Repair Bid Meets Macro Friction

Blueprint - Spot Bid Returns, Breadth Still Lags

- US spot BTC ETFs printed +$816.9M net for the week, driven by a +$471.4M Monday impulse and renewed strength on Thursday and Friday; US spot ETH ETFs added +$187.0M net, while US spot SOL ETPs finished the week at roughly -$5.8M.

- March US CPI rose 0.9% m/m and 3.3% y/y, while preliminary April University of Michigan consumer sentiment fell to a record low 47.6 from 53.3 in March.

- Weekend macro risk re-escalated after US-Iran talks ended without a breakthrough, though Saudi Arabia said its East-West pipeline had been restored to full 7 million bpd capacity.

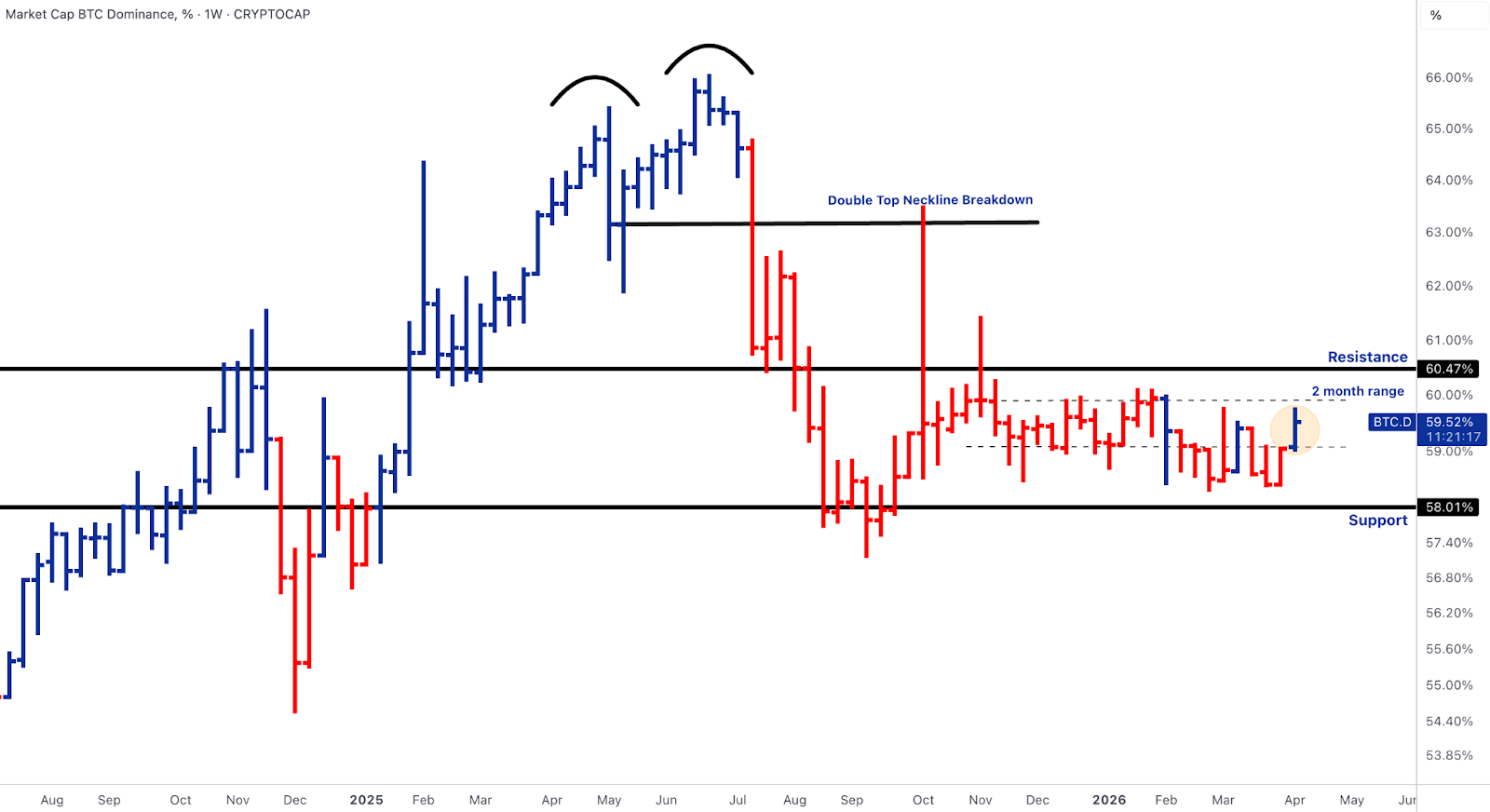

- BTC.D is still range-bound near 59.5%, holding between roughly 58.0% support and 60.5% resistance, and remains below the post-double-top breakdown threshold.

- TOTAL3 is sitting near $707B, still below the key ~$776B reclaim line but above the April 2025 low near $658B.

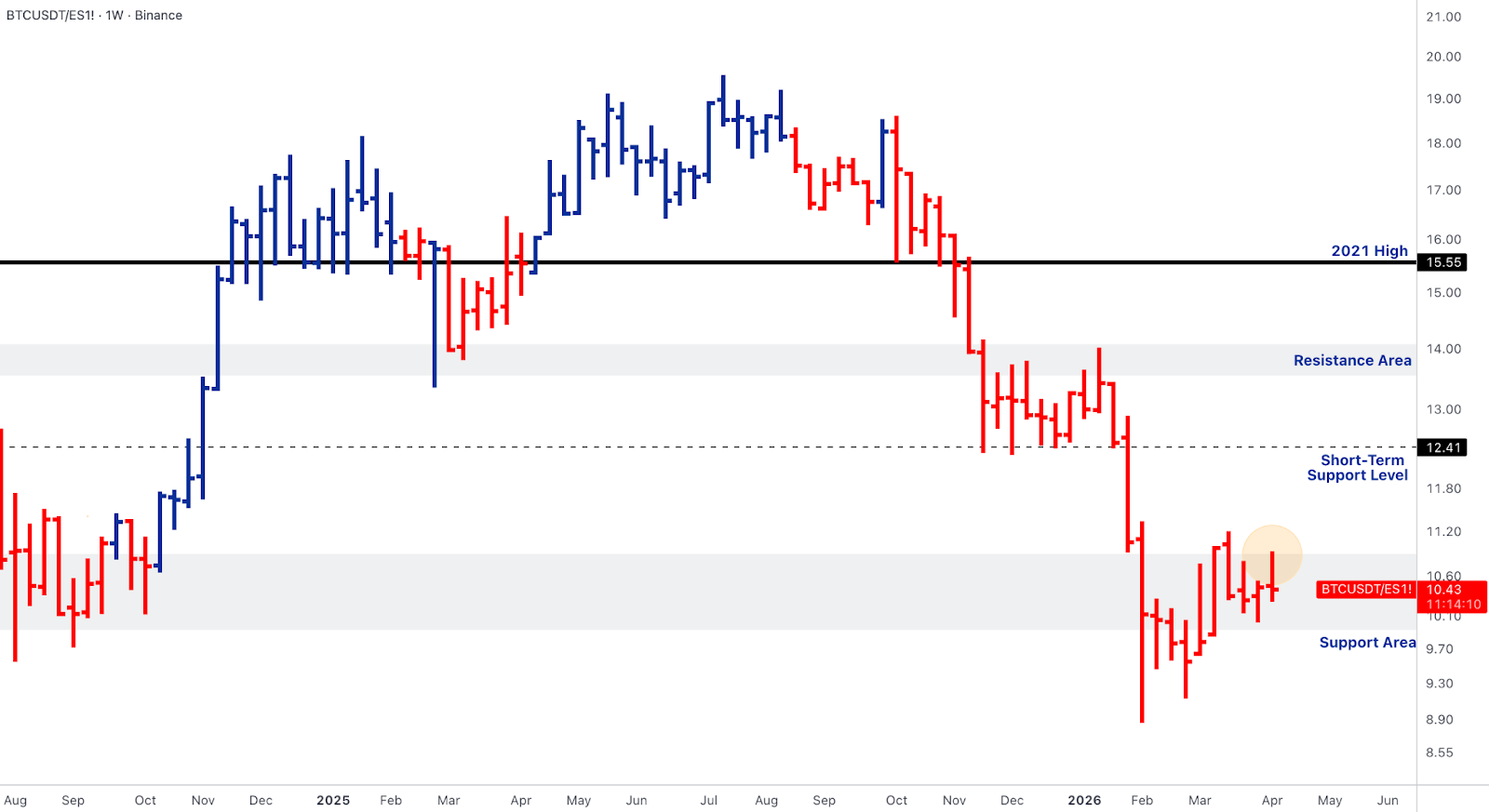

- BTC/ES remains depressed around 10.4, which keeps crypto in a relative underperformance regime versus equities.

- Private-credit stress remains a secondary macro overhang: the Fed has asked major banks for details on their exposure to private-credit firms, and Wall Street has launched a new CDS index designed to hedge or short private-credit risk.

Our take: The market is trading better, but it is not yet trading cleanly. Spot ETF demand has re-accelerated, especially in BTC, yet the broader backdrop remains difficult: inflation has re-firmed, confidence has deteriorated, geopolitics is still driving the weekend open, and cross-asset credit anxiety has not gone away. The charts reflect that split. BTC and ETH are attempting repair, breadth is trying to base, and BTC dominance has not broken higher, but none of those signals has crossed the levels that would justify calling a durable regime turn.

BTC - Better Spot Sponsorship, Incomplete Institutional Confirmation

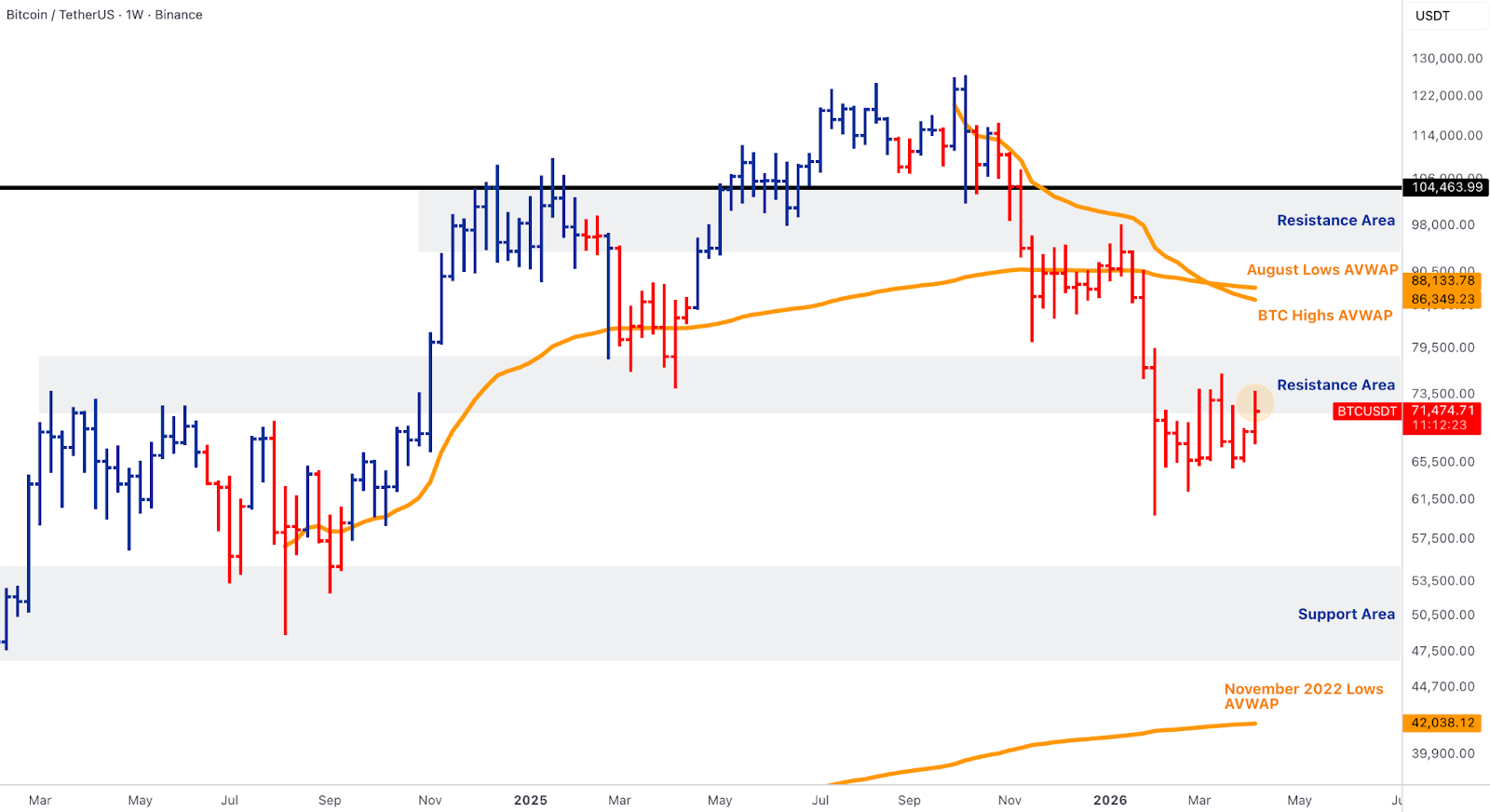

- BTC is trading back into the first low-to-mid $70k supply shelf, while the more important reclaim cluster still sits materially higher in the upper-$80k AVWAP zone.

- Morgan Stanley launched MSBT with a 0.14% sponsor fee, which the firm said is currently the lowest bitcoin ETP sponsor fee at launch.

- Despite the stronger weekly net print, the ETF tape was not one-way: Tuesday and Wednesday both saw net outflows before demand reaccelerated into the end of the week.

- The broader institutional derivatives complex still looks softer than the cash ETF tape: CME bitcoin futures open interest fell below $8B in March and to roughly $7.2B in early April as the basis trade unwound, with CME bitcoin futures activity falling to a 14-month low.

Our take: Bitcoin is still in base-building mode beneath supply, not in trend restoration. The constructive side of the tape is that treasury-style demand remains alive: Metaplanet added 5,075 BTC to bring total holdings to 40,177 BTC, while broader institutional access keeps expanding through products, custody, and listed vehicles. But that demand is being partially neutralised by real supply. Riot sold 3,778 BTC worth about $290M during the first quarter, while bitcoin also closed its worst first quarter since 2018, underscoring how weak the broader backdrop has been. The result is a market that can squeeze higher on positioning, but still struggles to reclaim broken shelves cleanly enough to change the regime.

ETH - Relative Improvement, Still Below the Real Reclaim Line

- ETH ETF demand was constructive throughout the week, with the complex finishing +$187.0M net and posting positive totals on Thursday and Friday.

- ETH is rebounding but remains below the key reclaim markers around the June 2022 AVWAP (~$2.37k) and the April low AVWAP (~$2.98k).

- ETH/BTC has improved back toward ~0.0309, holding above the immediate support band but still below the more important ~0.0354 short-term resistance.

- The Ethereum Foundation said it had cleared two-thirds of its 70,000 ETH staking target, while Bitmine disclosed a further 71,252 ETH weekly purchase, its largest weekly haul since late December

Our take: ETH’s tape is improving, and its relative chart versus BTC is one of the cleanest. Positive ETF flows, incremental treasury staking, and visible corporate accumulation are all supportive at the margin. But structurally, ETH is still not through the first reclaim threshold that would separate a bounce from a repair phase. The market has stopped getting worse; it has not yet become strong. Until ETH can hold above the ~$2.37k line and push ETH/BTC through the ~0.035 area, the right framing remains relative stabilization, not leadership.

SOL & BNB - Holding Support, Still in Repair

- SOL ETP flows stayed weak, finishing the week around -$5.8M, and the chart pack still shows SOL below the $112-113 reclaim zone.

- BNB remains below the prior breakout area around $742 on the chart pack, even as it continues to hold above the broader support shelf.

- Neither asset has yet reclaimed the levels that would justify calling renewed leadership.

Our take: SOL and BNB remain useful barometers of alt-risk appetite, but neither chart is giving a clean leadership message. SOL is still the weaker structure and continues to trade beneath the zone that would mark a credible repair. BNB is firmer by comparison, but it too remains below the level that invalidated the prior breakout failure. In practical terms, both are still repair candidates rather than leadership signals.

Alpha Cluster - Idiosyncratic Strength, Not Broad Alt Leadership

- Grayscale’s Zcash vehicle remains positioned for ETF conversion, and reports tied this week’s move to roughly $46M of shielded ZEC accumulation.

- WLD has the cleanest supply-side catalyst in the field: World said daily unlocks will fall by about 43% from ~5.1M to ~2.9M WLD starting July 24.

- TON has a credible infrastructure catalyst: Catchain 2.0 brought sub-second finality to mainnet, with blocks now arriving roughly every 400 milliseconds.

Our take: The alpha tape remains discriminating rather than expansionary. This week’s outperformers were not driven by a broad improvement in alt breadth, but by a small set of tokens with clear, asset-specific catalysts. ZEC’s strength was anchored in regulated-access optionality and visible trust accumulation, which gave the move a more durable institutional logic than a simple momentum squeeze. WLD benefited from a meaningful reduction in future token supply, a catalyst that matters disproportionately in a market still highly sensitive to unlock overhang. TON’s outperformance was tied to a tangible network upgrade that improves throughput and strengthens its payments and application-layer case. With TOTAL3 still below its main repair line and higher-beta leadership still unconfirmed, the right interpretation is selective relative strength inside a fragile breadth backdrop, not the start of a broad-based alt regime.

Rails, Regulation, and Institutionalisation - Still the Strongest Structural Story

- Hong Kong granted its first stablecoin issuer licenses to HSBC and Anchorpoint Financial.

- US lawmakers return to Washington for a critical week of negotiations over how stablecoin rewards should be treated in the broader crypto-bill package.

- The ECB backed the EU plan to centralize crypto supervision under ESMA, while Japan’s cabinet approved a bill that would classify crypto assets as financial products and prohibit insider trading.

- Circle launched a payments platform that allows PSPs, fintechs, and banks to use stablecoin rails without having to hold USDC directly, while Chainalysis projected stablecoin volumes could reach $1.5 quadrillion annually by 2035.

Our take: This remains the strongest structural story in crypto. Spot prices are still uneven, but the direction of travel in payments, settlement, licensing, and supervisory architecture keeps improving. Hong Kong licensing, US legislative work, European supervisory consolidation, and new bank-facing payment rails all point the same way: crypto’s investability is being built through stablecoins and tokenized financial infrastructure faster than it is being expressed in the spot charts. That does not remove short-term market fragility, but it continues to improve the medium-term quality of the asset class.

Outlook - Macro Now Has to Validate the Repair

- The immediate Monday open is vulnerable to renewed geopolitical stress after weekend US-Iran talks failed, though the restoration of Saudi pipeline capacity should cushion the worst oil-logistics tail risk.

- The US macro calendar is meaningful: March PPI, industrial production, existing home sales, Empire State, and Philadelphia Fed surveys are all due, while multiple Fed officials are also scheduled to speak.

- China is the other major macro swing factor, with Q1 GDP, March industrial production, March retail sales, and the unemployment rate all due in the same window.

- The IMF/World Bank Spring Meetings run from April 13-18, and the earnings slate includes major US banks plus ASML, TSMC, and Netflix.

Our take: The setup for the coming week is straightforward: the market has earned a repair bid, but macro now has to validate it. If producer prices, industrial activity, and China growth data land in a way that contains the stagflation scare, BTC can keep leaning on the low-$70k shelf and ETH can continue grinding toward its first reclaim level. If inflation pressure remains sticky, geopolitics re-widens the oil shock, or earnings reopen cross-asset growth concerns, the current recovery can still stall beneath structural resistance. The balance of evidence is better than it was two weeks ago, but it is still too early to call full confirmation.

Thanks for reading this week's Market Pulse.