Structural Repair Meets Macro Friction

Blueprint - Flows Improve, Structure Lags

- BTC spot ETFs remained positive but decelerated through the back half of the week, with early strength fading into softer closes as war-driven inflation anxiety returned to the foreground.

- ETH spot ETF demand improved, helped by the debut of BlackRock’s staked Ethereum product, which opened with over $100M in assets and more than $15.5M in first-day volume.

- The macro regime stayed hostile for duration and high beta: the Fed held rates at 3.5%-3.75% and still projected only one cut in 2026, while Powell stressed that inflation must cool further before easing resumes.

- Europe leaned more hawkish as well, with ECB officials openly discussing the possibility of an April hike if war-related price pressure worsens, while UK rate volatility intensified around a hawkish BOE repricing.

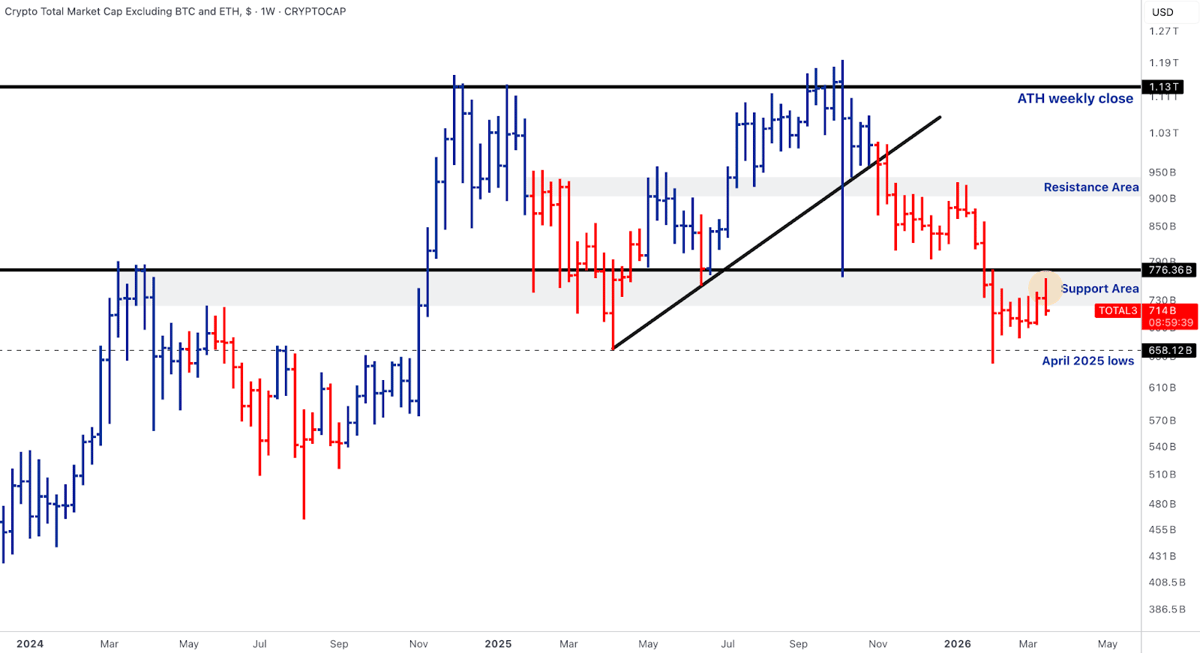

- BTC.D stayed trapped inside its post-breakdown range rather than reasserting leadership, while TOTAL3 continued trying to base above its lower support shelf instead of extending lower immediately.

Our take: The market is still in a macro-driven repair phase, not a clean bull re-acceleration. Price action improved versus the panic lows, but the regime remains constrained by oil-linked inflation risk, delayed rate-cut expectations, and persistent sensitivity to geopolitical headlines. That is why majors are stabilising rather than reclaiming, and why breadth is improving only selectively. The constructive element is that structural crypto adoption did not pause during the drawdown: tokenised funds, tokenised equities, stablecoin rails, staking ETFs and on-chain derivatives all kept advancing. That leaves the market in a familiar late-correction posture: weak enough to remain headline-sensitive, but strong enough that internal infrastructure keeps deepening underneath the surface.

BTC - Corporate Bid Intact, But Still Below Reclaim Bands

- War and inflation fears pushed Bitcoin back below $70,000 during the week after a brief recovery attempt, with Bloomberg describing the move as macro-driven rather than crypto-idiosyncratic.

- The Fed’s hold-plus-higher-for-longer tone and the bond market’s reduced faith in cuts this year kept pressure on duration-sensitive assets, including crypto.

- Selling from older wallets and whales remained part of the tape, but VanEck noted that long-term holder activity has slowed, a constructive signal for medium-term supply pressure.

- Corporate treasury accumulation continued: Strategy bought more BTC, Metaplanet kept expanding its long-run acquisition plan, Strive added BTC, and additional public-company treasury buyers added on weakness.

- Structurally, BTC remains below the major reclaim cluster: prior support in the low-to-mid 70s is the first gate, while the August-lows AVWAP/highs AVWAP zone still caps any true trend repair.

Our take: BTC is trading like a macro asset with embedded structural sponsorship. The structural sponsorship comes from treasury buyers, ETF stickiness, and slower long-term-holder distribution. The macro overlay is what is stopping those positives from becoming trend-following price action. In practical terms, BTC has done the first part of the job by holding the lower support shelf, but it has not done the second part, which is forcing acceptance back into the 70s and then through the AVWAP cluster overhead. Until that happens, this remains a recovery from damage rather than a fresh impulsive uptrend. The tape is better than the headlines, but still not strong enough to call a full regime turn.

ETH - Better Flow Profile, But Relative Leadership Still Needs Proof

- BlackRock’s staked Ethereum ETF had a solid debut, helping improve ETH flow sentiment and reinforcing the staking-plus-ETF transmission channel.

- Bitmine continued expanding its ETH treasury, while the Ethereum Foundation sold 5,000 ETH in an OTC deal to Bitmine, underscoring that treasury-style ETH accumulation remains a live institutional theme.

- A large whale purchase of roughly $111M in ETH added to the sense that opportunistic capital is accumulating into weakness.

- ETH/BTC improved modestly but still sits below the 0.0354 short-term resistance area and far below the 0.0398 broader resistance zone on the weekly structure.

- Spot ETH itself remains below the June 2022 low AVWAP and well below the higher reclaim band overhead.

Our take: ETH is improving on the flow and sponsorship axis faster than on the price and leadership axis. That distinction matters. The staked ETF launch, treasury accumulation and selective whale buying are all constructive because they deepen the case for ETH as an income-bearing institutional asset, not just a beta token. But price still needs to prove that the market is willing to reward those positives. The real confirmation remains the same: ETH/BTC needs to reclaim the mid-0.03s decisively, and spot ETH needs to start rebuilding above broken weekly support. Until then, ETH is no longer in freefall, but it is not yet leading the next rotation leg either.

SOL & BNB

- Solana remains below the January 2023 lows, AVWAP / new resistance around 112-114, but continues to defend the 2024 support zone in the low-80s on the weekly chart.

- BNB has held together far better than most majors, continuing to base above the broad 600 area and keeping the prior structural breakdown far more contained than in BTC, ETH or SOL.

- Solana’s broader ecosystem still has important rails momentum under the surface, but this week’s clearest institutional infrastructure headlines clustered more around tokenised markets, stablecoin rails and exchange-linked settlement than around spot SOL itself.

Our take: SOL is still in repair mode. The fact that it has not broken fresh lows while broad macro pressure persists is useful, but the market still needs a reclaim of the 112-114 zone before the chain re-enters any serious leadership conversation. BNB, by contrast, remains the cleaner relative-strength gauge. It has not delivered a major breakout, but it has also absorbed macro stress without the same degree of structural damage. In a market where leadership is still scarce, that matters. For now, SOL is a stabilisation candidate; BNB is still the higher-quality relative-strength expression among the large-cap alts.

Alpha Cluster - Tactical Rotation Leaders

- DEXE led the approved alpha basket, extending its outperformance as the on-chain asset-management and treasury-execution narrative benefited from tokenised-fund and on-chain credit momentum.

- RIVER continued to track the Bitcoin-infrastructure theme, supported by corporate BTC accumulation and renewed interest in BTC-native rails.

SUN benefited from the stablecoin and settlement-velocity narrative as payment rails continued to expand across the ecosystem. - Hyperliquid remained one of the highest-conviction narrative expressions after Grayscale filed for a HYPE ETF, S&P-branded perpetuals were licensed for Hyperliquid, and tokenised equity/commodity trading momentum kept building.

- INJ stayed relevant through Circle-linked native USDC and cross-chain transfer support, reinforcing its positioning inside the on-chain derivatives and tokenised trading rails theme.

Our take: The alpha tape is telling a clearer story than the majors: capital is rotating toward infrastructure, rails and tokenised-market beta, not into random high-beta reflex bounces. DEXE fits the on-chain asset-management theme. RIVER fits BTC-infrastructure leverage. SUN fits the stablecoin settlement layer. Hyperliquid is the cleanest expression of the on-chain perps and tokenised market thesis. INJ fits the interoperable trading-rails stack. That is why this basket matters: it is not just outperforming, it is outperforming for coherent reasons tied to the week’s most important structural developments. In a market where macro still caps majors, that type of thematic selectivity is exactly where relative alpha should keep appearing.

Rails & Institutional Infrastructure - The Bull Case Keeps Getting Built

- Lawmakers reached an agreement in principle on stablecoin yield treatment, a meaningful step toward broader crypto legislation.

- The SEC and CFTC jointly moved toward a framework under which most crypto assets are not treated as securities, while Nasdaq won approval for a tokenised equities pilot.

- Amundi launched a $100M tokenized fund across Ethereum and Stellar, while Moody’s pushed more credit analysis on-chain.

- Mastercard agreed to acquire stablecoin infrastructure firm BVNK for up to $1.8B, and PayPal expanded PYUSD access to 70 markets.

- Visa rolled out tooling for AI-bot payments, reinforcing the programmable-payments rail as a live commercialisation path.

Our take: This remains the most important bullish section of the report. Spot prices are still wrestling with war, oil and rates, but the underlying crypto stack is moving deeper into the financial system almost every week. Stablecoin legislation is progressing. Tokenised funds are launching. Tokenised equities are being formally piloted. Payment giants are buying infrastructure rather than experimenting around the edges. That is not speculative noise; it is institutional productisation. The market may still be range-bound in the near term, but the rails are becoming too real to dismiss. This is what keeps the medium-term constructive even while the short-term tape remains fragile.

Outlook

- The macro calendar for the week ahead is lighter than the prior FOMC-heavy stretch, but still includes US flash PMIs, US consumer confidence, weekly jobless claims, revised University of Michigan sentiment, import prices and

- Fed speakers; globally, flash PMIs, UK and Japan inflation prints, eurozone confidence data, and several central-bank touchpoints remain important.

- Markets will continue to price war transmission through oil, shipping and inflation expectations, especially around Hormuz disruptions and Kharg Island supply risk.

- BTC’s first technical test remains the lower-70s, with broader trend repair requiring a move back into the high-80s reclaim cluster.

- ETH/BTC still needs a decisive move through the mid-0.03s to validate broader alt rotation.

- TOTAL3 needs to convert the mid-700s into acceptance, while BTC.D remains the best real-time gauge of whether breadth can widen.

Our take: The next move is still likely to be determined less by crypto-specific news than by whether the market starts to believe the oil shock is peaking. If war risk cools and the forward-looking macro data soften just enough, the setup is there for a continued breadth repair: BTC.D can drift lower, TOTAL3 can climb out of support, and selective alts can keep outperforming. If oil keeps grinding higher and central banks stay in hawkish damage-control mode, the market probably remains stuck in a choppy stabilisation regime rather than transitioning into full trend repair. The key point is that crypto now has something it did not have in prior drawdowns: a dense and expanding institutional rail stack underneath price. That does not remove macro risk, but it does change the quality of the base being built.

Thanks for reading this week's Market Pulse.