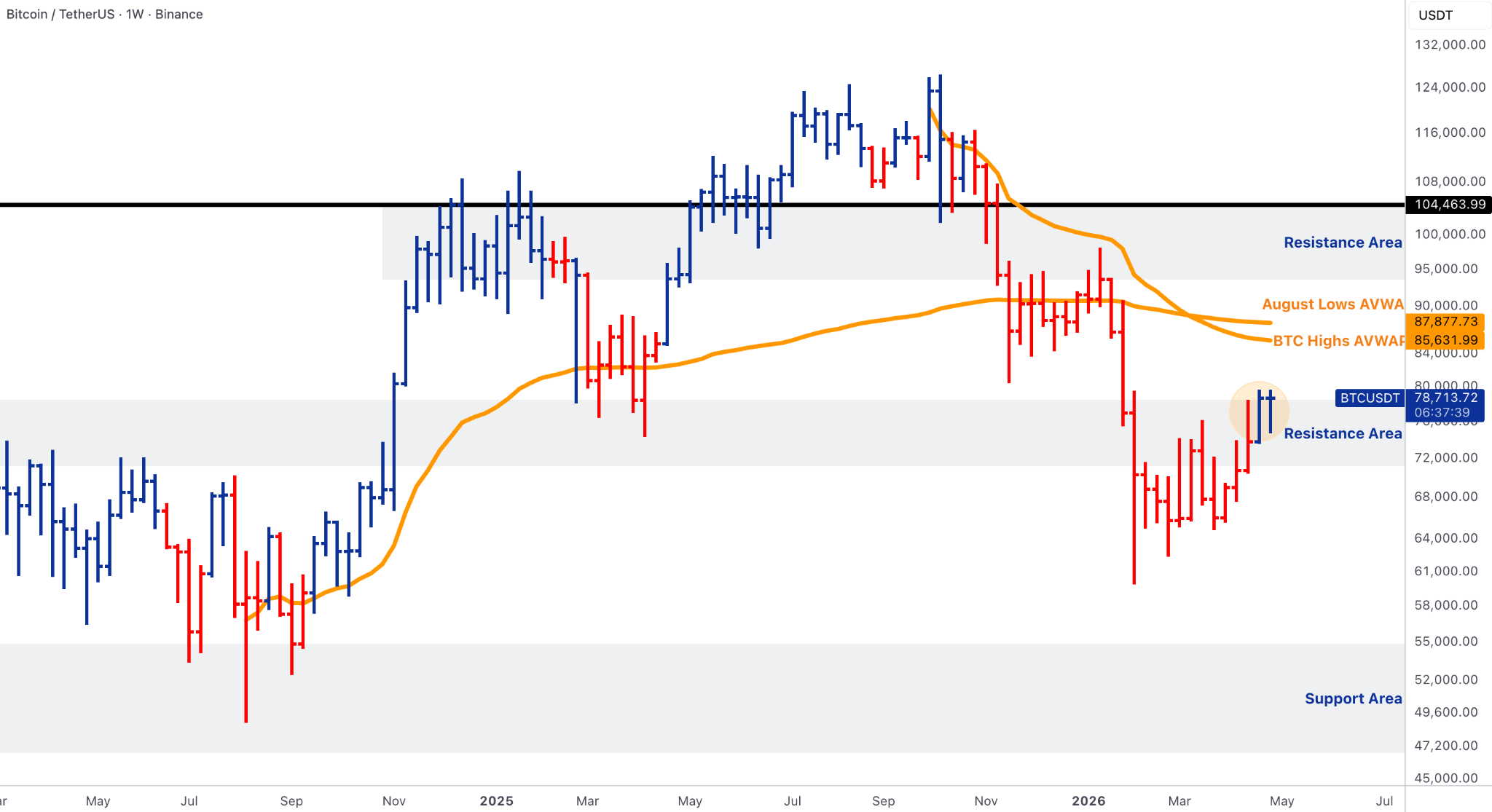

- BTC remains inside the first major resistance band around $74k-$79k, trading near $78.7k. Acceptance above $79k-$80k remains the tactical trigger; above that, the next major resistance cluster is the BTC highs AVWAP near $85.6k and the August lows AVWAP near $87.9k. The larger structural ceiling remains around $104.5k.

- The macro setup is mixed for BTC. Inflation data strengthened the scarcity/debasement narrative, but the Fed’s divided hold, hot PCE, elevated ISM prices and energy shock keep real-yield risk live. ISM Manufacturing held expansion at 52.7, but the Prices Index rose to 84.6, its highest level since April 2022, with ISM explicitly tying pressure to steel/aluminium, tariffs and petroleum-linked inputs from the Middle East conflict.

Our take: BTC is still the leadership asset, but the week did not deliver clean confirmation. The Friday ETF inflow matters because it prevented a negative weekly flow outcome and kept price supported near resistance; however, a single-session reversal is lower-quality than steady multi-day accumulation. The next decision point is straightforward: sustained acceptance above $79k-$80k would put $85.6k-$87.9k back in play, while rejection from this band would imply that ETF demand is stabilising the market but not yet strong enough to force a new impulse leg. BTC remains the preferred crypto exposure, but conviction should be tied to flow persistence and price acceptance rather than the headline weekly inflow alone.

ETH - Treasury Support Cannot Offset Weak Relative Structure

- ETH ETFs posted -$82.5M of weekly net outflows. The complex saw four consecutive outflow sessions before a +$101.2M Friday rebound, leaving the weekly structure materially weaker than BTC. ETHA and FETH were the main drags, while ETHB was the only meaningful positive offset.

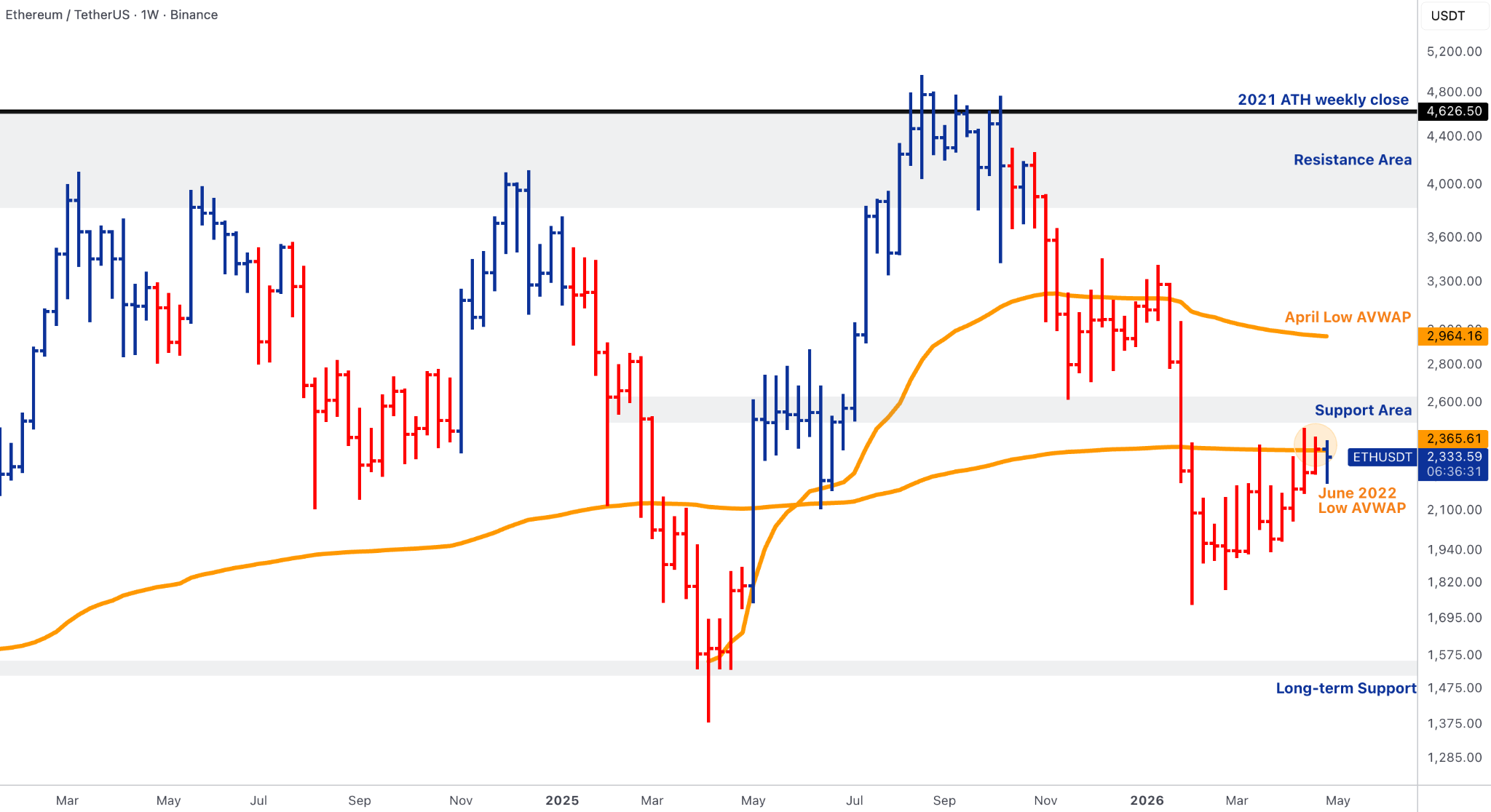

- ETH is trading around $2,330, slightly below the June 2022 low AVWAP near $2,365-$2,366. The immediate reclaim remains $2,365-$2,400, followed by the stronger $2.5k-$2.6k repair band. The April low AVWAP near ~$2,964 remains the larger structural hurdle.

- ETH/BTC remains the key constraint. The ratio is near 0.0296, still below 0.0354 short-term resistance and far below the 0.0398 major resistance area. This confirms that ETH has stabilised versus its lows but has not reclaimed leadership.

- ETH continues to receive corporate-treasury support, with the Ethereum Foundation completing another 10,000 ETH OTC sale to BitMine at an average price near $2,292, bringing recent EF sales to BitMine to roughly $47M over two weeks. That supports the treasury-absorption narrative, but not enough to offset negative ETF flows and weak relative structure.

Our take: ETH remains an improving but fragile laggard. Treasury accumulation and staking demand help absorb supply, but the market is not rewarding ETH with leadership: ETF flows turned negative, ETH failed to hold above the June 2022 AVWAP, and ETH/BTC remains structurally weak. The upgrade path is unchanged. ETH needs to reclaim $2,365-$2,400, then $2.5k-$2.6k, while ETH/BTC must regain 0.0354 before the asset can be framed as more than a beta repair trade. Until then, ETH should remain secondary to BTC in the institutional hierarchy.

SOL & BNB - Stabilisation Without Flow Confirmation

- SOL wrapper demand was effectively absent, finishing the week at -$1.2M. There was no meaningful institutional allocation through the wrapper complex, and the only flow print was a small GSOL outflow on 30 April.

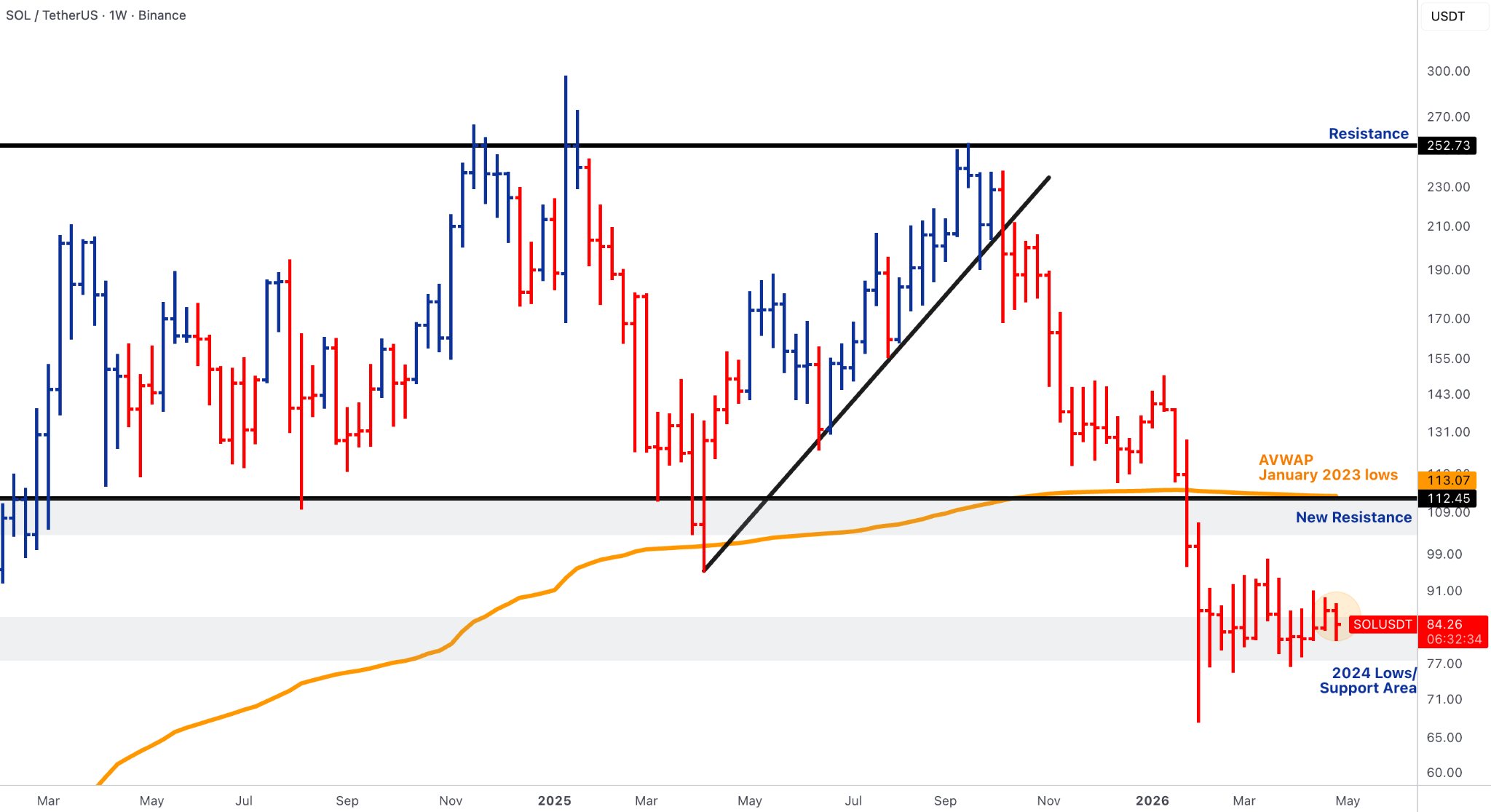

- SOL remains trapped in the damaged lower range around $84, still far below the decisive $112-$113 reclaim zone, which also aligns with the January 2023 lows AVWAP. The current structure remains closer to stabilisation around the 2024-lows support area than genuine repair.

- BNB is trading around $620, more orderly than SOL but still below the broken $742 structure. The lower support area around $500-$535 remains relevant if the bounce fails, while $742 is the level needed to restore a more constructive chart.

- Stablecoin and payment-rail newsflow increasingly touches Solana and broader application rails, including Meta enabling USDC creator payouts on Solana and Polygon. The token-level read-through remains limited, however, because SOL’s own chart and wrapper flows do not yet confirm leadership.

Our take: SOL and BNB remain in the stabilisation bucket. SOL has clear upside convexity if it reclaims $112-$113, but the current chart and flow data do not validate a leadership call. BNB’s structure is cleaner but incomplete below $742. The broader lesson is that rails adoption does not automatically equal immediate token outperformance. Application and payment use cases are advancing, but the majors below BTC still need price confirmation, flow confirmation and dominance relief before they can credibly lead.

Alpha Cluster - Catalyst Quality Remains Narrow

- ZEC carried the cleanest week-specific catalyst in the alpha set. Grayscale Zcash Trust activity accelerated in April, with average daily volume rising to roughly $1.7M, while ZEC shielded supply reached a record high. The Orchard shielded pool reportedly grew from 1.92M ZEC to 4.55M ZEC over the past year, bringing shielded balances close to 30% of circulating supply.

- TAO was the highest-quality liquid name from the top-performer screen. The move fits the broader AI-infrastructure trade after mega-cap earnings kept AI capex investable, even as the market became more selective between companies with visible AI/cloud monetisation and those facing heavier capex scrutiny.

- PUMP had a specific tokenomics catalyst after Pump.fun burned roughly $370M of previously repurchased PUMP tokens, equal to approximately 36% of circulating supply, and committed 50% of future revenue to buybacks/burns for the next 12 months. The catalyst is measurable, but it remains high-beta application risk rather than institutional core exposure.

Our take: The alpha tape is active, but still narrow. ZEC has the strongest week-specific read-through because privacy usage, trust liquidity and shielded-supply growth all point toward a tighter and more differentiated asset profile. TAO is the cleaner liquid AI-beta expression, helped by equity-market confirmation that AI infrastructure remains a fundable theme. PUMP adds tactical tokenomics optionality, but belongs further out on the risk curve. None of this changes the broader regime signal: catalyst trades are working selectively, but broad alt expansion is not confirmed while BTC.D holds above 60.47%, TOTAL3 remains below $776B, and ETF demand remains concentrated in BTC.

Rails, Regulation & Institutionalisation - Stablecoin Infrastructure Leads, DeFi Risk Caps the Narrative

- Stablecoins and payment rails were the strongest structural theme. Visa said its stablecoin settlement pilot now supports nine blockchains and has reached a $7B annualised settlement run-rate, up 50% since the prior quarter. Meta’s USDC creator payouts, Western Union’s stablecoin plans, Shinhan Card’s Solana stablecoin work and Ripple/OKX RLUSD distribution all point to the same direction: regulated payments infrastructure is absorbing stablecoin rails faster than broad DeFi beta.

- The regulatory perimeter is becoming more precise. BlackRock pushed back against proposed limits on tokenised reserve assets under GENIUS Act implementation, while the stablecoin-yield compromise around the CLARITY Act appears to preserve activity-based rewards while restricting bank-deposit-like passive yield. Morgan Stanley’s Stablecoin Reserves Portfolio adds a TradFi reserve-management layer, investing only in cash, short-dated U.S. Treasuries with maturities of 93 days or less, and certain overnight Treasury/cash-collateralised repos.

- Tether remains central to the stablecoin reserve story. The issuer reported $1.04B of Q1 profit and an excess reserve buffer of $8.23B, reinforcing both the profitability and systemic relevance of the largest stablecoin issuer.

- DeFi security remained the major institutional offset. TRM Labs estimated that North Korean-linked actors stole roughly $577M through the Drift and KelpDAO attacks, accounting for 76% of crypto hack losses through April; KelpDAO alone involved approximately $292M, with $75M frozen on Arbitrum. This keeps bridge risk, governance risk and cross-chain laundering exposure central to institutional DeFi underwriting.

- Productisation continued through market-structure expansion. CME plans to launch AVAX and SUI futures on 4 May, pending regulatory review, with both micro and larger contracts available. Separately, MARA’s $1.5B Long Ridge acquisition shows the miner narrative continuing to migrate from pure BTC production toward energy ownership, data centres and AI compute optionality.

Our take: The structural adoption story is increasingly centred on regulated rails rather than open-ended DeFi beta. Stablecoin settlement, reserve products, tokenised collateral, payment distribution and derivatives listings are all moving in a direction institutions can underwrite. DeFi is also adapting, but the Kelp/Drift exploit cycle shows why institutional adoption remains constrained by bridge risk, governance latency, emergency-admin powers and collateral-risk assumptions. The correct framing is bifurcation: regulated digital-asset rails are accelerating, while permissionless risk systems still need to prove they can harden fast enough for institutional balance sheets.

Outlook - Payrolls, Refunding, Fed Speak and AI-Beta Confirmation

- The next macro test is labour. The April Employment Situation is scheduled for Friday, 8 May, with JOLTS, ADP and weekly claims setting up the labour-market read beforehand.

- Rates volatility remains central after the divided FOMC. Treasury’s financing estimates are scheduled for 4 May, followed by refunding/auction-schedule documents on 6 May. This matters because crypto is entering the week with BTC still below $79k-$80k acceptance and ETF demand already decelerated versus the prior week.

- AI/data-centre earnings remain the equity-beta channel. After mega-cap earnings defended the AI trade, the market will now look to Palantir, AMD, Arista and Super Micro for confirmation that AI infrastructure demand remains strong beyond the largest platforms.

- Oil and Hormuz remain the inflation-tail overlay. OPEC+ agreed a symbolic 188k bpd June quota increase, but the increase remains largely theoretical while Strait of Hormuz disruptions continue to limit Gulf exports and keep energy inflation risk elevated.

- Crypto-native productisation continues with CME’s planned AVAX and SUI futures launch on 4 May, though derivatives access should be treated as structural market development rather than immediate spot-demand confirmation.

- The key crypto levels remain unchanged. BTC needs acceptance above $79k-$80k to target $85.6k-$87.9k. ETH needs to reclaim $2,365-$2,400, then $2.5k-$2.6k. TOTAL3 needs $776B. BTC.D needs to lose 60.47%. SOL needs $112-$113. BNB needs $742.

Our take: The next phase is a confirmation test across labour, yields and equity beta. A soft-but-not-broken payroll print with contained wages would help real yields and support BTC’s attempt to hold the $74k-$79k band. A hot jobs or wage print would reinforce the Fed’s inflation caution and increase rejection risk near $79k-$80k. Treasury refunding and Fed communication will determine whether rates volatility stays contained, while AI earnings will decide whether the equity-risk floor remains supportive for BTC/ES and TAO-style AI beta. Until BTC accepts above resistance and breadth improves, the preferred institutional stance remains BTC-led, flow-aware and selective on alts, with stablecoin rails, productisation and tokenised reserve infrastructure carrying the strongest structural narrative beneath the price action.

Thanks for reading this week's Market Pulse.

You can follow us on Telegram for all our updates: @HT Markets