Liquidity fades into resistance while rails keep compounding

Blueprint - Repair Phase Under Macro Pressure

- BTC spot ETFs posted a weekly net outflow of roughly $464M on the supplied flow sheet, while ETH spot ETFs lost about $191M, and SOL ETPs were essentially flat to slightly negative.

- BTC dominance remains stuck inside its ~58.0%-60.5% range and still below the prior post-double-top breakdown zone, while TOTAL3 is stabilising above the April 2025 low area but remains below the key ~$776B reclaim shelf.

- BTC/ES is still depressed, confirming crypto has not yet re-established relative strength versus US equities.

- Macro stayed restrictive: Treasury rewards hit fresh year highs as oil kept war-driven inflation pressure alive, US consumer sentiment deteriorated with one-year inflation expectations rising to 3.8% from 3.4%, and the Nasdaq 100 fell into a technical correction. Weekend headlines then pointed to the Iran conflict broadening further, with Houthis joining the war and US preparations extending toward potentially weeks of ground operations.

Our take: This remains a repair market, not a reacceleration market. Price has improved from the recent stress lows, but the recovery still lacks the two confirmations that matter most: cleaner institutional sponsorship through ETF flows and a renewed relative-strength impulse versus other risk assets. BTC.D is not breaking down in a way that would validate broad alt leadership, and TOTAL3 has only managed to stabilise at the lower edge of its range rather than reclaim the structure it lost in the first quarter. At the same time, macro conditions remain unfriendly to high-beta assets. Oil, rewards and inflation expectations are still doing the work of tightening financial conditions, leaving crypto caught between tactical relief and structural damage. The strategic offset is that market infrastructure keeps advancing anyway.

BTC - rebound into supply, not reclaim

- BTC is trading in the upper-60s, rebounding into the underside of the ~71-78k resistance zone.

- Price remains below both the BTC highs AVWAP and the August lows AVWAP, with the larger ~87-93k reclaim cluster still overhead.

- Spot BTC ETF demand softened materially again, with US outflows hitting a three-week high. At the same time, Morgan Stanley moved closer to launching its spot BTC ETF with a 0.14% fee, undercutting every current rival and reinforcing that the ETF channel is still becoming more competitive even as near-term demand stays defensive.

- Supply-side flows stayed active: MARA sold 15,133 BTC for about $1.1B to repurchase convertible notes, and additional sovereign / whale BTC transfers kept the overhead supply present.

Our take: BTC’s rebound is real, but it still looks like a relief move into supply rather than the start of a new impulsive phase. That distinction matters. The market has stabilised, but it has done so while ETF demand deteriorated and natural sellers remained active. That combination usually produces bounces that are tradable but difficult to trust. Until BTC can reclaim and hold the low-70s, then begin working back toward the high-80s AVWAP cluster, the dominant interpretation remains bearish repair rather than trend re-acceleration. Morgan Stanley’s aggressive entry into fees is strategically important because it deepens the medium-term institutional distribution channel, but it is not yet translating into immediate price sponsorship.

ETH - sponsorship still weak, infrastructure still strengthening

- ETH is trading around $2k, still below the June 2022 AVWAP (~$2.37k) and well below the April low AVWAP (~$3.0k).

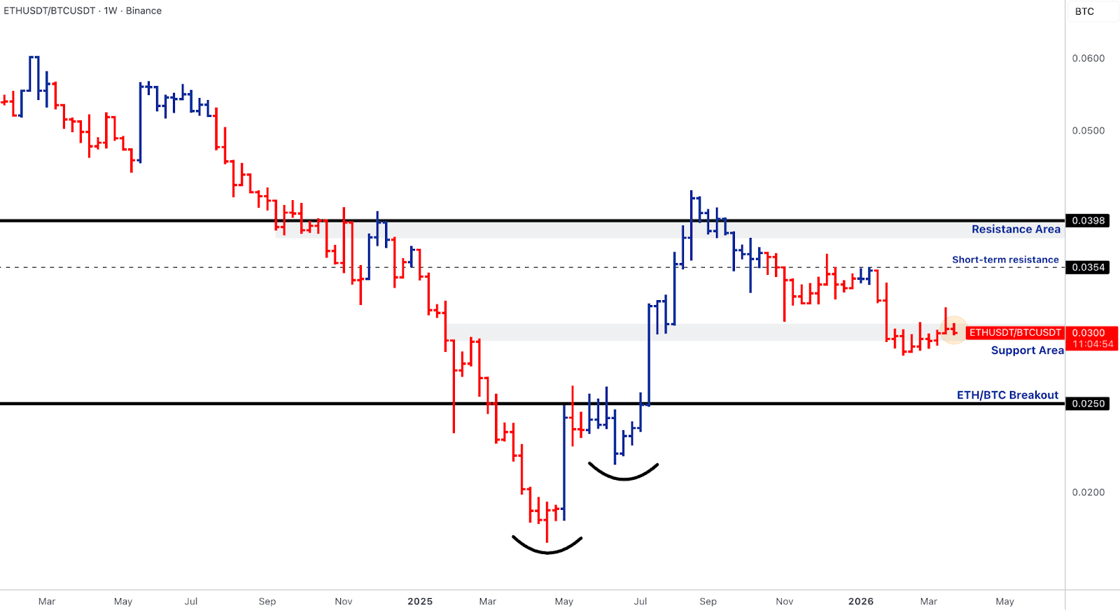

- ETH/BTC is sitting near ~0.03, holding the lower support band but still below the ~0.0354 short-term resistance pivot.

- The supplied ETF table shows roughly $191M of weekly ETH ETF outflows.

- ETH-specific flow remained mixed: legacy wallets continued to distribute, including more OG / ICO-era selling, but BitMine kept expanding its ETH treasury and launched its Mavan staking platform, while Ethereum-linked financialisation kept widening.

Our take: ETH still has not repaired its sponsorship problem. The chart remains weak, ETF demand remained negative, and old-wallet supply is still appearing in strength. But the strategic counterweight continues to build underneath the price. Treasury accumulation, staking-linked productisation and ETH-linked financial infrastructure are all becoming more visible even while the spot chart stays damaged. That is why ETH should still be framed as structurally weak but strategically relevant. The tactical threshold remains simple: hold the 0.029-0.030 ETH/BTC shelf and reclaim 0.035 to improve the relative picture. Until then, ETH is basing beneath resistance, not leading.

SOL & BNB - support holding, leadership absent

- SOL is still pinned near the 2024 lows support area (~$75-85), with the critical reclaim gate unchanged at ~$112-114, where the former breakout shelf and January 2023 AVWAP converge.

- BNB remains below the broken ~$742 breakout shelf and far below the longer-term $1,000 validation level.

- The institutional / enterprise rail story around these ecosystems remains constructive: Mastercard and Western Union tapped Solana Foundation’s enterprise tooling, while BNB is stabilising as an exchange beta rather than reasserting leadership.

Our take: Neither chart is leading. SOL is doing the minimum required to avoid renewed downside expansion, but holding the floor is not the same as repairing the structure. Until it reclaims the 112-114 band, it belongs in the stabilisation bucket rather than the leadership bucket. BNB looks marginally firmer in relative terms because it is leaning more directly into the underside of its prior breakout zone, but the same conclusion holds: below 742, this is still a retest phase rather than a restored trend. Both assets function better as repair gauges than as proof of a new, higher-beta regime.

Alpha Cluster - TAO, AAVE, ONDO and HYPE

- TAO remains the cleanest liquid AI-infrastructure expression in the current alt tape.

- AAVE gained a real protocol catalyst after Aave Labs outlined its V4 reinvestment module, targeting idle liquidity and better lender rewards economics.

- ONDO fits the week’s strongest tokenisation theme after Franklin Templeton moved to tokenise five equity and gold ETF strategies through Ondo.

- HYPE stayed in focus after Grayscale filed for an ETF tracking Hyperliquid exposure, reinforcing the market’s growing acceptance of on-chain perps infrastructure as an investable category.

Our take: The most important feature of this week’s alpha cluster is that it is infrastructure-led, not meme-led. TAO captures selective AI rotation; AAVE reflects DeFi reward-efficiency and protocol cash-flow optimisation; ONDO sits inside the accelerating tokenised-capital-markets buildout; and HYPE expresses the institutionalisation of on-chain trading rails. That mix is telling. It suggests capital is still willing to chase crypto beta, but only where there is a clean structural story and a week-specific catalyst. In other words, the alpha tape is already more selective and higher quality than the broader market.

Rails & Productisation - still the strongest part of the crypto story

- Franklin Templeton’s Ondo partnership, NYSE’s work with Securitise on a 24/7 tokenised-securities platform, and Visa’s deeper Canton engagement all reinforced the tokenised-capital-markets buildout.

- Tether appointed KPMG for its first full financial audit, a notable credibility step for the stablecoin complex.

- Mastercard’s crypto-fiat connector strategy, additional stablecoin payment integrations, Delaware’s stablecoin-issuer legislation, and policy work around tokenisation/innovation exemptions all kept the rails story moving.

- Fannie Mae’s move toward crypto-backed mortgages and White House review of a rule that could eventually open crypto exposure to the $10T 401(k) channel broadened the medium-term access narrative.

Our take: This remains the strongest part of the crypto story. Spot prices are still below broken reclaim bands, but the plumbing keeps improving: tokenised funds, tokenised equities, stablecoin infrastructure, payment distribution, and staking-linked financialisation are all moving deeper into regulated or quasi-regulated channels. That is why the strategic takeaway should remain constructive even when the tactical one stays cautious. Productisation is still outrunning price, and that divergence is likely to matter more over time than another week of weak ETF demand.

Outlook

- Iran / Middle East tensions and oil-market disruption remain the dominant cross-asset risk variable, with the Strait of Hormuz and regional shipping/security still central to inflation and risk sentiment.

- US JOLTS Job Openings (Tue) - important for assessing whether labour demand is cooling enough to support rate-relief expectations. BLS schedules the February JOLTS release for Tuesday, March 31, at 10:00 a.m. ET.

- US ISM Manufacturing (Wed) - a key growth and pricing signal, especially after war-driven energy inflation concerns. ISM schedules the March Manufacturing PMI release for Wednesday, April 1, at 10:00 a.m. ET.

- US ADP Employment (Wed) - useful as a labour-market bridge into payrolls, even if secondary to Friday’s official report.

- US Retail Sales (Wed) - the delayed February release is relevant given the recent soft-consumer backdrop and will shape the market’s read on household demand.

- US Initial Jobless Claims (Thu) - still one of the cleanest weekly reads on labour-market deterioration versus resilience.

- US Nonfarm Payrolls / Unemployment Rate (Fri) - the most important macro release of the week. BLS schedules the March Employment Situation for Friday, April 3, at 8:30 a.m. ET.

- Good Friday liquidity effect (Fri) - payrolls hit on a day when many markets are closed or trading in reduced-liquidity conditions, which raises the probability of sharp moves carrying into the following reopening.

Our take: Crypto remains a high-beta liquidity asset, but next week’s setup is more nuanced than a simple “weak data equals risk-on”. The labour complex is now central. A softer JOLTS / ADP / payrolls sequence could help the market lean back toward rate-relief pricing, which would support BTC’s attempt to reclaim the 71-78k resistance shelf and could give breadth a chance to improve. But that support competes directly with the oil and war channel: if geopolitical escalation keeps energy elevated, weaker growth data may no longer translate cleanly into easier financial conditions.

That leaves three practical market tests. First, BTC still needs acceptance back through the low-70s before the bounce can be treated as more than a repair rally. Second, TOTAL3 needs a reclaim of the ~$776B shelf to argue that breadth is genuinely improving rather than merely stabilising at the lows. Third, ETH/BTC must hold the 0.029-0.030 support zone and push back toward 0.035 to validate broader alt participation. If labour data soften and oil pressure eases, the market can extend stabilisation and selectively reward the strongest infrastructure names. If oil and rewards stay elevated, the more likely outcome is another week of choppy, range-bound repair beneath damaged structure.

Thanks for reading this week's Market Pulse.